If you’re a homeowner looking to borrow in 2025, it’s important to compare the best HELOC lenders and home equity loan options. Popular choices like Bank of America HELOC, AmeriSave HELOC, and BECU HELOC offer competitive rates and flexible terms. You can also explore fixed-rate loans such as 15 year loan rates, 30 year loan rates, or shorter options like 2 year fixed home loan rates and 5 year fixed home loan rates. Tools like a 30 year HELOC payment calculator or Bankrate HELOC comparisons can help you decide. If you prefer a one-time payout, lenders like AmeriSave and Bank of America offer home equity loans with fixed payments. Be sure to research ARM loan rates and check Bank of America home loan rates or AimLoan rates to see what fits your budget. Finally, use trusted resources to find the best HELOC rates and the best home equity lenders for your needs.

Navigating mortgage rates as a first-time buyer in Utah can feel overwhelming. From understanding interest rate types to knowing how credit scores impact your rate, this guide can help break it down. Whether you’re buying in Salt Lake, Park City, or St. George, learn some tips that every first-time homebuyer should know before locking in a mortgage.

Mortgage rates determine how much interest you’ll pay over the life of your loan. Even a 0.5% difference can mean thousands in extra costs. First-time buyers should know how rates are tied to broader economic factors like inflation and the Federal Reserve.

First-time buyers often gravitate toward fixed-rate mortgages for predictability. But adjustable-rate mortgages (ARMs) may offer lower initial rates, especially for buyers planning to sell within a few years.

Loan Tip: Ask your lender for side-by-side estimates using a Utah mortgage calculator (internal link).

Higher credit scores generally unlock lower interest rates. Even a modest down payment of 5–10% can help reduce your rate and avoid PMI (private mortgage insurance). Before applying, consider using a free Utah credit report checker to identify ways to improve your score.

Also, don’t settle for the first quote. Compare offers from at least three lenders. Use tools from local Utah mortgage brokers, banks, or credit unions to review both rate and APR (annual percentage rate), which includes fees and closing costs.

Before you make an offer, get pre-approved, not just pre-qualified, to show sellers you’re serious. Set a realistic budget that includes closing costs, property taxes, and potential HOA fees. And don’t forget to factor in future maintenance expenses. Partnering with a local real estate agent who understands Utah’s market can help you find neighborhoods with the best long-term value. Finally, always read the fine print and ask questions – There’s no such thing as a bad one when it comes to your first mortgage.

Ultimately, understanding mortgage rates is a key step toward making smart, confident decisions as a first-time buyer in Utah. Whether you’re deciding between fixed and adjustable rates, checking your credit, or comparing lender offers, the knowledge you gain now will pay off for years.

Home Loans for First Time Buyers: What Are Your Options?

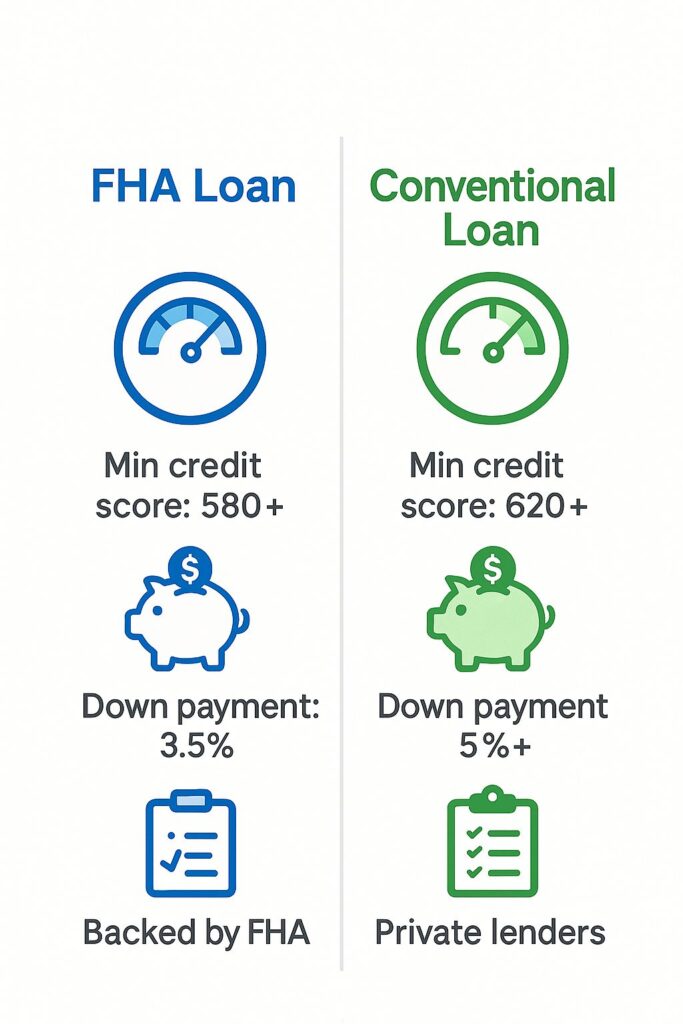

First-time homebuyers often wonder what types of home loans for first time buyers are available. Options include FHA loans, VA loans, and USDA loans, each offering benefits like low or no down payment and flexible credit requirements. If you’re looking for a mortgage for first-time home buyers with lenient credit requirements, FHA loans for first time buyers are a popular choice. In fact, many first time home buyer programs in Utah work in tandem with FHA guidelines to make homeownership more accessible.

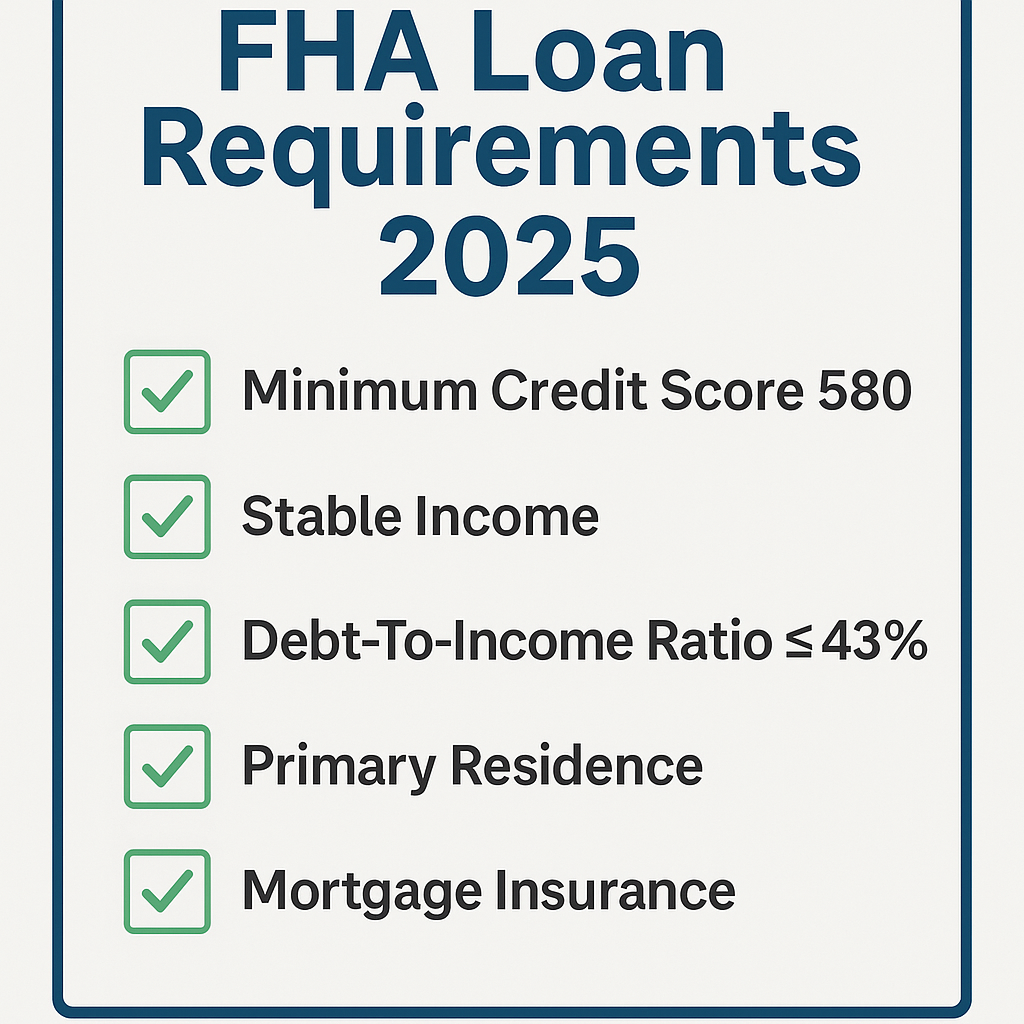

Understanding FHA Loan Requirements in 2025

The FHA loan requirements 2025 include a minimum credit score of 580 for a 3.5% down payment and a stable income history. These loans are government-backed, which makes them less risky for lenders and more accessible for buyers. To get an accurate picture of costs, you can request an FHA mortgage quote from lenders or use online tools. Many first time buyer mortgage quote tools also provide a breakdown of estimated monthly payments and interest rates.

Best Mortgage Lenders for First Time Buyers with No Down Payment

Some lenders specialize in home loans with no down payment. These include best mortgage lenders for first time buyers no-down payment options, which may combine down payment assistance programs with competitive rates. When shopping around, consider the best mortgage lenders for new buyers and compare terms, customer reviews, and loan options. You can also find a local lender near me to work with someone familiar with Utah’s housing market.

Mortgage Rates in Utah Today

If you’re wondering about home rates Utah or home rates today FHA, keep in mind that these can fluctuate based on your credit score, loan type, and market conditions. To make sure you’re getting the best deal, research how to get the lowest mortgage rate and compare offers from multiple providers. Utah homebuyers often benefit from region-specific deals and seasonal rate drops.

Step-by-Step Mortgage Loan Process

Understanding the mortgage loan process step by step can eliminate stress and help you prepare the right documents. Here’s a simplified overview: 1. Get pre-approved – This gives you a clearer budget and strengthens your offer. 2. Submit documentation – Lenders will ask for income, credit history, and ID verification. 3. Appraisal and inspection – These ensure the home is worth the loan amount. 4. Final underwriting – The lender reviews all information before approval. 5. Closing – You sign the final paperwork and officially become a homeowner. Knowing the documents needed to apply for mortgage can help you get through these steps quickly.

Pre-Approval vs Pre-Qualification: What’s the Difference?

Many people confuse pre approval vs pre qualification mortgage. Pre-qualification is an estimate based on unverified information, while pre-approval involves a full credit check and verified documents. Most sellers prefer buyers who are pre-approved because it shows a serious commitment. Learning how to get pre approved for a first home can give you a competitive edge when making an offer.

Assistance Programs and Closing Costs

Utah offers several down payment assistance programs that can significantly reduce upfront costs. These programs are especially useful for first-time buyers who may not have large savings but meet certain income requirements. In addition to down payments, there are closing costs for home loans— typically 2% to 5% of the home’s purchase price. Some assistance programs also help cover these costs, making homeownership more affordable.

How Long Does Mortgage Approval Take?

If you’re wondering how long does mortgage approval take, the average timeline is 30 to 45 days. However, delays can occur if you’re missing documents or the lender needs more information. Getting pre-approved and being organized with paperwork can speed up the process.

Common Mistakes First Time Home Buyers Make

One of the most common mistakes first time home buyers make is not budgeting for all expenses beyond the down payment. These include moving costs, property taxes, HOA fees, and maintenance. Another frequent error is applying for new credit or making large purchases during the approval process, which can jeopardize your loan. Partnering with the best banks for home mortgage ensures you get guidance through each step.

Refinancing Later: When It Makes Sense

Once you’ve been in your home for a few years, you may consider refinancing. Today’s refinance rates 30-year fixed remain competitive, especially for those who originally purchased when rates were higher. Refinancing can help you lower your monthly payment, pay off your loan faster, or cash out equity—but be sure to compare costs and consult a professional.

Unlock Your Future: A Veteran’s Roadmap to First-Time Homeownership in Utah

VA Loan Calculator Guide for Utah First-Time Home Buyers

Published by Kassidy Jo Samuels

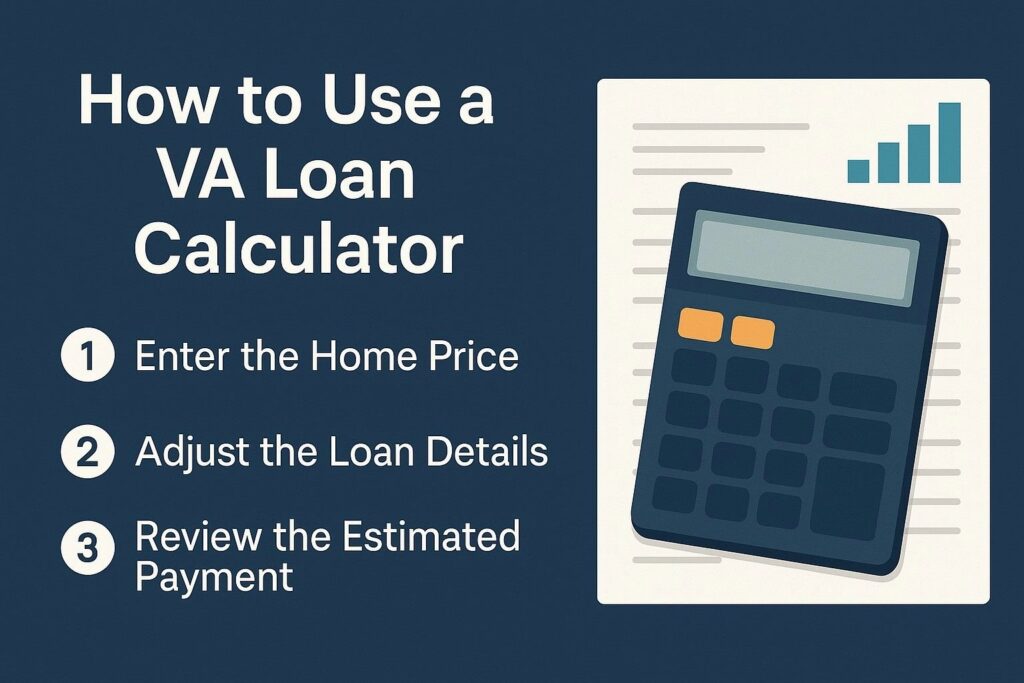

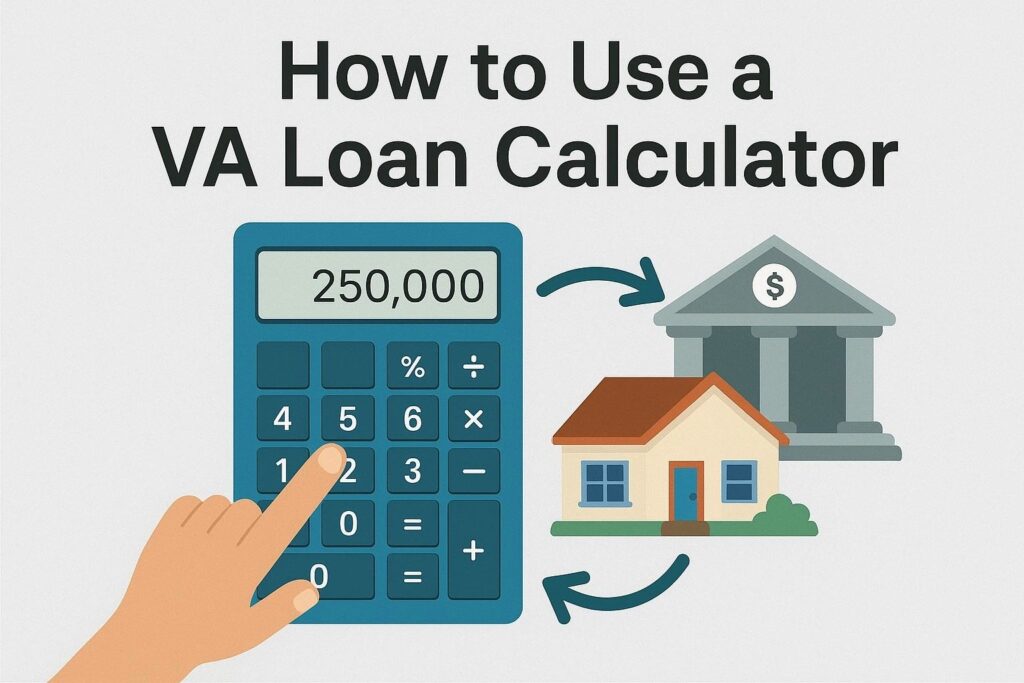

Using a VA Loan Calculator to Estimate Costs

Buying your first home can feel overwhelming, especially if you’re transitioning out of the military and beginning to explore your VA loan benefits. However, whether you’re a veteran or an active-duty service member, taking advantage of the VA home loan program can significantly ease the path to affordable homeownership.

To get started, it’s essential to understand how to estimate your mortgage accurately using a VA loan calculator. Equally important is knowing how to navigate the mortgage pre-approval process with confidence.

In this guide, we’ll walk you through the most important tools—such as a home loan calculator, VA mortgage calculator, and equity home loan calculator—so you can make well-informed decisions about your future in Utah’s competitive housing market

Mortgage Pre-Approval and Loan Calculators

Understanding Mortgage Calculators

If you’re beginning your home buying journey, then a home loan calculator is one of the best places to start. Not only does it provide a quick snapshot of your potential monthly payments, but it also helps estimate how much house you can realistically afford based on key factors like your income, down payment, and loan terms.

For veterans, however, a VA home loan calculator offers an even more accurate estimate. Specifically, it takes into account important VA-specific benefits by factoring in:

VA funding fees

$0 down payment options

Competitive interest rates

The best tools allow you to input principal, interest, property taxes, and insurance—giving you a clear monthly payment estimate to compare offers.

Using VA Loan Payment Calculator Tools

The VA loan program offers significant benefits:

No down payment

No private mortgage insurance

Lower interest rates

Use these tools to your advantage:

VA loan payment calculator: Breaks down monthly costs

Veteran home loan calculator: Compares loan amounts and repayment terms

Equity home loan calculator: Estimates the value of equity over time

Understanding Current Home Loan Interest Rates

Utah’s housing market is competitive, and interest rates fluctuate based on market conditions, your credit, and loan type. Check:

Average home loan interest rates and,

Current Utah rates before locking in

Start by getting pre-approved—a conditional offer from a lender after reviewing your finances. This boosts your credibility with sellers.

Some lenders even offer “pre-pre-approvals” for early-stage planning.

Exploring Veterans United, Rocket, and USAA Home Loans

When comparing lenders, consider:

Veterans United – Veteran-focused service, top-rated resources

Rocket Home Loans – Fast digital pre-approvals

USAA – Especially competitive for military families with strong credit

Use their platforms to:

Compare home loan mortgage rates

Use online calculators

Gather rate estimates

A First-Time Buyer in Utah? Here’s What to Do Next

If you’re applying for a first-time home loan as a veteran:

Compare VA loans with conventional options

Use calculators to evaluate both affordability and long-term savings

Understand that “home loan” and “mortgage loan” are often interchangeable

✔️ Checklist:

Start with mortgage pre-approval

Use VA calculators to check payment estimates

Compare lenders’ interest rates

Review multiple offers before choosing

Final Thoughts on Home Loan Mortgage Rates and Tools

With so many tools at your disposal—from the home loan calculator to the VA mortgage payment calculator—there’s no reason to go into the home buying process unprepared.

Whether you’re checking USAA home loan rates, comparing loan types, or simply exploring your eligibility, you have the tools and benefits to make smart, informed decisions.

Navigating the world of home loans can feel overwhelming. Whether you are buying your first home or refinancing, understanding today’s mortgage rates and the different loan options available is essential. In this guide, we’ll help you compare current mortgage interest rates, explore loan types like FHA loans, VA home loans, and first-time homebuyer loans, and use calculators to find the right mortgage for you.

Compare Current Mortgage Interest Rates

Today’s mortgage rates change daily based on market conditions, your credit score, and the type of loan you choose. Use our Mortgage Rate Comparison Tool to see current mortgage rates & options from the best mortgage lenders in Utah. This will help you decide whether a home equity loan vs. mortgage refinance makes the most sense for your goals. If you prefer a broader overview of national trends, check out Bankrate’s mortgage rates today for external reference.

Estimate Your Monthly Payment

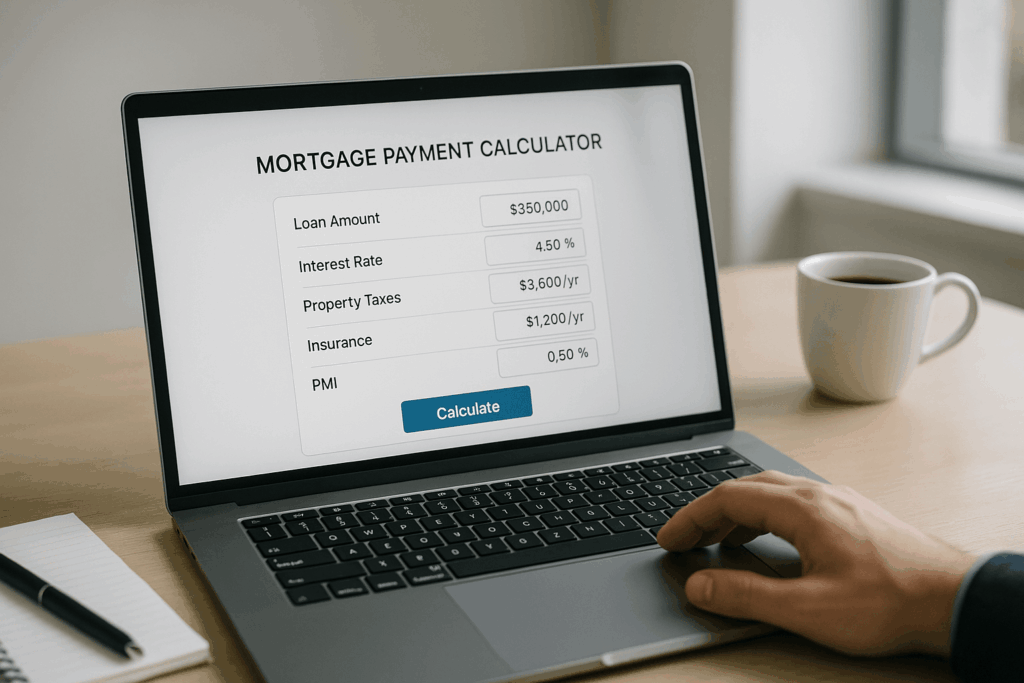

Using a mortgage payment calculator with taxes and insurance helps you understand the true cost of your home. Try our Monthly Mortgage Payment Calculator to include property taxes, homeowners’ insurance, and PMI. For even more accuracy, start with a house payment estimate to see how different down payments and interest rates affect your budget. Before you finalize your budget, don’t forget to review if you qualify for the mortgage interest deduction to lower your tax bill.

Mortgage-payment calculator displayed on a laptop beside a coffee mug and notepad. Created by ChatGPT using OpenAI’s DALL·E image model (29 June 2025).

Popular Loan Options

FHA loans are ideal for buyers with lower credit scores and smaller down payments. VA home loans offer excellent benefits to veterans and active service members, such as no down payment and competitive interest rates. If you are considering other options, first-time homebuyer loans often provide special incentives to make homeownership more accessible. To learn more about FHA loan requirements, visit the official HUD website. If you’re thinking about tapping into your home equity, compare home equity loan vs. mortgage options carefully.

How Much House Can You Afford?

Before you get pre-approved, use a how much house can I afford calculator to find your comfortable price range. This tool works together with a house payment estimate to show how monthly mortgage payment calculator figures align with your income and expenses. Knowing this in advance will streamline the mortgage pre-approval process and help you understand your mortgage loan eligibility.

Mortgage-planning couple. Created by ChatGPT using OpenAI’s DALL·E image model (June 29 2025).

Prepare for the Mortgage Application Process

The mortgage application process requires documentation of your income, assets, and credit history. Be prepared to cover mortgage closing costs, which typically range from 2– 5% of the home price. If you’re wondering how to apply for a mortgage, our step-by-step guide will walk you through each requirement, including tips to improve your credit and boost your mortgage loan eligibility. Already own your home. Compare refinance rates today to see if you can lower your payment or shorten your term. Use our Refinance Calculator to explore your options.

For seniors considering accessing home equity, reverse mortgage lenders may provide specialized products to convert equity into cash.

How to Apply for a Mortgage and Understand Your Eligibility

If you are wondering how to apply for a mortgage, start by gathering your financial

documents, including recent pay stubs, tax returns, and bank statements. This information

will help your lender verify your income and assets. It’s also important to review your credit

report in advance, since your credit score plays a major role in determining your mortgage

loan eligibility.

Most borrowers will begin with a mortgage pre-approval process, which provides a clear

idea of how much you can borrow and the interest rate you are likely to receive. After pre-

approval, you can confidently make offers on properties within your budget. Throughout the

mortgage application process, your lender will guide you step by step to be sure you

understand every requirement and potential mortgage closing costs.

Considering Reverse Mortgage Lenders

For homeowners aged 62 and older, reverse mortgage lenders can help convert part of your home equity into cash without selling your property. A reverse mortgage can be a useful tool for supplementing retirement income or covering unexpected expenses. However, it’s essential to compare offers carefully and consult with a financial advisor to be sure this option aligns with your long-term goals. Always research reputable reverse mortgage lenders and read all disclosures before signing any agreements to avoid surprises with current mortgage rates & options.

Choosing the right mortgage doesn’t have to be complicated. With the right tools and guidance, you can confidently compare today’s mortgage rates, estimate your house payment estimate, and find the loan that fits your needs. Ready to get started? Contact our team to begin your mortgage journey today.

Buying your first home is exciting — but it can also feel overwhelming. Whether you’re wondering how much house you can afford or what your monthly payments will look like, using a home loan mortgage calculator is one of the smartest tools available. This guide will walk first-time buyers through how these calculators work and how they help you understand mortgage rates today, estimate payments, and even prepare for a possible refinance later down the line.

[Image: mortgage-payment-breakdown-graphic.jpg | Alt: Chart showing annual mortgage amortization schedule by year, with principal, interest, and total payments]

One of the first steps to responsible homeownership is knowing what your monthly costs will look like. A mortgage payment estimate includes several factors: the total loan amount, the interest rate, the length of the mortgage (often 15 or 30 years), and any property taxes or insurance.

Using a tool like a mtg calc helps first-time homebuyers see the full picture. Many first time home buyer programs recommend calculating your loan-to-value ratio and your debt-to-income ratio to better plan your finances. This ensures you’re not taking on more debt than you can comfortably manage.

Online calculators typically request inputs like:

Home price

Down payment

Credit score

Current interest rates

Term length (15-year or 30-year)

As you input values, the calculator will give you a monthly mortgage payment, including principal and interest. Some calculators even break down escrow, taxes, and PMI (private mortgage insurance), offering a more comprehensive view.

Why You Should Compare Mortgage Rates Today

It’s essential to compare mortgage rates today before locking in a loan. Rates can fluctuate daily based on economic conditions, inflation, and lender competition. Many calculators let you plug in different home loan mortgage rates to compare outcomes. This helps you decide whether it’s better to go with a fixed mortgage or explore an adjustable-rate mortgage (ARM).

Sites like LendingTree and Bankrate allow you to compare rates from multiple mortgage lenders at once. Even a 0.5% difference in interest can mean thousands of dollars over the life of a loan. That’s why first time homebuyer mortgage tips often emphasize shopping around.

To find the best deal:

Use online tools to compare lenders

Ask about discount points

Factor in closing costs

Consider government-backed loans like FHA, VA, or USDA

Being proactive in rate comparison not only saves money but also makes you a more informed borrower. It’s about more than just getting approved — it’s about getting the best possible deal for your situation.

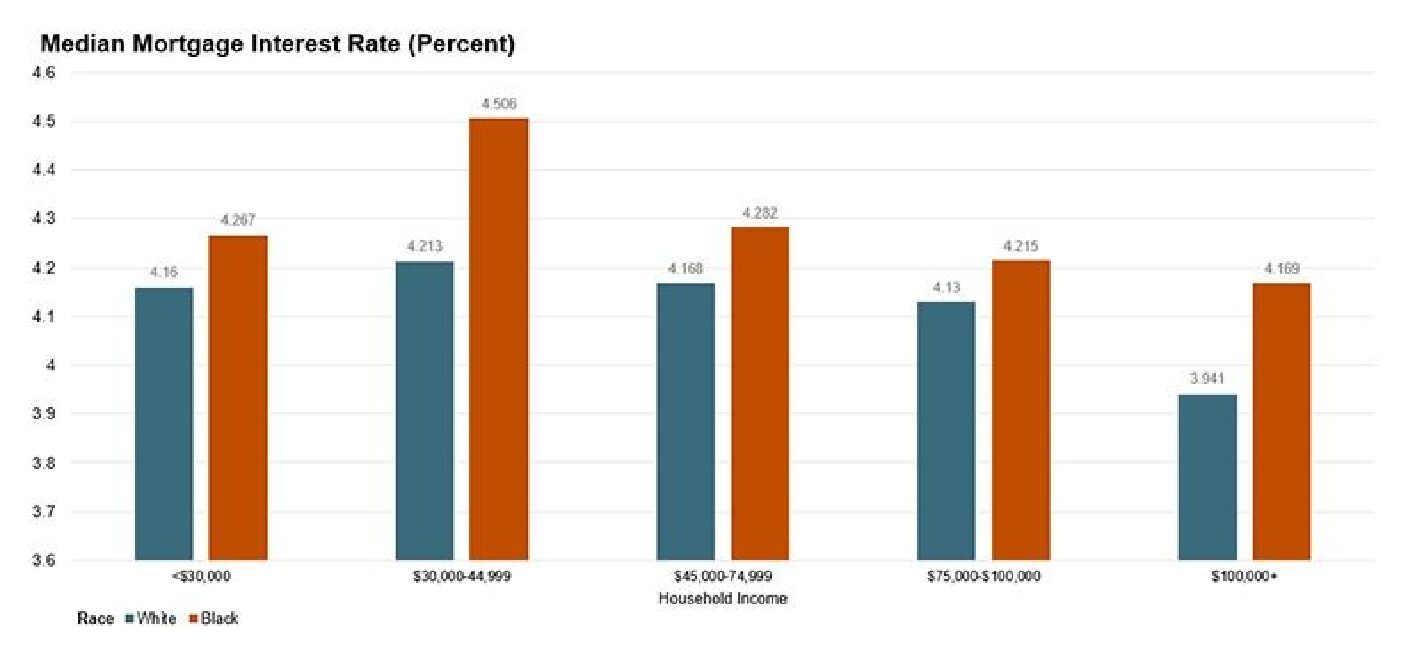

[Image: harvard_jchs_black_homeowner_interest_rates_disparity_hanifa_2021_fig_1_sm.png | Alt: Graph comparing median mortgage interest rates by race and income group]

Using the Calculator for Refinance and Amortization Schedules

Even after you purchase your home, tools like a home loan mortgage calculator remain useful — especially if you’re planning to refinance. Refinancing allows you to replace your current loan with one that has better terms, like a lower interest rate or a shorter loan term.

When you refinance, a new amortization schedule is created, outlining how much of your monthly payment goes toward principal vs. interest over time. Using a calculator to run a refinance scenario helps you:

Decide if refinancing makes financial sense

Estimate new monthly payments

Calculate long-term savings

For example, switching from a 30-year to a 15-year mortgage will increase monthly payments but significantly reduce total interest paid. You might also use a calculator to compare home equity loan or HELOC options for renovations or debt consolidation.

[Image: home-loan-comparison-15-vs-30.jpg | Alt: Bar chart comparing interest paid on 15-year and 30-year mortgage terms]

First-Time Homebuyer Tips: Maximizing Calculator Use

If you’re a first-time homebuyer, the key to using a home loan mortgage calculator effectively is consistency. Run multiple scenarios: adjust the down payment, raise or lower your credit score, and play with different loan terms. Doing this will give you a strong sense of your financial flexibility.

Don’t forget to check your state’s first-time home buyer grants, changing loan limits, and average home prices in your area. This contextual knowledge, paired with smart calculator use, will help you move forward with confidence.

It’s also wise to keep a close eye on your debt-to-income ratio, especially if you’re planning on taking out other loans like car payments or student loans. The lower this ratio, the better your terms will be.

Empowering Yourself with the Right Tools

For anyone navigating the homebuying journey, especially first-timers, tools like a home loan mortgage calculator are essential. Not only do they help you predict monthly payments and compare loan options, but they also prepare you for long-term decisions like refinancing.

Whether you’re figuring out how much house you can afford or weighing different home loan options, being informed and using the right tools gives you a huge advantage. With interest rates always fluctuating and housing markets shifting, staying proactive is your best bet.

Remember: the better your credit score, the better your terms — so work on maintaining strong financial habits even after your loan closes.

By putting in the research now and using calculators smartly, you’ll not only make your home purchase smoother but also set yourself up for long-term financial success.

Understanding current mortgage rates Utah can be the difference between saving thousands or paying more than you should for your home. Whether you’re a first-time buyer or considering a refinance, this guide will help you feel confident in your decisions. We’ll walk you through today’s interest rates, common loan options, and how to get pre approved for mortgage Utah quickly and easily.

Compare Mortgage Rates Utah with Confidence

Before you choose a lender, it’s smart to compare mortgage rates Utah and see what options are available. Rates can change daily and depend on your credit score, income, and loan type. Using a mortgage calculator Utah shows you the impact of different rates and helps you plan your budget accurately.

If you’re shopping for a larger property, pay special attention to Utah jumbo mortgage rates, which can have stricter credit and down payment requirements.

Working with the best mortgage broker Utah can simplify the process. A broker can help you access competitive offers from the best mortgage lenders in Utah and make sure you’re getting the best terms for your situation.

FHA loans are a popular option for buyers who need flexibility. The Utah FHA loan requirements include a minimum credit score and specific property guidelines. With as little as 3.5% down, these loans can help more buyers enter the market.

If you need help with your down payment, consider exploring Utah down payment assistance programs or a zero down mortgage Utah. Both options can make buying a home more affordable, especially for first-time buyers.

Keep in mind that Utah mortgage closing costs can range from 2–5% of your loan amount. Using a mortgage affordability calculator Utah can help you plan for these expenses and avoid surprises.

How to Get Pre Approved for a Mortgage in Utah

The Utah mortgage pre approval process helps you understand exactly how much you can afford and shows sellers you’re serious. You’ll need to provide income documentation, verify employment, and have your credit reviewed. Most buyers can get pre approved for mortgage Utah within a few days.

Remember, the Utah mortgage approval timeline varies depending on the lender and your unique financial picture. If you’re concerned about credit issues, some lenders specialize in working with the best mortgage lenders for bad credit Utah, helping you find options that fit your needs.

Considering Refinancing in Utah?

With rates still relatively low, now can be a great time to explore mortgage refinancing rates Utah. Refinancing can help you lower your monthly payments, reduce your loan term, or tap into equity for renovations and other expenses.

A cash out mortgage refinance Utah allows you to use your home’s value to access cash. Use a mortgage refinance calculator Utah to estimate your savings and see if refinancing makes sense for your goals.

Veterans may qualify for Utah VA mortgage benefits, including no down payment and lower interest rates, making refinancing even more attractive.

Tips for Choosing the Right MortgageLenderin Utah

Finding a lender you trust is as important as finding the right home. Start by reading Utah mortgage lender reviews and asking friends or your real estate agent for recommendations. A good lender should be responsive, transparent, and willing to answer all your questions.

Be sure to compare mortgage brokers Utah to see who offers the best service and rates. The best mortgage broker Utah will guide you through every step and make sure you never feel overwhelmed.

Conclusion

Navigating current mortgage rates Utah doesn’t have to be stressful. With the right tools and a trusted professional by your side, you’ll be able to compare rates, explore loan options, and move into your new home with confidence. Use resources like a mortgage calculator Utah, research Utah FHA loan requirements, and don’t hesitate to ask questions. The more informed you are, the smoother your mortgage journey will be. Staying up to date with mortgage rates Utah can help you save thousands on your home.

If you’re considering buying a home in Utah but are concerned about high down payments or strict credit requirements, an FHA loan Utah could be the solution you’ve been looking for. Backed by the Federal Housing Administration, FHA loans are designed to make homeownership more accessible—especially for first-time buyers and those with moderate incomes.

We’ll break down everything you need to know about FHA loans in Utah, from requirements to current rates, and how to use an loan calculator to estimate your payments.

Top Benefits of FHA Loans

Utah homebuyers can benefit greatly from an FHA loan, especially in today’s competitive housing market. Here’s why:

Lower down payment options (as low as 3.5%)

Competitive mortgage rates

More lenient credit score requirements

Access to FHA approved condos

Streamlined refinancing

To qualify, buyers need to meet certain criteria. While requirements can vary slightly by lender, they generally include:

A minimum credit score of 580 for the 3.5% down payment option

Proof of steady income and employment

The home must be your primary residence

The property must meet FHA appraisal standards

Staying within FHA loan income limits based on location

If you’re unsure whether you meet these guidelines, many lenders offer prequalification tools to help you assess eligibility.

Understanding FHA Loan Mortgage Rates

FHA mortgage rates are often competitive compared to conventional loans, but they can fluctuate based on:

Market conditions

Your credit score

Loan amount and term

Current FHA rates are still historically low, making it a great time to explore your options. Be sure to compare multiple lenders to secure the best possible rates.

Tools to Help You

Before you apply, it’s wise to estimate your monthly mortgage payments using tools like:

Loan Calculator

Mortgage Calculator

Payment Calculator

These calculators help you:

Estimate your monthly principal, interest, taxes, and insurance

Understand how different FHA mortgage interest rates affect your payments

Determine how much you can afford

How to Apply

When you’re ready, follow these steps:

Check your credit score and financial documents

Use an FHA home loan calculator to estimate your payments

Shop around for lenders offering competitive rates

Complete your application and get pre-approved

Find a property that meets FHA approved condos or other requirements

Finalize your loan and close on your new home

Other Options

Beyond standard loans, you might also explore:

203k FHA loan: Great for homes that need repairs or renovations

FHA streamline refinance: A simplified process to lower your rate or monthly payments without extensive documentation

Final Thoughts

For many Utah residents, an FHA loan opens the door to homeownership. By understanding loan requirements, tracking mortgage rates, and using tools, you can make informed decisions and get one step closer to owning your dream home.

Ready to take the next step? Contact a local lender today and explore your options for an FHA loan!

Additional Useful Links

We want to provide you with the most comprehensive set of tools available online. Check out these other links!

Buying a home in Utah is a major milestone, and with that comes important financial decisions including whether to invest in mortgage protection insurance. This guide will walk you through everything you need to know: how to use a mortgage protectioninsurance calculator, understand rates, and assess whether it’s the right fit for your situation.

This guide explores the ins and outs of mortgage protection insurance, how it differs from other policies. And how it fits into the broader picture of mortgages, refinancing, and home equity loans—especially for Utah homeowners.

What is Mortgage Protection Insurance?

Mortgage protection insurance (MPI) is a type of life insurance designed to pay off your mortgage in the event of your death or disability. This ensures that your family can remain in the home without the added stress of monthly mortgage payments.

Many homeowners ask, “Do I need mortgage protection insurance?” The answer depends on your personal and financial circumstances. If you’re the primary income earner and your family would struggle to cover the mortgage without your income, MPI can provide essential security.

Using a Mortgage Protection Insurance Calculator

Before deciding, it’s wise to use a mortgage protection insurance calculator to estimate potential costs and benefits. This tool helps determine your monthly premium based on your age, mortgage amount, and health status. With so many providers available, it’s important to research to find the best mortgage protection insurance for your situation.

Understanding the mortgage protection insurance cost is also crucial. Premiums vary significantly, so comparing options can save you money over time.

Understanding Mortgage Rates in Utah

While insurance protects your mortgage, understanding current mortgage and loan rates helps you make financially sound decisions. Today, mortgage interest rates continue to fluctuate due to market conditions. If you’re shopping for a home, exploring the lowest mortgage rates today or the cheapest mortgagerates today can lead to significant long-term savings.

Whether you’re looking for the best home loan rates for a new purchase or the best homeloan rates refinance to lower your current payment, being informed is your best advantage.

If you’re a veteran, it’s also worth looking into the best VA loan rates and learning how to applyfor a VA loan, which can offer lower interest and favorable terms.

Home Equity and HELOC Rates

Many homeowners tap into the equity of their homes to finance renovations, debt consolidation, or education. This is where understanding home equity rates today and the current HELOCrates comes in. A HELOC (Home Equity Line of Credit) is a revolving line of credit backed by your home’s equity.

Before committing, it’s helpful to use a current HELOC rates calculator and ask, “Whatis the current interest rate on a home equity loan?” This ensures you’re comparing the besthome equity rates today and avoiding costly financial missteps.

Refinance or Not? That’s the Question

Refinancing your mortgage can help reduce your interest rate, change your loan term, or access cash. The decision hinges on many factors—use a refinance calculator to determine whether refinancing makes sense for you.

Ask yourself, “When to refinance mortgage?” The answer often depends on how current rates compare to your original loan, your credit score, and how long you plan to stay in your home.

If you already have a favorable loan, refinancing might not be necessary. However, during times of historically low rates—like many we’ve seen in Utah recently—it may be the perfect opportunity to lock in a better deal.

Navigating the Home buying Process

If you’re in the market to purchase a home, knowing how to buy a house is step one. Surprisingly, one of the most frequently searched topics is also one of the simplest: how to geta mortgage. The answer involves several steps, including checking your credit, saving for a down payment, getting preapproved, and shopping for the best mortgage lenders.

Don’t be discouraged if the process feels overwhelming. Working with a trusted lender or financial advisor can help clarify the path and reduce stress.

If you’re considering an investment, you’ll also want to compare rental property mortgagerates, which are typically higher than primary residence rates due to the added risk for lenders.

Looking Ahead: The Mortgage Rates Forecast

Knowing the mortgage rates forecast can give you a competitive edge whether you’re buying, refinancing, or taking out a home equity loan. Economic indicators like inflation, Federal Reserve decisions, and employment data all influence future rates.

While no one can predict the future with certainty, keeping an eye on forecasts can guide your timing when making major financial decisions—especially if you’re trying to lock in the lowestmortgage rates today.

Final Thoughts

Navigating the world of mortgages, equity, refinancing, and insurance can seem daunting, but knowledge is power. For Utah homeowners, being informed about your options can lead to better decisions, lower costs, and long-term financial security.

To recap, here are a few key takeaways:

● Use tools like a mortgage protection insurance calculator or refinance calculator before making commitments. Shop around for the best mortgage protection insurance, and weigh the mortgageprotection insurance cost against potential benefits.

● Monitor mortgage interest rates, current HELOC rates, and home equity rates today to secure favorable terms. Consider the mortgage rates forecast and evaluate when to refinance mortgage for optimal savings.

● If you’re a first-time buyer understand how to get a mortgage, how to buy a house, and whether you qualify for programs like VA loans.

Being proactive and educated about your financial options ensures that your investment, your home remains a source of comfort and stability for years to come.

Mortgage Rates Today: What Utah Homebuyers Need to Know

When it comes to buying a home or refinancing your current one, staying informed on the mortgage rates today is essential. In a constantly shifting market, knowing the latest rates can help you save thousands over the life of your loan. This guide will break down the most relevant information on refinance rates, HELOC rates, and choosing the best mortgage lenders in Utah.

Current Mortgage Rates and Why They Matter

If you’re shopping for a loan, understanding the current mortgage rates can make a massive difference in your monthly payments. Whether you’re buying your first home or refinancing, even a 0.25% change in rates could significantly impact your affordability.

Many factors influence mortgage interest rates, including Federal Reserve policy, inflation, and housing demand. Fortunately, the average home loan rates in Utah remain competitive compared to national averages, giving local borrowers an edge.

Compare Refinance Rates for the Best Deals

If you’re considering a refinance, you’ll want to closely monitor refinance rates. These rates vary slightly from purchase loan rates and depend on your credit profile, loan term, and equity.

In 2025, many Utah homeowners are locking in savings by exploring refinance mortgage rates with both local banks and national lenders. The goal is to reduce monthly payments, switch to a fixed rate, or tap into equity for renovations.

Exploring HELOC Rates and Home Equity Opportunities

Many homeowners are turning to HELOC rates to leverage the value in their homes. A home equity line of credit allows borrowers to draw funds as needed, often at lower interest than personal loans or credit cards.

If you’re seeking liquidity for major expenses, consider comparing best HELOC rates available through both banks and credit unions. Utah’s home equity loan rates remain favorable in 2025, especially for those with strong credit.

Choosing the Best Mortgage Lenders

With hundreds of options, choosing the best mortgage lenders can feel overwhelming. Look for lenders who offer transparency, fast pre-approvals, and favorable terms on both home loans and refinance mortgage rates.

For Utah borrowers, it’s important to seek out mortgage lenders who understand the local market. The best HELOC lenders may also offer bundled services that combine home equity products with standard loan offerings.

Breaking Down Home Loan Options

Today’s lending environment offers a wide range of home loan interest rates, including both conventional and government-backed options. Borrowers can choose from fixed-rate loans, ARMs, and even low down-payment programs.

Make sure you review not just mortgage rates, but also fees, loan terms, and your long-term goals. Many homebuyers benefit from consulting with loan officers to discuss the best home loan rates based on their financial profile.

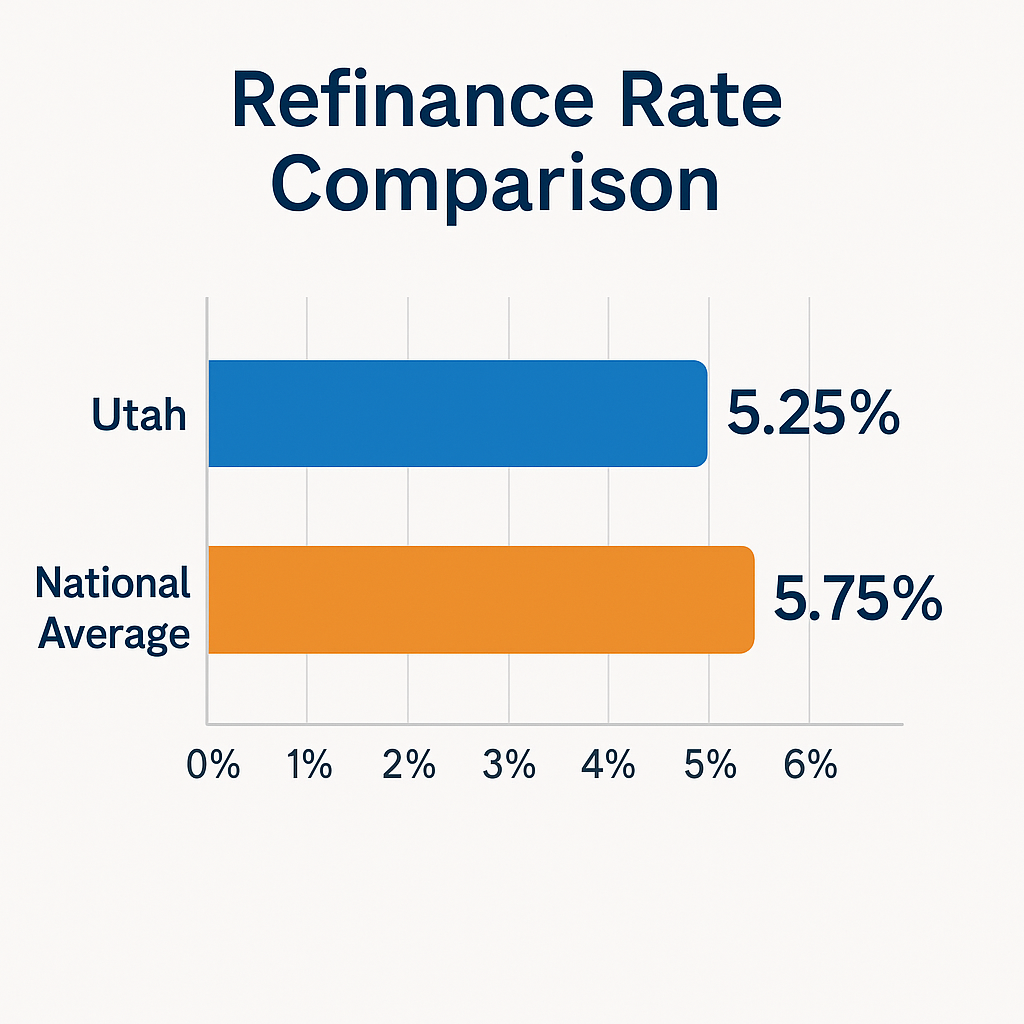

Understanding VA Loan Rates in Utah

Veterans and active-duty service members should explore VA loan rates. These loans typically offer lower rates, no private mortgage insurance (PMI), and more flexible credit requirements.

Local lenders in Utah offer highly competitive va home loan rates and may provide rate reductions through streamlined refinance options. If you’re eligible, these products often beat the best conventional mortgage rates on the market.

Finding the Best Mortgage Rates for Your Situation

So how do you secure the best mortgage rates? Start by checking your credit score, reducing debt-to-income ratio, and comparing offers across multiple lenders. Online comparison tools make it easier to spot deals.

If you’re a first-time homebuyer, working with a local mortgage lender can simplify the process. Whether you’re exploring home refinance rates or new home loans, always ask for a full loan estimate.

Tips to Secure the Lowest Home Loan Rates

To increase your chances of securing the lowest mortgage rates or best home equity loan rates, follow these steps:

Improve your credit score (aim for 720+)

Save for a down payment of at least 20%

Compare loan offers from at least 3 lenders

Opt for shorter loan terms when possible

Final Thoughts: Lock in Your Rate Now

With interest rate uncertainty on the horizon, now is the time to lock in competitive mortgage rates today. Whether you’re buying, refinancing, or accessing home equity, your best move is to get pre-qualified and compare personalized loan offers.

Take advantage of the wide variety of home equity line of credit rates, va mortgage rates, and refinance rates to create a financing plan that fits your goals. The Utah housing market still offers opportunities—seize them with the right mortgage strategy.