Buying a house can feel like being tossed into a frantic situation. While the process is complex, there is no need to fear! Understanding the market starts with finding the right mortgage lenders and home lenders who can explain how to get a home loan without the stress.

The first step for any first time home buyer is education. You need to know your mortgage rates and specifically mortgage rates today because they change faster than the speed of light. Use a home loan calculator to see how different current mortgage interest rates affect your monthly budget.

Preparing Your Application

Before you start looking at houses, you need a loan pre approval or home pre approval. This document is your shield in a competitive market. “What are we going to do?” You’re going to be prepared, that’s what!

When you fill out your mortgage application, lenders will look at your credit score to buy a house. This score determines if you qualify for the lowest home loan rates. If you are a single parent, look for a single parent home loan program designed to provide extra support.

Choosing the Right Loan Product

There is no “luck” in finding the right loan.

You must compare different options: – 5 year arm rates: These can offer lower initial payments. – 2nd home mortgage rates: Essential if you are looking for a vacation getaway. – First time buyer mortgage: Specialized programs for those new to the market. – Refinance rate: Keep an eye on this to see how to lower monthly mortgage payment costs later on.

Leveraging Your Equity

For those who already own property, the focus shifts to a home equity loan. Monitoring home equity rates and home equity loan interest rates allows you to use your home’s value for improvements or other expenses. The plan for your financial future is right here in your home’s equity.

Final Advice from the Pros

It’s all about knowing how to apply for a mortgage and tracking loan rates today. Whether you are a first time home buyer or looking to refinance rate terms, staying informed is your greatest advantage.

Don’t let your mortgage data get lost. Keep your home loan calculator results handy and stay in touch with your mortgage lenders.

For more information on the latest market trends, visit the Consumer Financial Protection Bureau.

The dream of owning a home in the Beehive State is more achievable than many realize, especially with the current Utah housing market forecast 2026 indicating a shift toward a more balanced environment. After years of rapid price escalation, inventory has stabilized, and buyers finally have more room to breathe. However, the most common question remains: Is now a good time to buy a house in Utah? For those prepared to leverage state resources, the answer is a resounding yes. By understanding the various Utah first time home buyer programs, you can navigate the path from renting to owning with financial confidence.

How to Qualify for a Mortgage in Utah and Secure Your Financing

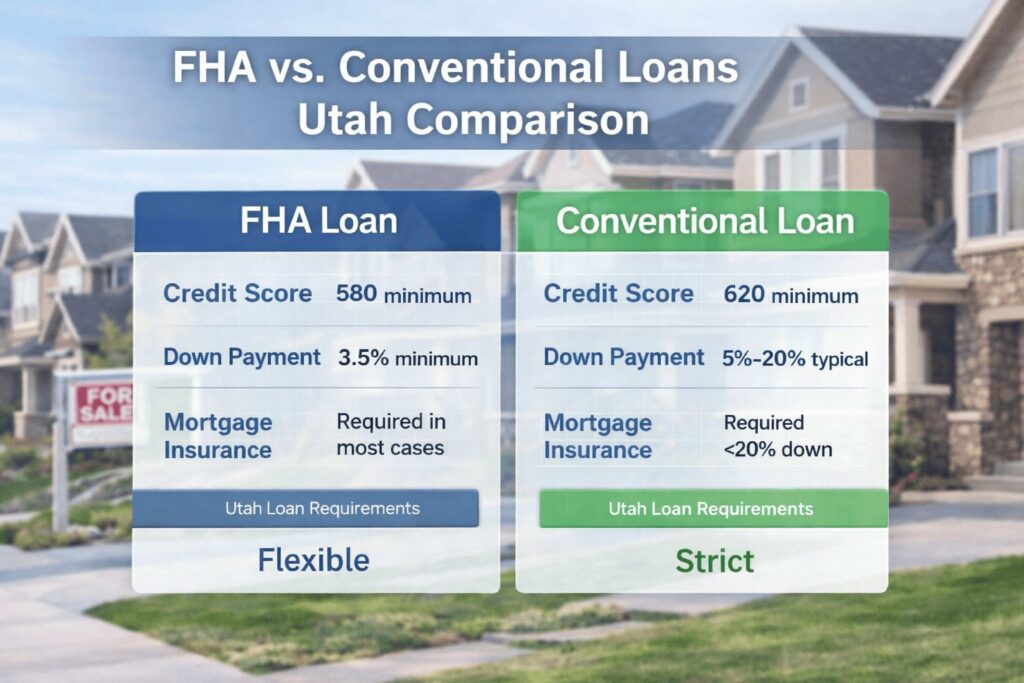

Before you begin touring neighborhoods, you must understand the financial benchmarks required by local lenders. Learning how to qualify for a mortgage in Utah starts with a deep dive into your credit health. The minimum credit score for mortgage in Utah typically ranges between 580 and 620 depending on the loan type, though a higher score will always unlock more competitive interest rates.

To gain a competitive edge, you should initiate the Utah home loan prequalification process as early as possible. This preliminary step gives you a ballpark figure of your borrowing power. However, in a serious market, a formal mortgage pre approval Utah is the “gold standard.” This document proves to sellers that a lender has fully vetted your financial documents and is ready to fund your purchase. During this phase, many buyers ask, “how long does mortgage approval take in Utah?” Generally, once you are under contract, the full underwriting process takes between 30 and 45 days.

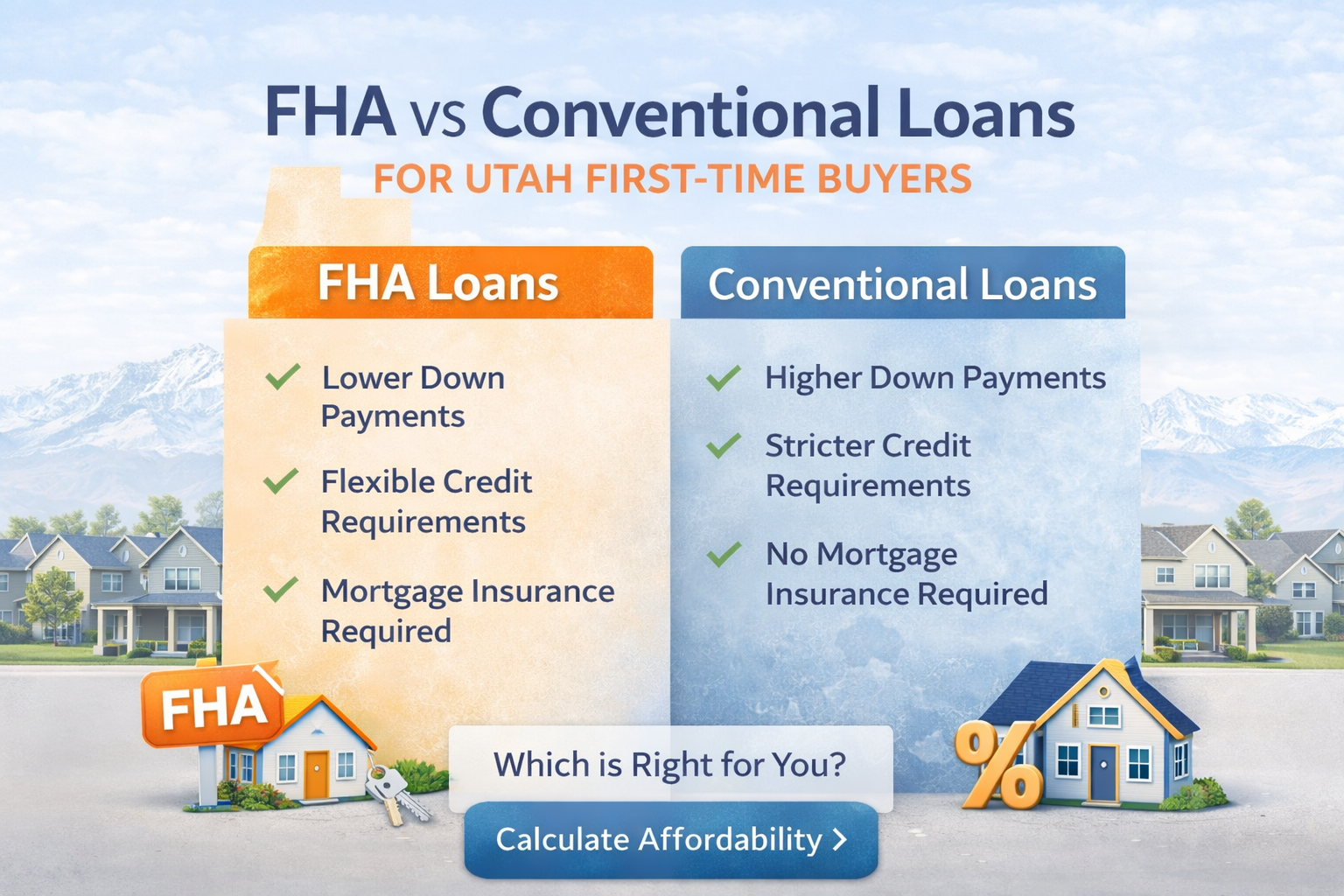

Choosing the right loan product is equally vital. Most buyers weigh the pros and cons of an FHA vs conventional loan Utah. An FHA loan is excellent for those with lower credit scores or smaller down payments, while conventional loan requirements Utah often demand a slightly higher credit profile but may offer lower long-term costs. For specific groups, there are specialized paths:

Utah VA loan eligibility: Veterans and active-duty members can often buy with $0 down.

Utah rural development loan requirements: Those looking in less populated areas may qualify for zero-down USDA financing.

Utah Home Buying Process Step by Step: From Search to Closing

Navigating the Utah home buying process step by step requires a blend of patience and preparation. Once you have secured your pre-approval, the next step is determining your budget. Use a Utah mortgage calculator to look beyond the listing price and understand the full monthly impact of your investment. This tool will help you answer the critical question: “How much house can I afford in Utah?”

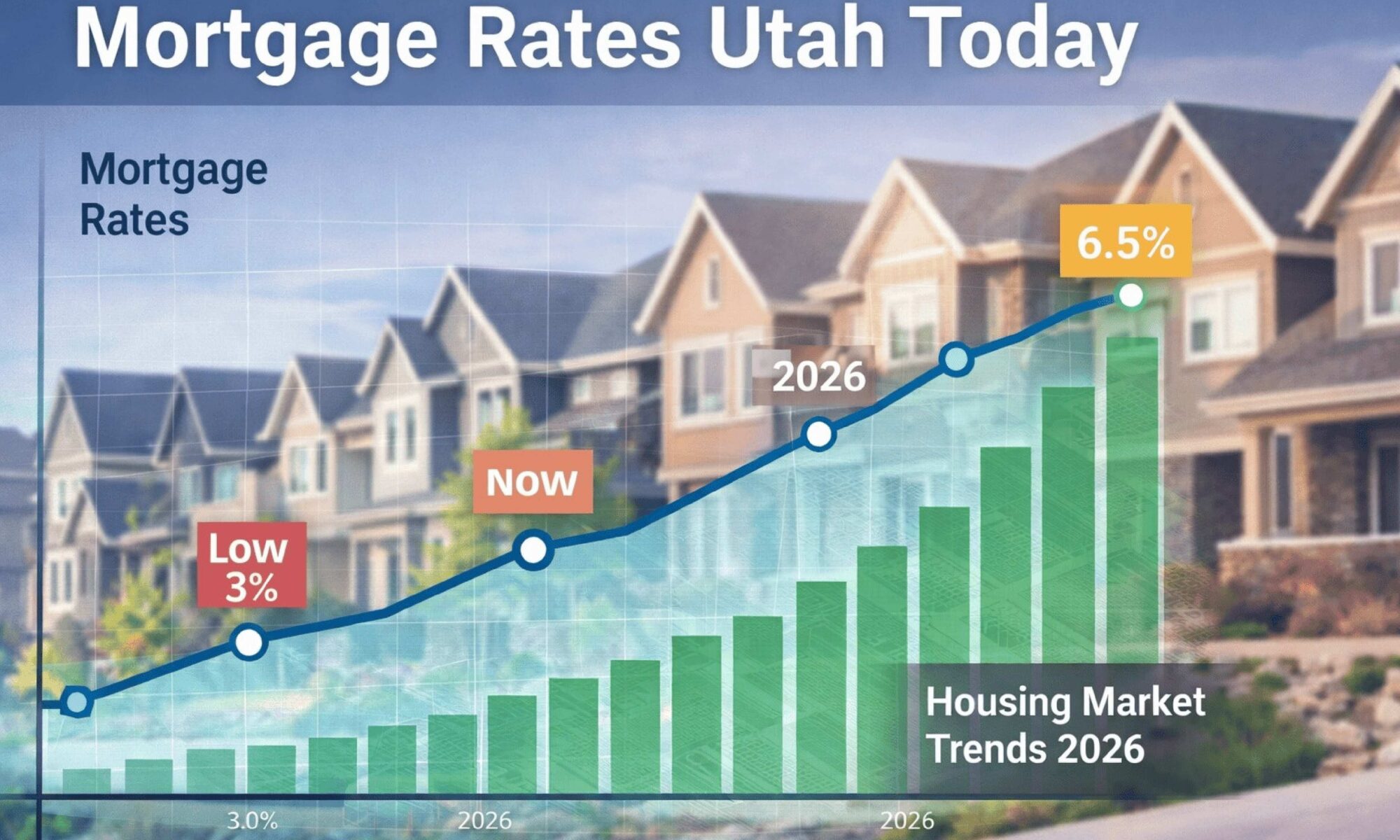

When calculating your budget, don’t forget to account for the average mortgage payment in Utah, which includes principal, interest, taxes, and insurance (PITI). As you monitor the market, keep a close eye on Utah mortgage rates today. In early 2026, 30 year fixed mortgage rates Utah have stabilized, offering a more predictable environment than the volatility seen in previous years. You will also need to decide between a fixed vs adjustable mortgage Utah. While a fixed rate offers a “set it and forget it” stability, an adjustable-rate mortgage (ARM) might offer a lower initial rate if you plan to move or refinance within a few years.

As you approach the finish line, you must prepare for closing costs in Utah. These fees, which cover everything from title insurance to appraisals, typically range from 2% to 5% of the home’s purchase price. To ensure you aren’t overwhelmed by these upfront costs, work with the best mortgage lenders for first time buyers Utah who can help you structure your offer to potentially include seller concessions or lender credits.

Maximizing First Time Home Buyer Grants Utah and Assistance

The most powerful tool in a new buyer’s arsenal is the availability of first time home buyer grants Utah residents can access. The state government and local municipalities have recognized the affordability challenge and created robust down payment assistance Utah initiatives.

One of the most popular programs is the “silent second” mortgage offered through the Utah Housing Corporation, which can provide the funds needed to cover your initial down payment or closing costs. These programs are often designed to work in tandem with other local first time home buyer grants Utah, effectively lowering the barrier to entry. For example, some cities offer forgivable loans if you stay in the home for a set number of years.

Even after you’ve successfully closed on your home, your financial strategy shouldn’t stop. As market conditions change, keep an eye on Utah refinance options for first time buyers. If interest rates drop significantly after your purchase, refinancing can help you lower your monthly payment or eliminate private mortgage insurance (PMI) more quickly as your home equity grows.

Conclusion: Securing Your Future in Utah

The 2026 market presents a unique opportunity for those who are well-informed and ready to act. By mastering the Utah home buying process step by step and taking full advantage of Utah first time home buyer programs, you can secure a home that fits both your lifestyle and your budget. Whether you are aiming for a zero-down path through Utah VA loan eligibility or seeking the best down payment assistance Utah has to offer, the resources are there to support you. Start your journey today by speaking with a local expert to begin your mortgage pre approval Utah and turn the dream of homeownership into a reality.

Self-employed borrowers face unique challenges when qualifying for a home loan. Traditional underwriting models were built for salaried employees, not entrepreneurs with fluctuating income. Fortunately, programs like bank statement home loans and other Non-QM options now make being self-employed and getting a mortgage far more accessible.

If you’ve been wondering, can a self-employed person get a mortgage? — This guide explains exactly how.

Bank Statement Home Loans for Self-Employed Borrowers

A mortgage for the self-employed with bank statements allows borrowers to qualify using 12–24 months of bank deposits instead of tax returns.

Unlike conventional loans, bank statement mortgage loans calculate income based on actual deposits, not net income after deductions. This makes them ideal for business owners who maximize write-offs.

How Bank Statement Mortgage Lenders Calculate Income

Most bank statement mortgage lenders:

Review 12–24 months of personal or business bank statements

Apply an expense ratio (often 50%)

Average monthly deposits to determine qualifying income

This structure makes bank statement home loans one of the most popular options among the best mortgage lenders for self-employed borrowers.

Best Mortgage Lenders for Self Employed in 2026

Choosing the best mortgage lenders for self employed borrowers requires finding lenders that specialize in Non-QM products.

When comparing lenders, consider:

best bank statement mortgage lenders

best no doc mortgage lenders

best non qm lenders

best mortgage company for self employed

best lender for self employed

best mortgage broker for self employed

best mortgage provider for self employed

The best in mortgage lenders for entrepreneurs understand fluctuating income and business deductions.

Internal Link Suggestion

If you have a Non-QM page, link like this:

Explore all Non-QM options here: https://www.yourwebsite.com/non-qm-mortgage-programs

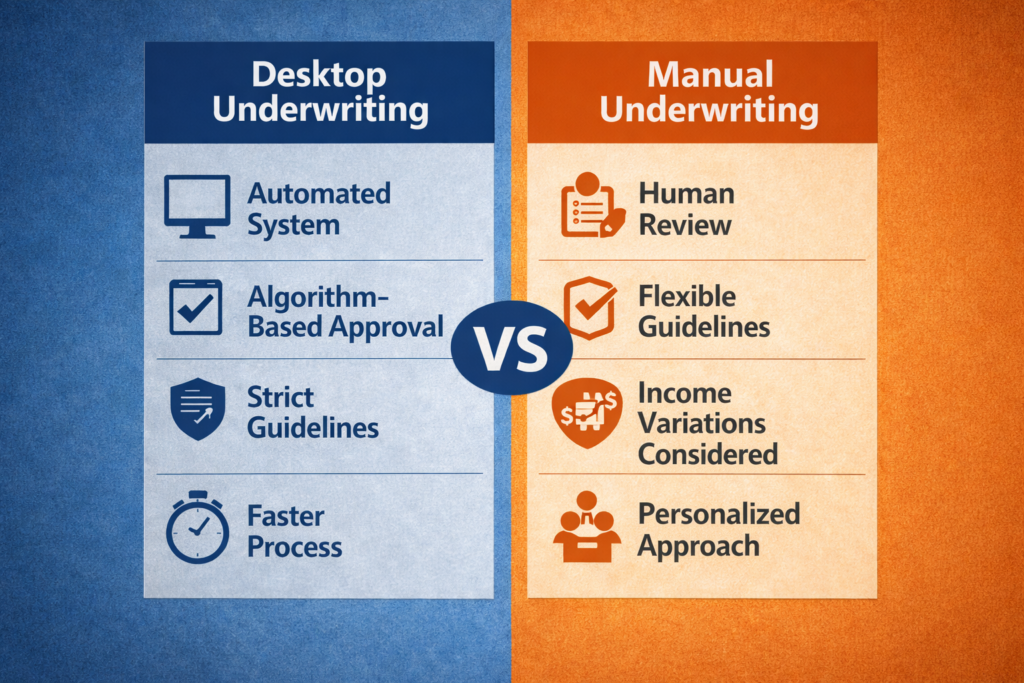

Desktop Underwriting vs Manual Underwriting

Understanding Desktop Underwriting vs Manual Underwriting can dramatically affect approval outcomes.

Desktop Underwriting (DU)

Strict documentation requirements

Automated approval system

Used for conventional loans

Manual Underwriting

Human review process

Greater flexibility

Ideal for self-employed borrowers

Many of the best home lenders for self-employed use manual underwriting when income is complex.

DSCR Loans for Real Estate Investors

If you own rental property, DSCR loans for real estate investors may be better than income-based loans.

Instead of verifying personal income, lenders qualify you based on rental property cash flow.

This makes DSCR programs a strong offering from the best non qm lenders.

Internal Link Suggestion

Learn more about DSCR loan programs here: https://www.yourwebsite.com/dscr-loans-for-real-estate-investors

Anchor text suggestion: DSCR loans for real estate investors

ITIN Home Loans for Non-Citizens

Self-employed borrowers without a Social Security number may qualify for ITIN home loans for non-citizens.

These programs:

Accept Individual Taxpayer Identification Numbers

Often paired with a bank statement, mortgage lenders

Provide alternative documentation options

Best Mortgage Refinance for Self-Employed Borrowers

Refinancing can help entrepreneurs access equity or lower rates.

Borrowers often search for:

best mortgage refinance companies for self-employed

best mortgage refinance for self employed

best refinance companies for self employed

If your tax returns show limited income due to deductions, refinancing with bank statement mortgage loans may offer better qualification terms.

The best mortgage for self employed borrowers depends on the income structure.

You may prefer:

bank statement, home loan,s if you maximize deductions

DSCR loans for real estate investors if you scale rental properties

ITIN home loans for non-citizens if you lack an SSN

Manual underwriting if automated systems decline your file

If you previously researched the best mortgage for self employed 2021 or best mortgage for self employed 2022, you’ll find that today’s programs are more flexible and competitive.

Working with the best home loan lenders for self-employed individuals ensures your application is structured correctly from the beginning.

Can a Self-Employed Person Get a Mortgage?

Yes — and more options exist than ever before.

Whether you’re comparing:

bank statement mortgage lenders

best mortgage lenders for self employed

best no doc mortgage lenders

best mortgage provider for self employed

best refinance companies for self employed

There is a solution that aligns with your business income.

If you’re serious about qualifying, start by speaking with the best lender for self-employed borrowers who understands how entrepreneurs earn, deduct, and grow income.

Buying your first home is a major milestone, and understanding utah mortgage rates for first time buyers is one of the most important steps in the process. Mortgage rates influence how much home you can afford, your monthly payment, and your long-term financial commitment. In Utah’s competitive housing market, being informed can make the difference between feeling confident and feeling overwhelmed.

This guide breaks down current mortgage rate trends, loan options, affordability considerations, and the full application process so first-time buyers can navigate the Utah housing market with clarity.

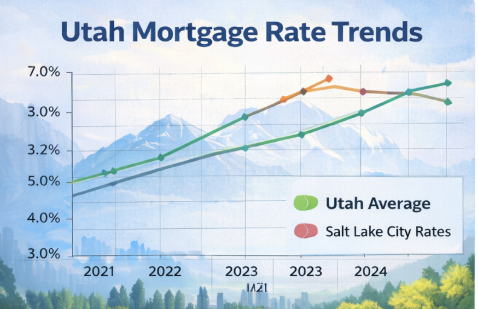

Mortgage Rates Today in Utah and Salt Lake City

Tracking mortgage rates today utah is essential for anyone considering buying or refinancing a home. Rates fluctuate based on economic conditions, inflation, and Federal Reserve policy, which means buyers should stay informed rather than rely on outdated information.

Rates can also vary by location. For example, mortgage rates salt lake city may differ slightly from other areas of the state due to housing demand and lender competition. Borrowers interested in refinancing should also monitor mortgage rates today refinance, refinance rates utah, and refinance rates today utah to determine whether refinancing could lower their monthly payment or overall loan cost.

Comparing multiple offers is critical, which is why using tools that focus on mortgage rate comparison utah can help buyers identify competitive loan options that align with their financial goals.

How Much House Can I Afford in Utah?

A common question among first-time buyers is how much house can i afford utah. Affordability depends on income, existing debt, interest rates, and down payment size. Even small differences in rates can significantly impact monthly payments.

Understanding mortgage down payment requirements utah is also important. While traditional loans often require larger down payments, many buyers qualify for low down payment mortgage utah options that make homeownership more accessible.

In addition to down payments, buyers should explore mortgage payment options utah, including fixed-rate and adjustable-rate loans, to determine which structure best fits their budget and risk tolerance.

FHA Loans and Other First-Time Buyer Options

Many first-time buyers benefit from government-backed loan programs such as FHA loans utah, which are designed to make homeownership more accessible for borrowers with lower down payments or less-than-perfect credit. Searching for FHA loans near me can help buyers connect with lenders who specialize in these programs.

For those specifically entering the market for the first time, a first time buyer fha loan utah can be an excellent option due to flexible qualification requirements. However, it’s still important to compare this option with conventional financing. Understanding conventional vs fha loan utah helps buyers weigh differences in mortgage insurance, interest rates, and long-term costs.

Borrowers with strong credit may also qualify for best home loans utah or best home loans for good credit utah, which can offer lower interest rates and reduced fees.

Credit Scores, Rates, and Timing the Market

Your credit profile plays a major role in determining loan terms. Knowing how credit score affects mortgage rate utahallows buyers to understand how improving their credit before applying could lead to meaningful savings over time.

Timing also matters. Many buyers ask about the best time to buy a house in utah, which depends on market conditions, inventory levels, and interest rate trends. While predicting the market perfectly is impossible, reviewing the utah mortgage interest rate forecast can help buyers make informed decisions about when to lock in a rate.

The Utah Mortgage Application and Approval Process

Understanding the utah home buying process mortgage helps first-time buyers feel prepared rather than surprised. The journey typically starts with pre-approval and continues through underwriting, appraisal, and final approval.

During this process, buyers will encounter the utah mortgage application process, which requires documentation such as income verification, credit history, and asset statements. Knowing the expected mortgage approval timeline utah can reduce stress and help buyers plan their move more effectively.

Working with local home loan lenders utah can be especially beneficial, as local lenders often understand regional market conditions and can provide personalized guidance.

Closing Costs, Rate Locks, and Final Considerations

Beyond the purchase price and interest rate, buyers should budget for average mortgage closing costs utah, which can include appraisal fees, title insurance, and lender charges. Planning for these expenses early helps avoid last-minute surprises.

Another key decision involves utah mortgage rate lock options. Locking in a rate protects buyers from market fluctuations during the loan process, offering peace of mind in a changing rate environment.

Finally, homeowners may want to explore future financing tools such as heloc rates utah, which can provide access to home equity for renovations or other financial needs after purchasing a home.

Preparing for Success as a First-Time Buyer in Utah

Navigating utah mortgage rates for first time buyers doesn’t have to be overwhelming. By understanding current rates, loan options, affordability factors, and the application process, buyers can approach homeownership with confidence. Taking time to compare lenders, improve credit, and plan for upfront costs can make the entire experience smoother and more financially rewarding.

With the right preparation and information, first-time buyers in Utah can turn homeownership from a challenge into an achievable goal.

Navigating the 2026 real estate market requires more than just a passing interest in home listings; it requires a fortified financial strategy. As home prices remain steady and inventory remains a challenge, the first step for any serious buyer is understanding the difference between mortgage prequalification vs preapproval. While a prequalification gives you a ballpark estimate of your buying power based on self-reported data, a preapproval is a rigorous, verified commitment from a lender that carries significant weight when you finally make an offer.

How Much House Can I Afford ?

Determining your budget is the cornerstone of a successful home search. To truly answer the question, “how much house can I afford,” you must look beyond the sticker price and evaluate your monthly cash flow. In 2026, lenders are scrutinizing mortgage income requirements more closely than ever, typically looking for a debt-to-income (DTI) ratio that ensures your total monthly obligations, including your future mortgage, stay within a manageable range.

When running these numbers, many buyers forget to include the mortgage insurance cost, which is a mandatory fee for those putting down less than 20% on a conventional loan or using an FHA product. Furthermore, you must determine exactly how much do I need for a down payment to reach your desired price point. While traditional advice suggests 20%, modern FHA down payment requirements allow buyers to enter the market with as little as 3.5% down, making homeownership accessible even as savings are stretched.

First Time Home Buyer Programs

The path to your first front door is often paved with financial assistance. There are numerous first time home buyer programs available in 2026 designed to lower the barrier to entry for new market participants. These programs often provide a combination of low-interest loans and first time home buyer grants that do not require repayment, provided the buyer remains in the home for a specified period.

Because real estate trends are highly localized, you should also investigate home buyer grants [state-specific] that may offer additional tax credits or cash assistance for down payments. Many buyers find that they can “stack” these benefits with down payment assistance programs and closing cost assistance to significantly reduce the out-of-pocket expenses required at the signing table. Taking the time to research these options before you start touring homes can add tens of thousands of dollars to your effective budget.

How to Improve Credit to Buy a House

Your credit score is the single most important factor in determining your interest rate and loan eligibility. If you find your score is below the minimum credit score for mortgage approval, typically 620 for conventional loans or 580 for FHA, you must prioritize how to improve credit to buy a house. This process includes paying down high-interest credit card debt, ensuring all utility bills are paid on time, and avoiding any new large purchases or credit inquiries in the months leading up to your application.

Once your credit is in a healthy range, you can explore more specialized financing options. For example, if you are looking at properties in less populated areas, a USDA rural development loan offers a 0% down payment option for eligible borrowers. For those with an Individual Taxpayer Identification Number, an ITIN home loan provides a vital alternative to traditional Social Security-based financing. If your dream home is a fixer-upper, the fha 203k loan allows you to bundle renovation costs directly into your mortgage, though you should be prepared for the fact that this specific, “how long does mortgage approval take” question often results in a 45-to-60-day timeline due to the extra inspections required.

Navigating Specific Loan Requirements

Different properties come with vastly different financial hurdles. If you are eyeing a luxury property, you must meet the stringent jumbo loan requirements, which often include higher cash reserves and credit scores. Conversely, those interested in a more affordable entry point might investigate a manufactured home loan, though these require the home to be permanently affixed to a foundation to qualify for traditional real estate rates.

Condo living offers its own set of challenges, as condo financing requirements demand that the homeowner association (HOA) maintains adequate insurance and financial reserves. Regardless of the property type, your lender will conduct a thorough audit of your finances to ensure you meet all mortgage income requirements. Understanding these nuances early in the process, before the clock starts ticking on a purchase agreement, is the difference between a smooth closing and a failed deal.

Buying your first home is an exciting milestone, but understanding your financing options can feel overwhelming. If you are researching first time home buyer mortgage Utah options, exploring loan requirements, or comparing interest rates, this guide will walk you through everything you need to know. From qualification steps to down payment assistance, we’ll cover the essential details to help you move forward confidently.

Current Mortgage Rates Utah for First-Time Buyers

Before choosing a loan, most buyers begin by checking current mortgage rates Utah lenders are offering. Rates directly impact your monthly payment and long-term affordability. You may also see rates referred to as home loan rates Utah, which include conventional, FHA, and other loan types.

For new buyers, understanding first time home buyer Utah interest rates is especially important because certain programs may offer more flexible terms. Rates are influenced by:

Credit score

Debt-to-income ratio

Down payment amount

Loan type

Using a mortgage affordability calculator or a first time home buyer Utah mortgage calculator can help estimate payments based on today’s market conditions.

First Time Home Buyer Programs Utah and Loan Requirements

Many buyers are unaware of the variety of first time home buyer programs Utah offers. These programs are designed to make homeownership more accessible by reducing upfront costs and easing qualification standards.

Understanding first time home owners loan requirements is critical before applying. In most cases, Utah first time home buyer loan requirements include:

Stable employment history

Acceptable credit score

Manageable debt-to-income ratio

Minimum down payment

If you are wondering how to qualify for a mortgage in Utah as a first time buyer, improving your credit, reducing debt, and saving consistently can strengthen your application.

Many first-time buyers choose FHA financing because FHA loan requirements are often more flexible than conventional loans.

FHA Loan Utah First Time Buyer Options

An FHA loan Utah first time buyer program is one of the most popular financing options for new homeowners. FHA loans are attractive because they offer lower minimum credit score thresholds and reduced upfront costs.

The FHA loan down payment can be as low as 3.5%, making it a practical solution for buyers without large savings. However, borrowers must also meet Utah FHA loan income requirements, which consider overall financial stability and debt levels.

For many buyers comparing best mortgage companies for first time buyers, FHA options are a major factor in the decision-making process.

How Much Mortgage Can I Qualify For?

A common question among new buyers is: how much mortgage can I qualify for?

Lenders evaluate income, credit history, monthly debts, and projected expenses. Using a first time home owners loan calculator can help you understand potential payments before formally applying.

If credit concerns are holding you back, you may be searching for how to get pre approved for a loan with bad credit. FHA loans and certain lenders may provide alternative pathways for buyers who are rebuilding credit.

Understanding your purchasing power early in the process helps you shop confidently within your budget.

Mortgage Pre-approval Process Utah Explained

The mortgage preapproval process Utah buyers complete is an essential first step before house hunting.

Here’s how it typically works:

Submit income documentation

Provide authorization for credit review

Review debt and employment history

Receive a preapproval letter

Many buyers ask how to get pre approved for a home loan first time buyer without feeling overwhelmed. Working with an experienced mortgage broker first time home buyer specialist can simplify the process.

A knowledgeable mortgage broker salt lake city professional may also help compare multiple lenders to secure competitive terms.

Best Mortgage Lenders Utah for First-Time Buyers

Choosing the right lender can significantly impact your experience. If you are researching the best mortgage lenders Utah offers, consider factors such as:

Loan program variety

Rate transparency

Customer service

First-time buyer support

Some buyers prefer to search for the best mortgage broker in Utah for first time buyers to receive personalized guidance. Brokers often help compare options from different institutions, increasing flexibility.

You may also explore companies labeled as the best mortgage companies for first time buyers, especially those that specialize in educational resources and program guidance.

Down Payment Assistance for First Time Home Buyers in Utah

Saving for a down payment can be one of the biggest hurdles. Fortunately, there are programs offering down payment assistance for first time home buyers in Utah.

These programs may include:

Grants that do not require repayment

Deferred payment second mortgages

Low-interest assistance loans

Combining assistance programs with competitive first time home buyer mortgage Utah options can dramatically reduce upfront costs.

Bringing It All Together

Navigating first time home buyer mortgage Utah options does not have to be confusing. By understanding:

Current mortgage rates Utah

First time home buyer programs Utah

Utah first time home buyer loan requirements

FHA loan Utah first time buyer options

Mortgage preapproval process Utah

Down payment assistance for first time home buyers in Utah

You can move through the homebuying process with clarity and confidence.

Whether you are comparing the best mortgage lenders Utah, working with a trusted mortgage broker first time home buyer specialist, or calculating affordability with a mortgage affordability calculator, preparation is key.

Your first home in Utah is within reach — and with the right loan program and guidance, homeownership can become a reality sooner than you think.

Buying your first home can feel overwhelming, especially when it comes to understanding loan options. A first time home buyer Utah loan is designed to make homeownership more accessible by offering programs with lower down payments, flexible credit requirements, and potential financial assistance. These loans are specifically structured to help buyers who may not have significant savings or prior experience navigating the mortgage process.

First-Time Homebuyer Loan Options Available in Utah

Utah offers several first-time homebuyer loan programs through both government-backed and conventional options. Many buyers qualify for FHA loans, which allow for smaller down payments and more forgiving credit standards, while others may benefit from USDA or VA loans depending on location and eligibility. In addition, Utah-based housing assistance programs can provide down payment assistance or reduced interest rates, making monthly mortgage payments more manageable.

Qualification Requirements for First-Time Buyers in Utah

To qualify for a first time home buyer Utah loan, lenders typically evaluate income, credit history, employment stability, and debt-to-income ratio. While requirements vary by program, many first-time buyers are surprised to learn that perfect credit is not necessary. Preparing ahead of time by reviewing your credit report, reducing outstanding debt, and saving for upfront costs can significantly improve your chances of approval and secure better loan terms.

How to Choose the Right First Time Home Buyer Utah Loan

Choosing the right loan is an important step toward long-term financial stability. Working with a knowledgeable mortgage professional can help first-time buyers compare loan options, understand eligibility requirements, and identify programs that best fit their financial situation. With the right guidance and preparation, a first time home buyer loan can turn the goal of homeownership into a realistic and achievable milestone. Start today, and watch your dreams in Utah grow!

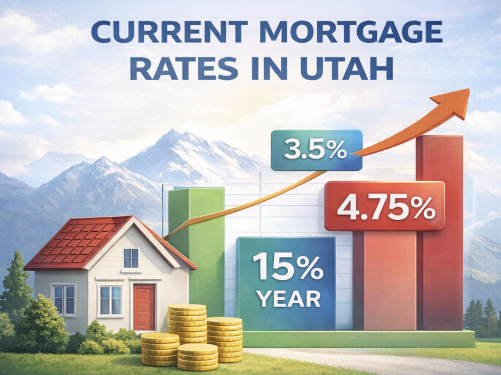

If you are shopping for a home or considering refinancing, understanding current mortgage rates in Utah is essential. Rates shift daily based on inflation, Federal Reserve policy, and overall economic conditions. Monitoring Utah mortgage rates today, along with national mortgage rates today, can help you lock in the best possible loan terms and reduce your long-term costs. Right now, both mortgage interest rates today and housing interest rates today remain sensitive to inflation data and bond market movements. Borrowers should also compare current mortgage rates, fixed mortgage rates today, and mortgage interest rates now to determine whether a fixed or adjustable loan makes more financial sense.

Current mortgage rates in Utah including 30 year and 15 year mortgage rates.

Evaluating Refinance Rates and Utah Housing Market Trends

Those exploring mortgage and refinance options should evaluate refinance mortgage rates and 15 year mortgage refinance rates carefully. Even a small reduction in mortgage interest rates today can significantly lower an average monthly mortgage payment over time. Keeping an eye on housing interest rates today and broader Utah housing market interest rates is critical.

Understanding Mortgage Pre-Approval in Utah

Before making an offer on a home, buyers should understand how to get pre approved for a home loan. A Utah mortgage pre approval provides clarity on budget and strengthens purchase offers. If you are wondering how I can get pre-approved for a home loan, lenders will review income, credit history, debt, and assets to provide a mortgage loan pre approval estimate. Knowing where to get a preapproval for a mortgage — such as local banks, credit unions, or online lenders — can help you secure the best mortgage rates in Utah.

Utah mortgage pre-approval process checklist for first-time home buyers.

Three people in a living room looking at a projected image of a mortgage.

The dream of homeownership is a cornerstone of financial stability, yet the path to achieving it can feel like a maze of paperwork and financial jargon. If you are wondering how to qualify for a home loan with first-time buyer status, you aren’t alone. In 2026, the market has evolved, but the fundamental pillars of credit, income, and preparation remain the bedrock of a successful application. This guide will walk you through every step, from the initial “can I?” to the final “welcome home.”

How to Apply for a Home Loan as a First-Time Buyer and Win

When you are ready to move from browsing listings to making offers, you need to understand how to apply for a home loan as a first-time buyer. Unlike a standard refinance or a move-up purchase, a first-time application requires a deep dive into your financial history to prove your reliability to lenders. The first step in this process is documentation. You will need at least two years of tax returns, recent pay stubs, and bank statements that show the source of your down payment.

Once your paperwork is in order, the next logical question is how to apply for a mortgage as a first-time home buyer. You should look for lenders who specialize in first-time programs, as they are more likely to be patient with your questions and familiar with specialized grants. For many, this also includes researchingfirst-time home buyer incentive programs. These incentives, often provided at the state or federal level, can provide down payment assistance or tax credits that make the monthly payment significantly more affordable. When you finally sit down to apply for mortgage options, don’t just settle for the first quote you receive. Comparison shopping is essential. By applying for first-time home loan products at three different institutions, you can leverage their offers against one another to secure a lower interest rate or reduced closing costs.

How to Get a Home Loan: First-Time Buyer Tips for Success

Hand holding a magnifying glass over a home blueprint, revealing a stack of money.

If you are starting from zero, you are likely asking for what experts recommend. The secret isn’t just having money in the bank; it’s about your debt-to-income (DTI) ratio. Lenders want to see that your total monthly debts, including your future mortgage, don’t exceed a certain percentage of your gross income. Knowing how to get a home loan for the first time involves cleaning up small credit card balances and avoiding new car loans or large purchases in the months leading up to your application.

For those in the early research phase, figuring out how to get a first-time mortgage can feel overwhelming. It begins with a credit check. Even if you think your credit is poor, there are specialized products available. Understanding how to get a mortgage specifically means looking into FHA loans, which allow for lower credit scores, or USDA loans for rural areas. Furthermore, learning how to use tools like the HomeReady or Home Possible programs can help you buy with as little as 3% down.

The ultimate goal for any applicant is to get approved for a first-timehome loan without the stress of a rejection. This requires “mortgage-readiness,” which means having a steady employment history and a clear paper trail for all your funds. When hurdles appear, such as a low appraisal or a high debt load, having a seasoned loan officer can make the difference between a “no” and a “yes.”

Prequalify for Home Loan First Time Buyer: Why It Matters First

A young couple crosses a glowing bridge filled with mortgage documents over a canyon labeled “The Pre-Approval Gap” toward a suburban home.

Before you ever step foot in an open house, you must prequalify for a home loan. Prequalification is a high-level look at your finances that gives you a “ballpark” figure of what you can afford. It is the best way to pre-qualifyfor a home loan as a first-time buyer because it prevents you from falling in love with a house that is outside your budget.

However, in a competitive 2026 market, a simple prequalification isn’t enough. You need to get pre-approved for first-time home buyer status. A pre-approval is much more rigorous; the lender actually verifies your income and runs your credit. Having a pre-approval letter in hand tells a seller that you are a serious, vetted candidate. This is especially true for first-time buyers who are competing against cash investors.

To find the best pre-approval mortgage for first-time home buyers, look for lenders who offer a “fully underwritten” pre-approval. This means a human underwriter has already signed off on your file, making your final closing much faster. Once you have your first time home buyer pre approval or first time home buyer preapproval (as it is often spelled in bank documents), you are officially ready to shop.

Final Steps and Where to Go

You might be wondering where to apply for first-time home buyer programs specifically. Start with your local credit unions or state housing authorities. Knowing where to apply for a first-time home buyer loan can save you thousands in fees. Often, the best place to get a first-time home loan is an institution that offers “first-time buyer” seminars, as they frequently provide “attendance grants” that can be applied to your closing costs.

As you conclude your research, you may still be asking, “Can I get a first-time home loan?” The answer is almost always yes, provided you follow the steps to get a mortgage. Pros suggest: save, build credit, and get professional guidance. Homeownership is a marathon, not a sprint, but by following this roadmap, you are well on your way to the finish line.

Utah homeowners have seen incredible appreciation in property values over the last few years. For seniors aged 62 and older living in the Beehive State, your home is likely your largest financial asset. But having wealth tied up in home equity doesn’t always help with daily living expenses or retirement goals. This is where the best reverse mortgage products come into play. A reverse mortgage, specifically a Home Equity Conversion Mortgage (HECM), allows older homeowners to convert part of their home equity into cash without having to sell the home or take on new monthly mortgage payments. If you are looking to supplement retirement income, cover medical costs, or fund home repairs, understanding this financial tool is essential. This guide will walk you through how to get a reverse mortgage in Utah, define eligibility requirements, and help you identify reputable reverse mortgage lenders.

What Is a Reverse Mortgage and How Does It Work?

Before diving into applications, many Utah seniors ask: Where can I get a reverse mortgage, and how does it actually work?

Unlike a traditional “forward” mortgage where you make monthly payments to a lender to build equity, a reverse mortgage works in reverse. The lender pays you. You can receive these funds as a lump sum, fixed monthly payments, a line of credit, or a combination of these options.

Crucially, you are not required to make monthly principal and interest payments for as long as you live in the home as your primary residence. The loan is typically repaid when the last surviving borrower passes away, sells the home, or moves out permanently.

While most people use these loans to tap existing equity, some current HECM holders find that rising Utah property values allow them to refinance reverse mortgage obligations they already have to access additional funds.

How to Qualify for a Reverse Mortgage: Eligibility for Utah Seniors

The most common question we receive is simple: Can I get a reverse mortgage?

To qualify for reverse mortgage products that are insured by the FHA (which most are), you must meet specific criteria set by the Department of Housing and Urban Development (HUD).

Here are the basic requirements to determine exactly how to qualify for a reverse mortgage:

Age Requirement: The youngest borrower on the title must be at least 62 years old.

Property Type: Your home must be your primary residence. This usually includes single-family homes, specific condos, and some manufactured homes that meet FHA standards.

Equity Position: You must have significant equity in your home—typically at least 50%—or own the home outright.

Financial Assessment: While there are no credit score minimums in the traditional sense, lenders must verify that you have the financial capacity to continue paying property taxes, homeowners insurance, and HOA fees (if applicable).

How to Apply for a Reverse Mortgage: A Step-by-Step Application Guide

Once you determine eligibility, the next step is understanding the mechanics of how to apply for a reverse mortgage. It is a more involved process than a standard home loan due to federal consumer protections.

If you are ready to apply for a reverse mortgage, anticipate these steps:

Step 1: HUD-Approved Counseling Before a reverse mortgage application can even be processed, federal law requires you to attend a counseling session with an independent, HUD-approved agency. This ensures you fully understand the obligations and alternatives.

Step 2: Choosing Providers You will need to select reverse mortgage providers to work with (more on that below) and submit your formal application.

Step 3: Appraisal and Underwriting The lender will order an FHA appraisal to determine the current market value of your Utah home. An underwriter will review your financial information to ensure you meet HUD guidelines to get a reverse mortgage.

Step 4: Closing Once approved, you will sign closing documents. If it is a refinance or a new HECM on an existing home, there is a mandatory three-day right of rescission period before funds are disbursed.

Understanding Reverse Mortgage Interest Rates

Like any loan, the cost of borrowing money matters. Finding the best reverse mortgage rates can significantly impact how much equity you retain over time.

Reverse mortgage interest rates can be fixed or adjustable.

Fixed rates are usually only available if you take the lump-sum payout option at closing.

Adjustable rates are typically chosen by borrowers who want a line of credit or monthly payments.

Because these loans involve compounding interest that is added to the loan balance over time, securing the best reverse mortgage rates for seniors is crucial for long-term estate planning.

Finding Reputable Reverse Mortgage Lenders in Utah

Knowing how can I get a reverse mortgage is half the battle; knowing who to get it from is the other half.

When looking for where to get a reverse mortgage, you generally have three categories of professionals to choose from:

Traditional banks.

Non-bank mortgage lenders specializing in HECMs.

Reverse mortgage brokers, who shop multiple lenders on your behalf.

Trying to find the top rated reverse mortgage company or the best bank for reverse mortgage products requires due diligence. You want to ensure you are dealing with reputable reverse mortgage lenders who are NRMLA (National Reverse Mortgage Lenders Association) members and adhere to strict ethical codes.

Don’t just settle for the first offer. We recommend comparing fees and service levels from several best reverse mortgage lenders active in the Utah market.

Is a Utah Reverse Mortgage Your Best Path Forward?

Tapping into your home equity is a major financial milestone, and for many Utah retirees, it’s the key to staying in the neighborhood they love while enjoying a comfortable retirement. However, the best reverse mortgage for one person might not be the right fit for another.

If you’re ready to see how the numbers look for your specific home, the next step is to compare reverse mortgage interest rates and get a professional reverse mortgage quote. By doing your homework and choosing reputable reverse mortgage lenders, you can ensure your home continues to take care of you for years to come.