Embarking on the journey to homeownership is an exciting milestone, but the path to securing a home loan can feel overwhelming. With so many options, from different loan types to fluctuating mortgage rates, it’s crucial to understand each step of the process. This comprehensive guide is designed to demystify the mortgage process in Utah and help you navigate your way to a new home. We’ll break down key terms and provide a clear, step-by-step roadmap to get you from considering a home to holding the keys.

Understanding Your Financial Position and Mortgage Pre-Approval

Before you even start house hunting, the most critical step is to get a clear picture of your finances. This involves looking at your credit history and understanding your debt-to-income ratio. Lenders use these factors to determine your loan eligibility and the interest rate you qualify for. A common question we hear is, “what credit score is needed to buy a house”. While requirements vary by loan type, having a good credit score is essential for securing the best mortgage rates today Utah. Your down payment Utah is another major factor. This is the amount of money you pay upfront toward the purchase of your home. A larger down payment can often lead to a lower interest rate and more favorable loan terms. Understanding these factors upfront will set you up for success. Once you’ve assessed your financial health, the next step is to get pre-approved for a mortgage. This is a formal process where a lender reviews your financial information and provides a pre-approval letter stating the maximum amount you can borrow. This letter is a powerful tool when making an offer on a home, as it shows sellers that you are a serious and qualified buyer. To get started, simply “apply for a mortgage”. This process is different from getting a mortgage prequalification, as it involves a more detailed look at your finances. Once you get a mortgage preapproval, you will receive a mortgage quote which outlines the potential loan terms. This step is a crucial part of knowing “how to get a home loan”.

Choosing the Right Mortgage Loan in Utah

Not all mortgages are created equal. Finding the right mortgage loan for your specific needs is a key part of the process. The “Mortgage Keyword List” PDF highlights several popular options, each with unique benefits and requirements:

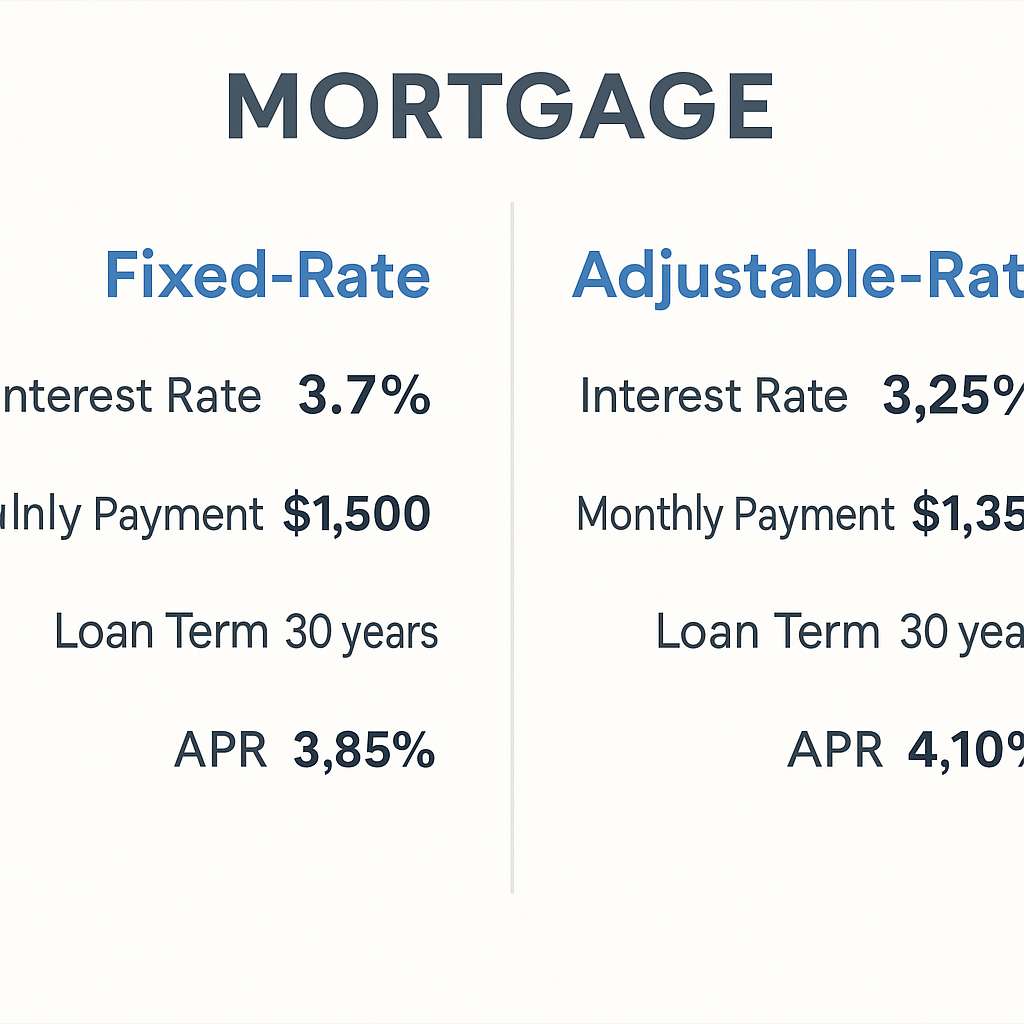

● Fixed-rate mortgage: Offers a constant interest rate and monthly payment for the entire life of the loan. This provides stability and predictability, protecting you from a sudden mortgage rate drop or an increase in your payments.

● Adjustable-rate mortgage: The interest rate fluctuates over time. These loans often start with a lower introductory rate, which can be beneficial if you plan to move or refinance before the rate adjusts.

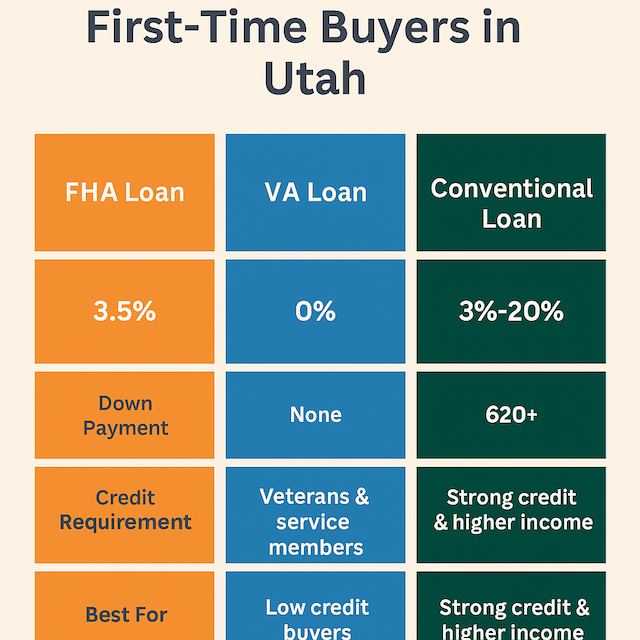

● Conventional loan: A loan not backed by a government agency. These loans often require a higher credit score and a larger down payment than government-backed options.

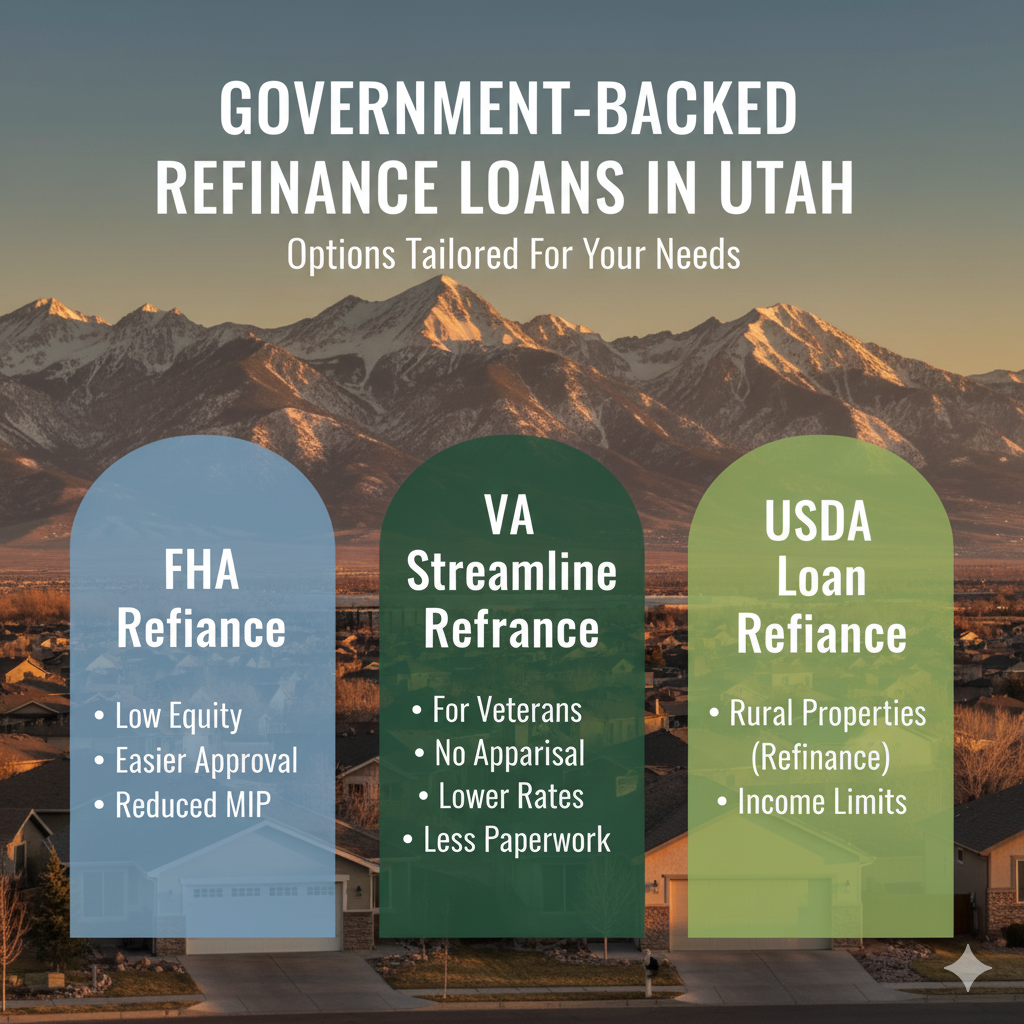

● FHA loan: A loan insured by the Federal Housing Administration, which often has more relaxed credit and down payment requirements. This makes them a popular choice for first-time homebuyers.

● VA home loan: A loan available to eligible service members, veterans, and their spouses, which often requires no down payment.

● USDA loan: A loan for eligible low-income borrowers in rural areas.

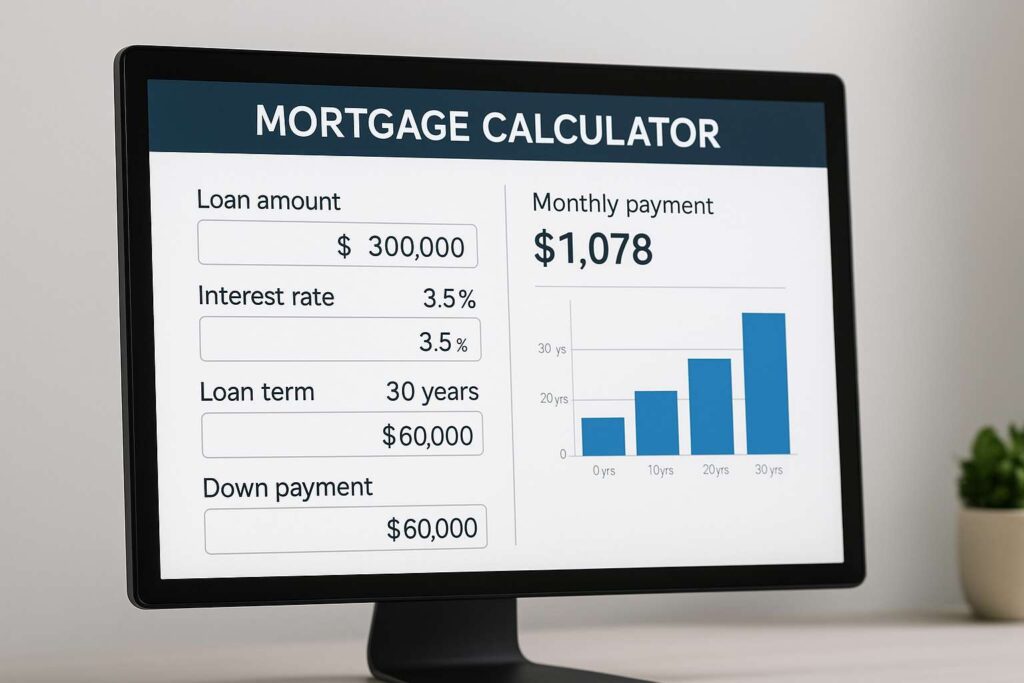

Your mortgage lender will help you compare options, but it’s important to do your own research. Using a mortgage calculator Utah or a home loan calculator can give you an idea of what your monthly payments might look like for each loan type.

The Underwriting Process and Closing the Deal

After you’ve found a home and your offer has been accepted, your loan application moves into the underwriting stage. The “mortgage underwriting Utah” process is where the lender verifies all the information you provided and formally approves your loan. The underwriters will review your financial documents and assess the property’s value. This stage ensures that the loan is a sound financial decision for both you and the lender. When your loan is approved, you will receive a closing disclosure, which outlines the final terms of your loan. It’s crucial to review this document carefully. Pay attention to the annual percentage rate (APR), which represents the total cost of the loan including interest and fees. You may also see “mortgage points”, which are fees paid to the lender in exchange for a lower interest rate. The document will also detail the loan’s amortization, which is the schedule of your loan payments over time. You can use an amortization calculator to see how your monthly payments are applied to both the principal and interest. The final step is closing on your new home. This is where you sign all the necessary paperwork and pay your “closing costs”. These are a variety of fees associated with the purchase of your home, including legal fees, appraisal fees, and more. Make sure to review your closing disclosure at least three days before closing to ensure there are no surprises.

Options for Current Homeowners: Refinancing and Home Equity

For current homeowners, the process is different but just as important. The “Mortgage Keyword List” PDF also highlights several options for leveraging your home’s value or improving your loan terms, including:

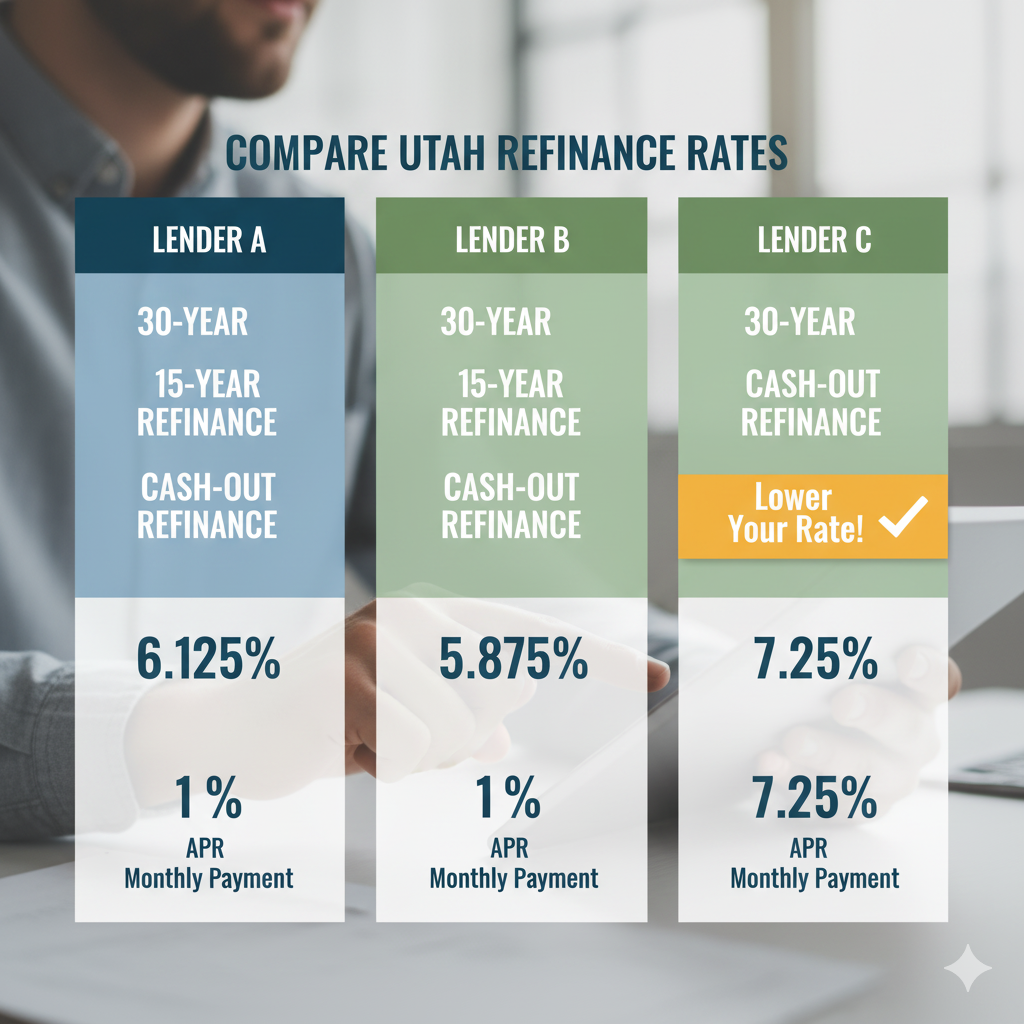

● Refinance rates: If you’re looking to lower your monthly payments or take advantage of a mortgage rate drop, refinancing can be a great option. A refinance calculator can help you understand the potential savings.

● Cash-out refinance: A cash-out refinance allows you to take cash out of your home’s equity while refinancing. A cash-out refinance calculator can help you determine how much cash you can get.

● Home equity loan: Also known as a second mortgage loan, a home equity loan provides a lump sum of money for a fixed period.

● HELOC: A HELOC, or home equity line of credit, provides a flexible line of credit you can draw from as needed. To find the best rates, search for “HELOC rates Utah” or “where to get a HELOC loan”.

● Balloon mortgage Utah: Another option that is popular in Utah is the balloon mortgage, which has a lump sum payment due at the end of the loan term.

Finding the right Utah mortgage rate is essential for saving money on your home loan in Utah. You can also research the different mortgage interest in Utah for your area. When looking for the best lenders, it is helpful to look for best mortgage lenders for first-time buyers who specialize in the Utah market. The mortgage process can be complex, but by taking it one step at a time, you can confidently navigate your way to homeownership or to a more favorable financial position.