Buying a home is one of the biggest financial decisions you’ll ever make and understanding how the application for a mortgage is the first step in making it happen. Whether you’re a first-time buyer or looking to refinance or expand your investment portfolio with a commercial mortgage, this guide is tailored to help Utah residents navigate the home loan process.

We’ll walk you through key considerations, calculators, and strategies for finding the best mortgage rates and lenders. From application tips to mortgage calculators, this comprehensive resource covers it all.

Before you get started, it’s important to understand some basic terminology and what the process looks like for different types of borrowers.

What Is a Mortgage and How Does It Work?

A mortgage is a loan used to purchase property. You borrow money from a lender and agree to repay it over time, usually with interest. Mortgages come in many forms, including fixed rate mortgage and commercial mortgage options, depending on your goals.

Check Current Mortgage Interest Rates Before You Apply

Knowing the current mortgage interest rates is crucial before you commit. Rates fluctuate daily, and even a small percentage point difference can cost or save you thousands over the life of your loan. Many buyers seek the lowest mortgage rates or cheapest mortgage rates, but those rates are often reserved for borrowers with strong credit and a solid financial profile.

You can also check out 30 year mortgage rates today to compare longer-term options, which are among the most popular mortgage terms for homeowners.

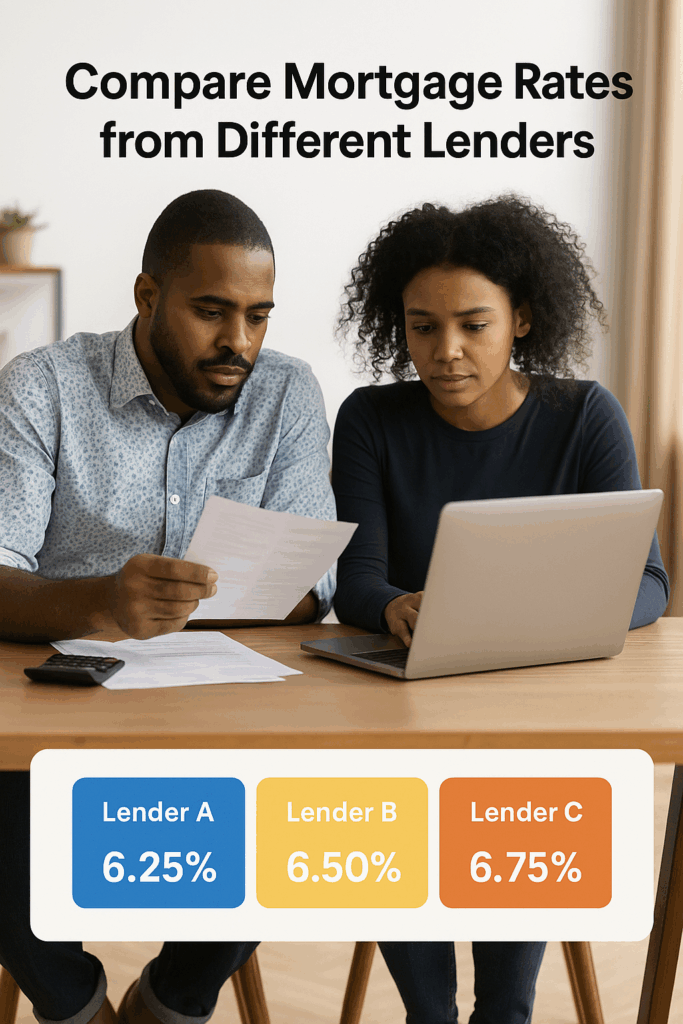

How to Find the Best Mortgage Companies in Utah

Finding the best mortgage companies in Utah can help you secure better terms and a smoother process. Compare lender reputations, rates, and fees. Don’t hesitate to get multiple offers so you can choose the best mortgage rates available to you.

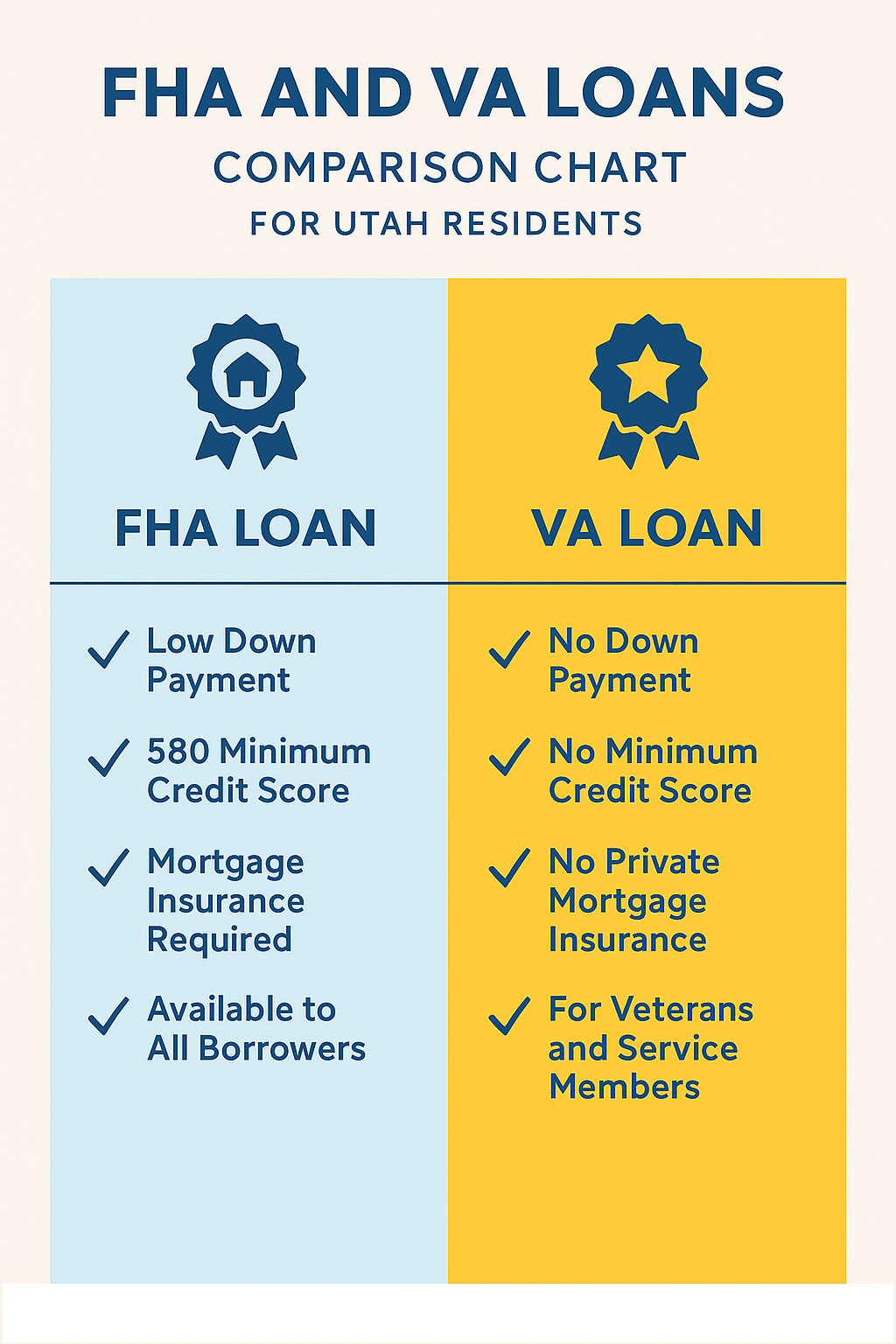

If you’re a veteran, consider a VA mortgage, which offers more favorable terms like lower interest rates and no down payment requirements.

Use Mortgage Calculators to Estimate Your Budget

Before you apply for a mortgage, it’s smart to assess what you can realistically afford. Use tools like:

- Mortgage payment calculator

- Monthly mortgage calculator

- Home affordability calculator

- Mortgage estimator

These calculators help you estimate your monthly payments, how much you can borrow, and how various down payments affect your financial picture.

You can also try a bankrate mortgage calculator or free mortgage calculator for different scenarios.

Prequalify for Mortgage: What You Need to Know

Getting prequalified for mortgage gives you a sense of what a lender might offer you based on basic financial information. This is a key step before house hunting and signals to sellers that you’re a serious buyer.Lenders will review your income, credit score, debts, and assets. From there, they may issue a mortgage approval calculator result or a prequalification letter.

How to Apply for a Mortgage in Utah: Step-by-Step

When you’re ready to apply for a mortgage, be prepared with documentation like pay stubs, tax returns, and bank statements. The mortgage application process can vary slightly by lender, but generally follows these steps:

- Fill out the official loan application.

- Submit all required documents.

- Wait for the lender to underwrite your application.

- Receive a loan estimate and closing disclosure.

- Close the loan.

If you’re a first-time buyer, ask questions about each step. Many lenders offer special first time buyer mortgage programs with lower interest rates, flexible terms, or reduced down payment requirements.

Considering a Commercial Mortgage? Here’s What to Know

If you’re planning to invest in property or start a business, you’ll likely need a commercial mortgage. These differ from residential mortgages in structure, repayment terms, and qualifications. Use a commercial mortgage calculator to determine what type of loan fits your business model.

Review the Average Mortgage Rate and Loan Details

It’s not just about the rate. Pay attention to loan fees, private mortgage insurance (PMI), and any terms that could impact your monthly payments or total loan cost. Check what the average mortgage rate is nationally and locally to compare.

Also, consider whether a fixed rate mortgage works better for your situation than an adjustable-rate mortgage, especially if you plan to stay in your home long-term.

Final Thoughts: Get Started with a Home Mortgage in Utah

Whether you’re exploring options for a home mortgage, investing in real estate, or looking for the best mortgage companies in Utah, being informed is your best tool. Use every resource at your disposal—from calculators and comparison tools to expert advice—to make the best decision.

Understanding how to get a mortgage is a crucial life skill. With the right guidance and preparation, you’ll not only find the best mortgage rates but also gain financial confidence in your decision.If you’re ready to begin your journey, try a mortgage estimator or get in touch with a Utah-based lender today to prequalify for mortgage and take the first step toward homeownership.