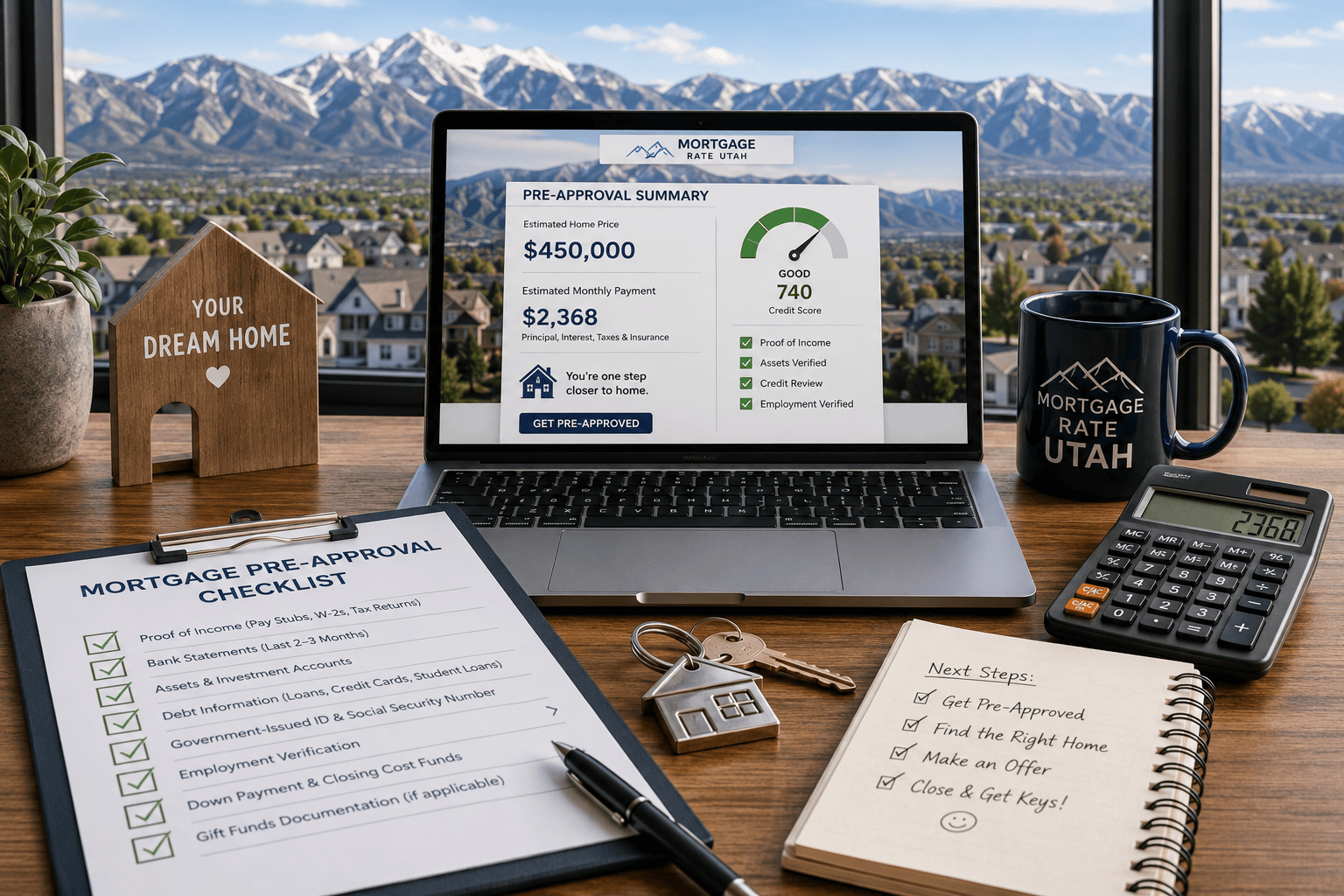

Mortgage Pre Approval Checklist: The Smart Way to Get Approved

Mortgage Pre Approval Checklist: Everything You Need Before Applying Getting ready to buy a home is exciting, but it can also feel overwhelming if you …

Mortgage Pre Approval Checklist: Everything You Need Before Applying Getting ready to buy a home is exciting, but it can also feel overwhelming if you …

Navigating the changing real estate landscape in the Beehive State requires keeping a close eye on shifting macroeconomic indicators. For thousands of local families, the …

How to Refinance Your Mortgage in Utah Refinancing your mortgage means replacing your existing home loan with a new one, ideally one with better terms. …

Understanding current mortgage rates Utah can be the difference between saving thousands or paying more than you should for your home. Whether you’re a first-time buyer or …

First of all, what does it mean to refinance? The process of refinancing has the goal of replacing a homeowners existing mortgage with a new …

What is Refinancing? Mortgage refinancing is a financial strategy that allows homeowners to replace their existing mortgage with a new, more favorable loan. Many homeowners …