Looking to learn more information about First-time Home buying quicker, and from those living around you about their thoughts? Follow these links below to solve some of your commonly asked questions.

First-Time Homebuyer Grants and Assistance Programs in Utah

If you are a first-time home buyer that is looking for assistance programs for down payments, closing costs, or to reduce your interest rate. ClickHEREto find more programs that can help assist you in this journey.

Utah’s 3 Best Neighborhoods to Live in

Exploring Utah’s neighborhoods can be an exciting adventure, especially for first-time home buyers. Here are the top three of the best areas to consider living in. Click HERE to find out more.

Best School District of First Home Owners

If you are a first-time home buyer in Utah, choosing a house with excellent schools is a top priority. There are several districts in Utah that stand out for their quality of education and support for students. Click HEREto find out more.

Pros and Cons of Buying a Condo vs. a Single-Family Home in Utah

Deciding between a single-family home and a condo can be challenging in Utah, here are some things to consider. ClickHERE to find out more.

Top 3 Affordable Suburbs of Salt Lake City

Want to buy a home near SLC? There are plenty of options to consider when looking for affordable housing. Click HERE to find out more.

What does a Home Inspection Cover in Utah

If you want to find out more about what an inspector is looking at, and why you should have them look at your house you are moving in, clickHEREto find out more and see what other people think too.

When my husband and I purchased our first home in Salt Lake City, Utah, it seemed like there were endless forms to fill out and too many documents to sign, followed by at least an hour of signing more closing document to wrap up the sale. The amount of paperwork involved with buying a home feels endless. However, It’s important to know what documents you’re signing at closing, and why you’re signing them because purchasing a home is a huge investment!

Don’t drown in closing document confusion! Read on for help.

I want to help first-time homebuyers understand what they’ll be reviewing during closing, and/or give experienced homebuyers a friendly reminder. So, below is a list of the most common closing documents you’ll encounter and a brief description of what they entail. Documents are in order alphabetically, by name.

The Affidavit of Title

The Affidavit of Title is a legal document which establishes that the seller holds the title to the property. The new homeowner will sign this document upon taking ownership. Also, it includes any information about liens or other title issues for that property.

The Certificate of Occupancy

The Certificate of Occupancy is a document that’s provided to the homebuyer and contains the address and description of the property. It verifies that it us up to code, which serves as proof that the property is fit to live in and fit for its purpose. This document only applies to new-build homes, therefore anyone closing on an existing home doesn’t need to worry about this one.

The Closing Disclosure

A Closing Disclosure is a form for the new homebuyer which gives the final details of the mortgage loan. It includes the loan terms, projected monthly payments, and how much the new homebuyer will pay in fees and other costs to get the mortgage (closing costs).

The Deed

A Deed is a legal document that transfers ownership of home from the current owner to the new buyer. It also contains a description of the property boundaries and any real property that it contains. Therefore, it is crucial to review this document for accuracy. Every real estate deed must be notarized and filed with the local government in order for the new homebuyer to sell the property, refinance the property, or obtain a line of credit on it. The title insurance company generally performs this task, but it’s important for the homebuyer to verify the process.

The Home Inspection Report is a detailed list of the the condition of the home and its components. It generally includes the following: foundation, exterior, bathroom fixtures, appliances, roof, plumbing, HVAC system, gas system, and electrical system. An inspector will visually examine the home and then provide the report. This is done prior to closing so that the buyer can review the document and request fixes to be made or even change their mind about purchasing the property.

The Homeowners Insurance

Lenders in Utah require homeowners insurance, and will ask for proof of insurance as one of the closing documents. Lenders want proof that their investment is protected.

The Initial Escrow Statement

The Initial Escrow Statement also goes by the name of the “Initial Escrow Disclosure”. This document outlines how the escrow account is set up and what expenses it covers. It covers common elements such as property taxes, mortgage insurance, homeowners association dues, etc.

The Loan Application

The Loan Application is the homebuyer’s acknowledgement that they understand the terms of the loan and their financial obligation to repay it. The new homebuyer will review this document along with the mortgage application. Therefore, it is important to review for accuracy and notify of any changes.

The Mortgage

The mortgage also goes by the name “The Deed of Trust.” This is an agreement between the new homebuyer and a lender that allows the homeowner to borrow money to purchase or refinance a home. The mortgage legally allows the lender to put the home up as collateral for the loan.

The Promissory Note describes the homebuyer’s commitment and responsibility to the mortgage loan. It will state the amount of the loan, the interest rate, repayment schedule and any consequences of defaulting.

The Purchase Agreement

The Purchase Agreement is sometimes called a “Purchase and Sale Agreement” or a “Real Estate Purchase Contract (REPC)”. It is a legally binding document between the buyer and seller for real estate purchases. The Purchase Agreement contains details such as: new homebuyer info, purchase date, purchase price, purchase details (property and any included amenities), how it will be paid for (loan, cash, etc.) It also contains details such as appraisals, conditions of purchase, etc. Utah law requires licensed Real Estate agents to use the REPC form, although the home buyer and home seller can agree to alter or delete its provisions, or to use a different form.

The Sellers Disclosure

The Sellers Disclosure is a document that lists in detail any issues with a home. In the state of Utah, a seller is required by law to disclose material defects and latent defects. Material defects are things you can easily see or find. Latent defects are not easily seen or not obviously apparent.

The Title Document is a list of all previous owners of the home and any liens or other clouds on the title. You’ll need to pay off any additional/existing liens in order to have a free and clear title. It’s important to review this document to prevent delays in the closing process. When you buy a home, you acquire the title, which represents your ownership rights.

The Title Insurance Policy

The Title Insurance Policy is a document that outlines protections for the lender. Hidden title hazards can emerge after purchasing a home, but title insurance can offer protection against them.

The Transfer of Tax Declaration

The Transfer of Tax Declaration is a document that lists the taxes owed for the transfer of the property. Utah does not charge a real estate transfer tax, therefore this is not a concern for Utah homebuyers as it is not a required closing document.

Thanks for Reading!

I hope this article was helpful! Now you’ve seen a quick summary of the closing documents you’ll encounter when buying a home. Also, depending on which state you’re purchasing a home in, there may be more or fewer documents to sign. If you want more details or additional information, then please check out these posts as well!

Great! You’ve decided to set roots in Utah, the land of stunning landscapes and vibrant communities. But before you picture yourself sipping tea on a cozy porch overlooking the Wasatch Range, there’s the hurdle of navigating the home-buying journey. This guide will provide a one-stop shop for buying a home in Utah real estate market.

Utah is known for its stunning landscapes, strong economy, and family-friendly communities. Here’s why buying a home in Utah could be one of the best decisions you make:

Booming Economy: Utah boasts a robust job market, particularly in tech and healthcare, which makes it a prime location for career growth and stability.

Outdoor Lifestyle: From skiing in Park City to hiking in Zion National Park, outdoor enthusiasts will find plenty to love. Utah’s natural beauty offers numerous recreational opportunities year-round.

Family-Friendly: With excellent schools and safe neighborhoods, Utah is a great place to raise a family. Communities are designed to be welcoming and supportive, making it an ideal place for young families.

Understanding the Utah Real Estate Market

The Utah real estate market is unique and has its own set of trends and characteristics:

Growth Areas: Salt Lake City, Provo, and St. George are some of the fastest-growing areas, attracting new residents due to their vibrant economies and desirable living conditions.

Price Trends: While prices have been rising, there are still affordable options, particularly in emerging neighborhoods across the valley. This offers opportunities for both first-time homebuyers and those looking to invest in real estate.

Overlooking shot of St. George, Utah. (Courtesy of Livability)

Utah Home Buying Statistics

Understanding the current market statistics can help you make informed decisions:

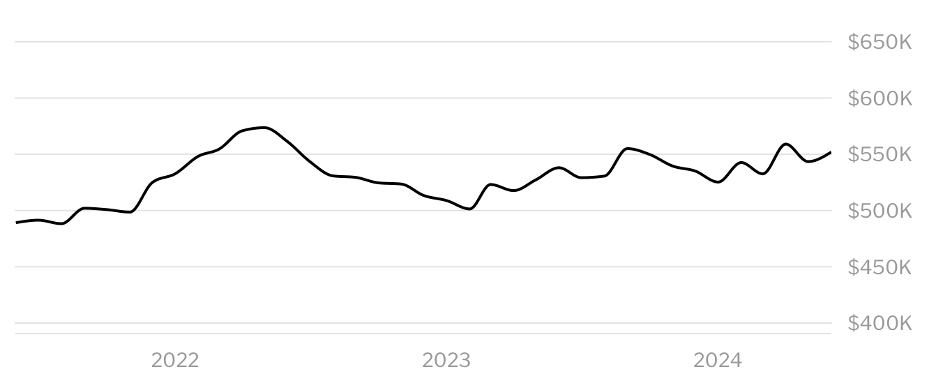

Statistics about Utah Home Buying

Average sale price of homes in Utah (June 2024) [i]

The Economy: Utah boasts a healthy economy, but buying a home requires sound financial planning. In June 2024, 26.6% of homes in Utah sold above list price[iv], which is something to consider when putting in an offer for a home. On the other hand, property tax rates in Utah are low. Utah has the sixth lowest property tax rate in the country at 0.55%.[v]

Getting a Mortgage: Whether you have 3% to put down on a home or 20%, finding the right lender is critical. We’ll explore top Utah lenders offering competitive rates and programs tailored to first-time homebuyers or specific needs.

Finding a Real Estate Agent: A solid real estate agent who will advocate for you in your Utah home buying journey is critical. We’ll discuss the benefits of working with an agent, along with tips for finding the perfect match who understands your needs and the local market.

Once you understand some of the important financial information, you can look at some important considerations for first-time homebuyers to make sure you’re well-prepared.

Tips for First-Time Homebuyers in Utah

Consider State Programs: Utah offers various first-time homebuyer programs and grants. Visit the Utah Housing Corporation for more information.

Budget for Closing Costs: In addition to your down payment, budget for closing costs, which can include fees for inspections, appraisals, and title insurance.

Research Neighborhoods: Take the time to research and visit different neighborhoods to find the one that best suits your lifestyle and needs.

Make sure to look into down payment assistance and loan programs that you may qualify for!

Utah Down Payment Assistance and Loan Programs

Programs

FirstHome

FHA or VA Mortgage

Conventional HFA Advantage Loan

Qualifications

– First time homebuyer – 660 or higher credit score

– Previously owned a home or first-time homebuyer – 620 or higher credit score

This program typically has lower purchase price and income limits and lower interest rates.

Homebuyers can purchase residence with up to 2 units

Financing option for this loan might have a higher interest rate but a lower mortgage insurance costs, which might result in a lower monthly payment.

Source: Down Payment Assistance and Loan Programs. (2023). In Utah Housing Corporation. Utah Housing Corporation. Retrieved July 18, 2024, from https://utahhousingcorp.org/pdf/Form211.pdf

Now that you have all of the information, you are ready for the next steps.

Next Steps to Buying Your Utah Home!

Take the next steps to buying your home!

Get Pre-Approved for a Mortgage

What are today’s mortgage rates in Utah? Check them out here.

Remember: interest rates will vary by lender and by borrower, depending on factors like credit score, loan program, down payment, etc. Compare quotes from at least 3 different lenders to make sure you’re getting the lowest rate.

Ask about down payment and closing cost assistance.

Partner with a knowledgeable real estate agent who knows the Utah market. Consider agents from reputable firms like Coldwell Banker and Re/Max.

Make sure they’re licensed, read reviews, ask questions about how they will help you, and trust your instincts to find the right person to help you buy your home.

[iii] GOBankingRates. (n.d.). The average credit score in each state — see where your state ranks. Nasdaq. https://www.nasdaq.com/articles/the-average-credit-score-in-each-state-see-where-your-state-ranks#

[v] Pitts, E. (2024, February 22). Some states have more affordable property taxes than others. Where does Utah rank? Deseret News. https://www.deseret.com/utah/2024/2/20/24078329/state-ranking-property-tax-value-utah-housing-market/