Adjustable Rate Mortgage Loan: A Comprehensive Guide for Homebuyers

The journey to homeownership comes with many big decisions, and one of the most important is choosing the right mortgage. While fixed-rate options remain popular for their consistency, the adjustable-rate mortgage loan (ARM) is gaining attention, especially in today’s changing interest rate environment. For many home buyers, an ARM offers a compelling, cost-effective alternative, but understanding how it works is essential to making a sound decision.

Understanding Your Adjustable Rate Mortgage Loan

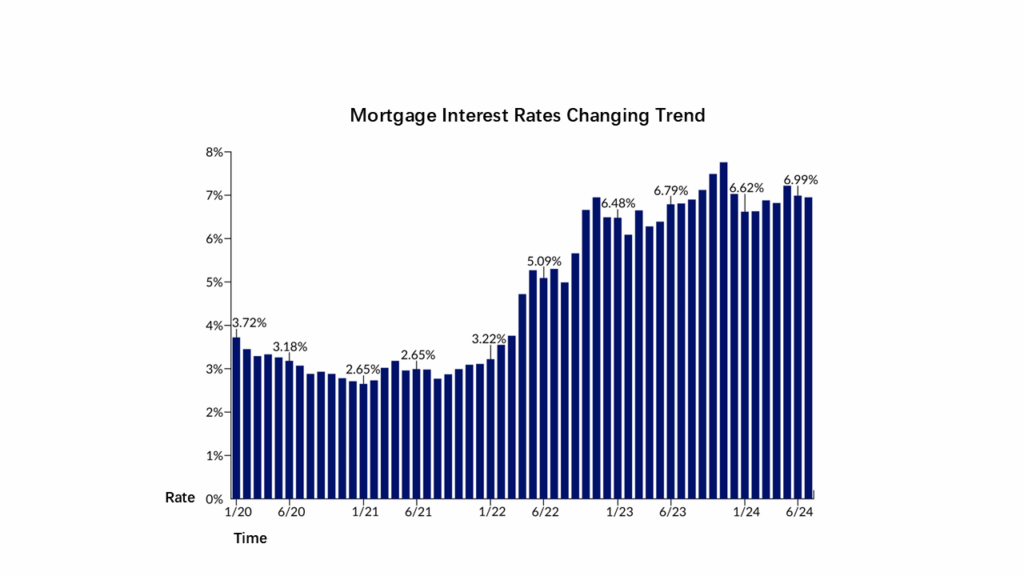

At its core, an adjustable-rate mortgage loan is a home loan with an interest rate that changes over time, usually after an initial fixed-rate period. This means monthly payments can go up or down depending on market trends. Staying informed about adjustable-rate mortgage rates today is essential for buyers exploring this option.

Unlike a fixed-rate mortgage, where the interest rate stays the same, ARMs typically start with a lower rate, making homeownership more affordable in the early years. This can be especially beneficial if you plan to sell or refinance a house before the rate adjusts. For example, if a job relocation or life change is on the horizon, or if you believe you’ll qualify for better terms down the road, an ARM could lead to substantial savings on interest in the early years. Still, it’s important to weigh the potential for higher payments later in the loan term.

Leveraging the Adjustable Rate Mortgage Calculator and Payment Strategies

Understanding how an ARM affects your finances is crucial, which is where an adjustable rate mortgage calculator becomes incredibly helpful. These calculators model various rate scenarios and help estimate future monthly payments, giving you a clearer picture of what to expect and allowing you to plan ahead.

To reduce the overall cost of your mortgage, use an additional mortgage payment calculator to explore how even small extra payments can lower your principal faster. Pairing this with strategies like accelerated weekly mortgage payments or using an accelerated mortgage payoff calculator can make a noticeable difference. Over time, consistent proactive payments can significantly cut down the length of your loan and reduce total interest, whether you have a fixed-rate or adjustable loan.

If market conditions shift or your personal financial situation changes, you might consider an adjustable-rate mortgage refinance. This option replaces your current ARM with a new loan, often a fixed-rate one, to lock in predictable payments or take advantage of lower interest rates. It’s a strategic move that many homeowners use to gain long-term stability and peace of mind. For more on this approach, check out the US News’ article on refinancing, which offers helpful insights.

Navigating Mortgage Approval and Diverse Loan Options

Beyond the type of loan, securing mortgage approval is a multi-step process. If you’re wondering about the best way to get approved for a home loan, start by maintaining a solid credit history, stable income, and a low debt-to-income ratio. Checking offers from academy mortgage rates or comparing what a popular bank mortgage might provide gives you a sense of where you stand in the market. It’s also worth looking into what a good mortgage company can offer and reviewing rates from a top 10 bank for a home loan to ensure you’re getting the most competitive deal.

For buyers facing credit challenges, working with an adverse mortgage lender or an adverse credit mortgage broker could open doors. These specialists help individuals with poor credit histories explore mortgage opportunities, such as an affordable loan solution mortgage, which offers more flexibility for those in unique financial situations. Older homeowners may also benefit from specific options like those provided by AARP reverse mortgage lenders, though it’s important to note that reverse mortgages differ significantly from standard purchase loans and are tailored to senior borrowers.

From Pre-Approval to Closing: What to Expect Next

After receiving pre-approval, the path to closing begins. The steps to buying a house after pre-approval include selecting a home, submitting an offer, and moving through the underwriting process. After getting pre-approved for a mortgage, it’s essential to maintain financial discipline. Many wonder about what’s allowed after pre approval mortgage status or whether applying for credit after mortgage offer is okay. Lenders typically recommend avoiding new credit lines during this period, even if you’re thinking, “after closing on a house can I apply for credit?” The answer is, it’s safest to wait until the deal is fully closed.

Knowing how long it takes from a mortgage application to approval can help ease anxiety; timelines vary, but clear communication with your lender will help you stay on track. Following each of the steps after pre approval with care keeps your loan moving smoothly toward closing.

In conclusion, an adjustable rate mortgage loan can be a smart, flexible option for certain homebuyers, especially those who value lower upfront costs and plan to move or refinance within a few years. But understanding the mechanics, planning for rate changes, and using the right tools like calculators and refinance strategies are key. With thoughtful research and smart planning, you can approach homeownership with confidence and clarity. For more financial guidance, visit Investopedia.