Mortgage rates play a major role in determining how affordable a home is, how much buyers can borrow, and whether refinancing makes financial sense. In Utah, where population growth and housing demand remain strong, understanding current mortgage rates—and where they may be headed—is especially important for both first-time buyers and existing homeowners.

This guide breaks down current mortgage rates in Utah, explains what influences them, compares loan options, and offers practical tips for securing the best possible rate in 2025.

Current Mortgage Rates in Utah

Mortgage rates in Utah generally track national trends, but they can vary based on local lenders, borrower qualifications, and loan type. As of today, Utah mortgage rates typically fall into the following categories:

- 30-year fixed mortgage rates: Higher than short-term loans, but offer stable monthly payments

- 15-year fixed mortgage rates: Lower interest rates with higher monthly payments

- Adjustable-rate mortgages (ARMs): Lower initial rates that adjust after a set period

The exact rate a borrower receives depends heavily on credit score, loan size, and whether the loan is for a purchase or refinance. Even small rate differences can add up to tens of thousands of dollars over the life of a loan.

30-Year vs. 15-Year Mortgage Rates in Utah

One of the most common decisions buyers face is choosing between a 30-year and a 15-year mortgage.

A 30-year mortgage offers:

- Lower monthly payments

- Greater cash-flow flexibility

- Higher total interest paid over time

A 15-year mortgage offers:

- Lower interest rates

- Faster equity buildup

- Significant long-term interest savings

For many Utah buyers—especially first-time homebuyers—the 30-year mortgage remains the most popular option. Borrowers with strong income stability, however, may benefit from the long-term savings of a 15-year loan.

Refinance Mortgage Rates in Utah

Utah refinance mortgage rates vary based on market conditions and borrower profiles. Homeowners typically refinance to:

- Lower their interest rate

- Reduce monthly payments

- Switch from an adjustable-rate to a fixed-rate loan

- Access home equity through cash-out refinancing

Refinancing is usually most beneficial when the new rate is meaningfully lower than the existing one and the homeowner plans to stay in the property long enough to recover closing costs.

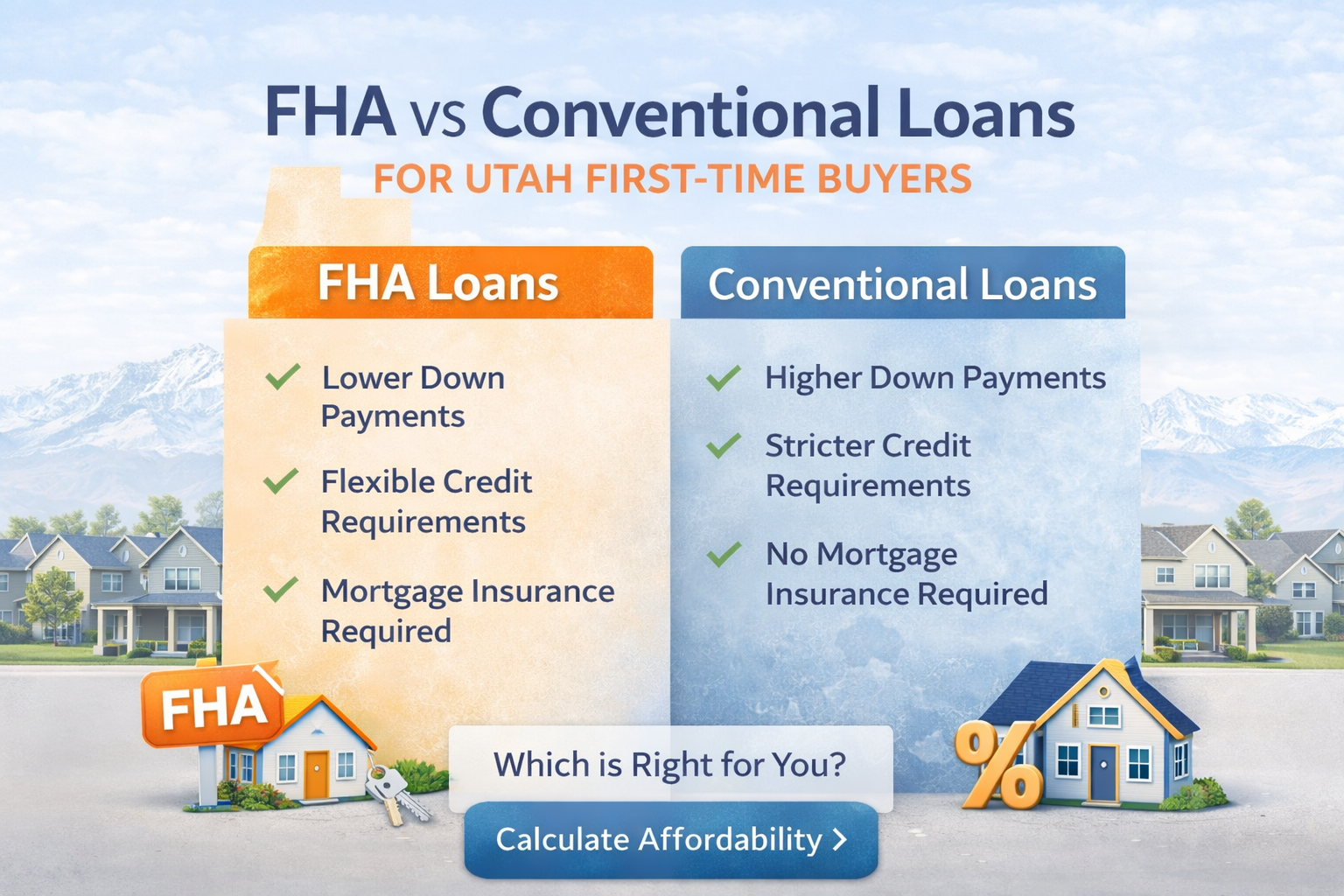

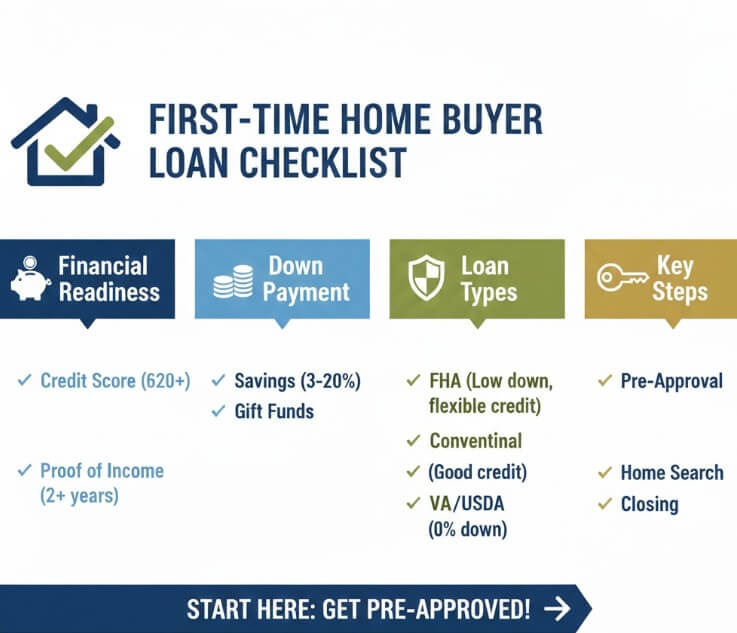

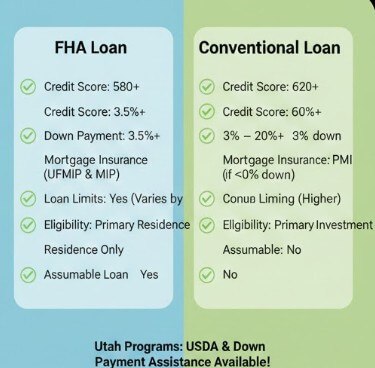

FHA, VA, Conventional, and Jumbo Loan Rates in Utah

Different loan types come with different rate structures and qualification requirements:

- FHA loans: Competitive rates designed for buyers with lower credit scores or smaller down payments

- VA loans: Often among the lowest rates available, reserved for eligible veterans and service members

- Conventional loans: Rates depend heavily on credit score and down payment size

- Jumbo loans: Used for higher-priced homes and may carry slightly higher rates due to increased lender risk

Choosing the right loan type can impact affordability just as much as the interest rate itself.

What Determines Mortgage Rates in Utah?

Several factors influence mortgage rates in Utah, including:

- National economic conditions and inflation

- Federal Reserve interest rate policy

- Housing supply and demand within Utah

- Borrower credit score and debt-to-income ratio

- Loan term, type, and down payment amount

Because lenders evaluate risk differently, comparing offers from multiple lenders is one of the most effective ways to secure a better mortgage rate.

Utah Mortgage Rate Trends and 2025 Forecast

Many buyers are asking whether mortgage rates will drop in Utah. While exact predictions are impossible, most forecasts suggest:

- Rates may gradually stabilize in 2025

- Large, sudden drops are unlikely in the short term

- Smaller fluctuations will continue throughout the year

Rather than trying to time the market perfectly, buyers should focus on affordability, personal finances, and long-term housing plans.

When to Lock a Mortgage Rate in Utah

Locking a mortgage rate can protect borrowers from sudden increases, especially in volatile markets. Borrowers close to finalizing a purchase often benefit from locking early, while those still shopping may monitor trends before committing.

How to Get the Best Mortgage Rate in Utah

To improve your chances of securing the best mortgage rate, consider the following steps:

- Improve your credit score before applying

- Pay down existing debt

- Save for a larger down payment

- Compare multiple lenders

- Understand the differences between fixed and adjustable rates

Using a Utah mortgage rate calculator can also help estimate monthly payments and long-term costs.

Final Thoughts

Mortgage rates in Utah directly affect buying power, monthly payments, and long-term financial stability. Whether you’re purchasing your first home, refinancing, or upgrading to a larger property, understanding current rates and trends allows you to make more confident decisions.

By comparing lenders, choosing the right loan type, and preparing financially, Utah homebuyers and homeowners can navigate the housing market more effectively in 2025.