Mortgage Pre-Approval in Utah

If you’re planning to buy a home in Utah, getting mortgage pre-approval is one of the smartest first steps you can take. Whether you’re a first-time homebuyer or just looking to better understand the process, this guide will walk you through everything from the mortgage approval process to an actionable application checklist. We’ll also cover FHA loan requirements, down payment assistance programs, and how to apply for a mortgage the right way.

Why Pre-Approval Matters

A mortgage pre-approval is more than just a helpful estimate—it’s a green light that shows sellers and agents you’re serious and financially ready. It also helps you understand how much home you can afford, what your mortgage interest rate might be, and which mortgage lenders or brokers near you are best for your situation.

Mortgage Pre-Approval Checklist

Before applying for pre-approval, gather the following documents and information:

- Proof of income (pay stubs, W-2s, tax returns for 2 years)

- Bank statements (checking, savings, investment accounts)

- Employment verification (current and past employer details)

- Credit score and history

- Photo ID

- List of debts (student loans, credit cards, auto loans)

- Down payment amount and source

If you’re self-employed, you’ll likely need to provide:

- Two years of personal and business tax returns

- Profit and loss statements

- 1099 forms or bank deposits as proof of income

Pro tip: Lenders may also ask for explanations of large deposits or credit inquiries, so keep records handy.

Understanding the Mortgage Approval Process

Here’s a quick look at the typical mortgage approval timeline in Utah:

- Pre-Qualification (Optional): A soft look at your finances, often done online using a mortgage calculator or by submitting estimated income and credit score.

- Pre-Approval: A more thorough process involving document review and a credit check.

- Loan Estimate Issued: You’ll receive details about estimated interest rate, monthly payments, and closing costs.

- Underwriting: A formal risk analysis by the lender that verifies income, employment, credit, and assets.

- Final Approval & Closing: Once underwriting is complete, the lender issues final approval and you move to closing.

Choosing the Right Mortgage Lender or Broker in Utah

When shopping for a home loan, it’s smart to compare offers from different lenders. Use tools to get a mortgage quote, but make sure you understand what’s behind the numbers. Ask each lender about:

- Current interest rates

- Whether the loan is fixed or variable

- Points or fees to buy down your rate

- Whether they offer FHA, VA, or USDA loans

- Utah-specific grants or down payment assistance programs

Keyword tip: Searching “mortgage broker near me” can help you find local professionals who know Utah’s market best.

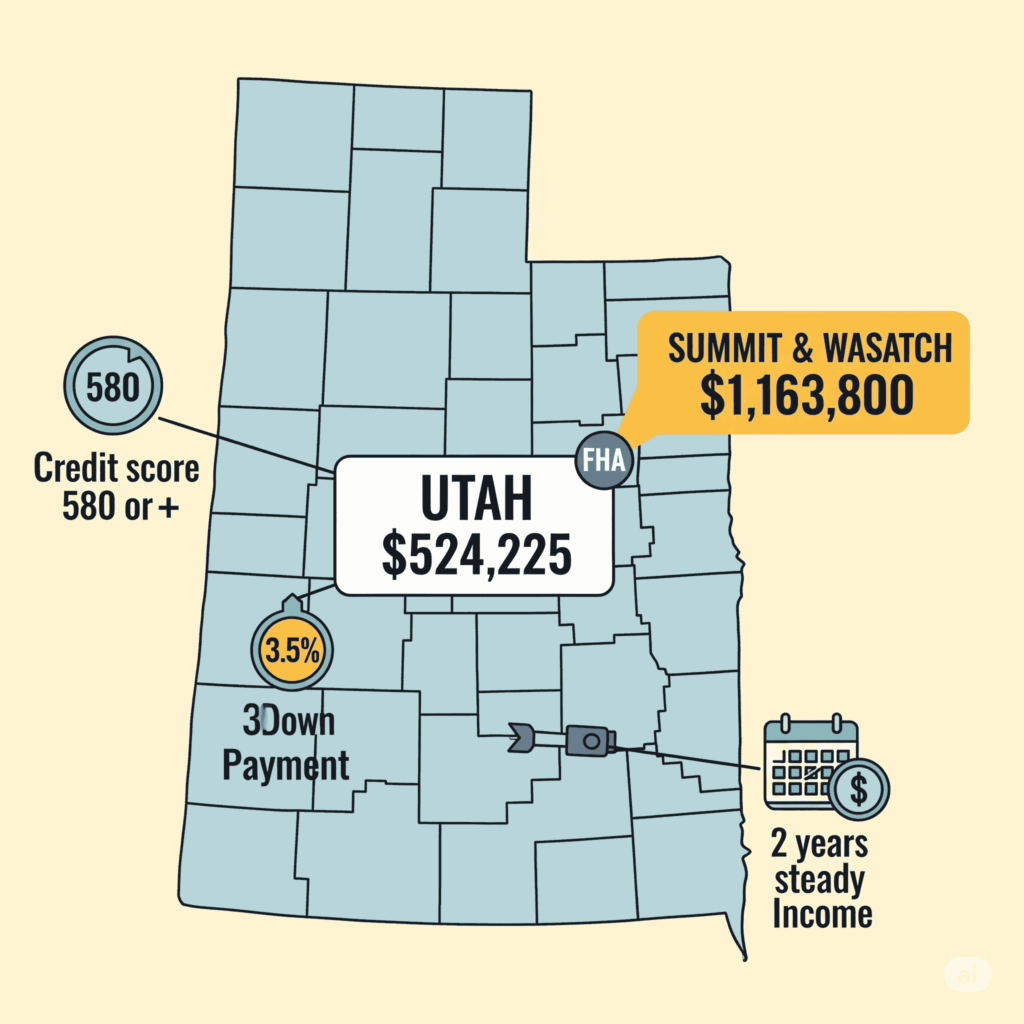

FHA, VA & First-Time Homebuyer Options in Utah

Many Utah buyers, especially first-timers, qualify for government-backed loans with lower down payment requirements. Here’s a quick breakdown:

FHA Loans:

- Minimum credit score: 580 (with 3.5% down)

- Lower income and credit requirements

- Must meet FHA appraisal and property guidelines Federal Housing Administration (FHA) | USAGov

VA Loans (for veterans or active military):

- No down payment required

- No private mortgage insurance (PMI)

- Competitive interest rates

Utah First-Time Buyer Assistance:

- Utah Housing Corporation offers grants and second loans for down payments UHC – Utah Housing Corp

- Other programs provide first-time homebuyer grants or closing cost assistance

- Look into local city or county programs (e.g., Salt Lake City DPA program)

Mortgage Rate Tip: Quote vs Pre-Approval

There’s a difference between getting a mortgage quote and being pre-approved. A quote gives you an estimate based on general info. Pre-approval confirms what you’re actually eligible to borrow after document review.

Want the best of both worlds? Shop for quotes from multiple mortgage lenders—then get pre-approved with your top choice

Common Questions

How do I apply for a mortgage in Utah?

Start by gathering documents listed above, checking your credit, and comparing quotes. You can apply online, in person, or through a broker.

What credit score do I need?

Most lenders require at least a 620 score for conventional loans, but FHA allows for scores as low as 580 with 3.5% down.

Can I buy a home with bad credit?

Yes—home loans for bad credit are available through FHA programs and some local lenders. Expect higher rates and stricter terms.

What if I’m self-employed?

You’ll need at least 2 years of consistent income and detailed documentation. Many lenders offer mortgages for self-employed borrowers.

Ready to Get Pre-Approved?

The mortgage pre-approval process in Utah doesn’t have to be overwhelming. With the right checklist, knowledge of available programs like FHA loan requirements and down payment assistance, and a solid lender or broker on your side, you’ll be positioned to make confident, competitive offers on your dream home.

Use our free mortgage calculator to estimate your payments, then contact one of our trusted Utah lenders for a fast pre-approval. Whether you’re a first-time buyer, self-employed, or exploring options like VA home loans, we’re here to help.

{kind=link}