Thinking about buying a home in Utah in 2025? Learn about first-time buyer programs, local mortgage rates, refinancing options, and expert tips to make your journey smoother.

Is 2025 Your Year to Buy a Home in Utah?

If you’re thinking about buying a home in Utah in 2025, chances are you’ve got a lot on your mind. Maybe it’s your first time, and you’re just trying to understand where to begin. Or maybe you already own a home and are wondering whether this is the right year to refinance or invest in a second property.

Wherever you are in the process, you’re not alone—and you don’t have to figure it all out at once.

We’ve pulled together this guide to help you feel more informed and confident—whether you’re comparing Utah mortgage rates today, researching first time home buyer Utah programs 2025, or trying to connect with the best mortgage companies in Salt Lake City.

First Time Buyer? Let’s Talk Programs and Loan Options

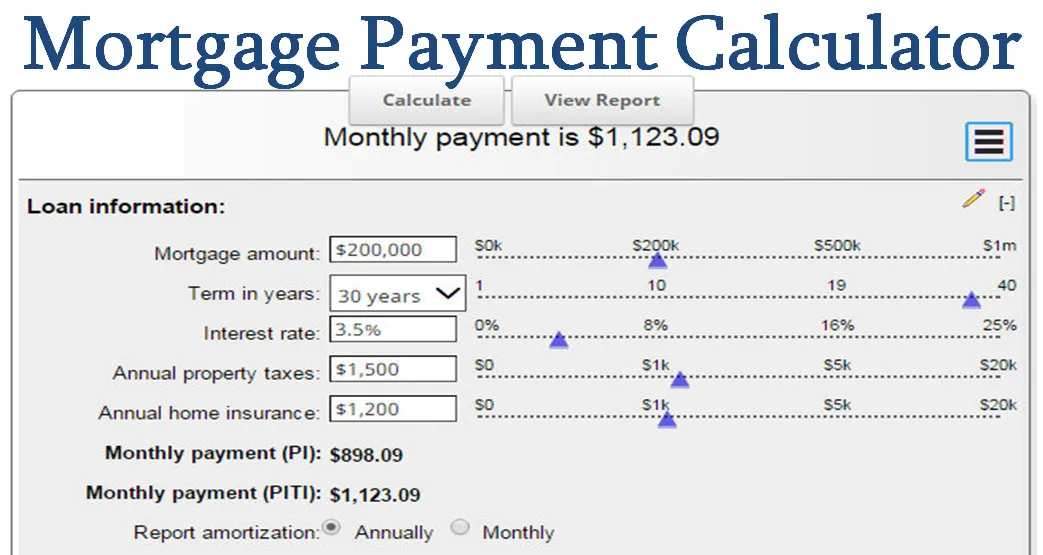

Being a first-time buyer can feel overwhelming, but Utah offers a surprising amount of support. Through first time home buyer programs 2025, you may qualify for lower rates, better terms, and even down payment assistance to make buying your first home more affordable.

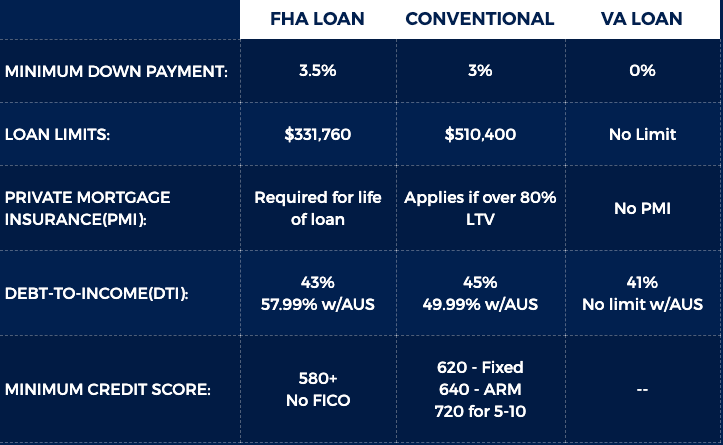

You’ll want to explore first time home buyer loan options, which might include FHA, VA, or conventional loans tailored for first-time buyers. Each has pros and cons, but a good lender will help you find the best mortgage for first time home buyer situations based on your income, credit, and goals.

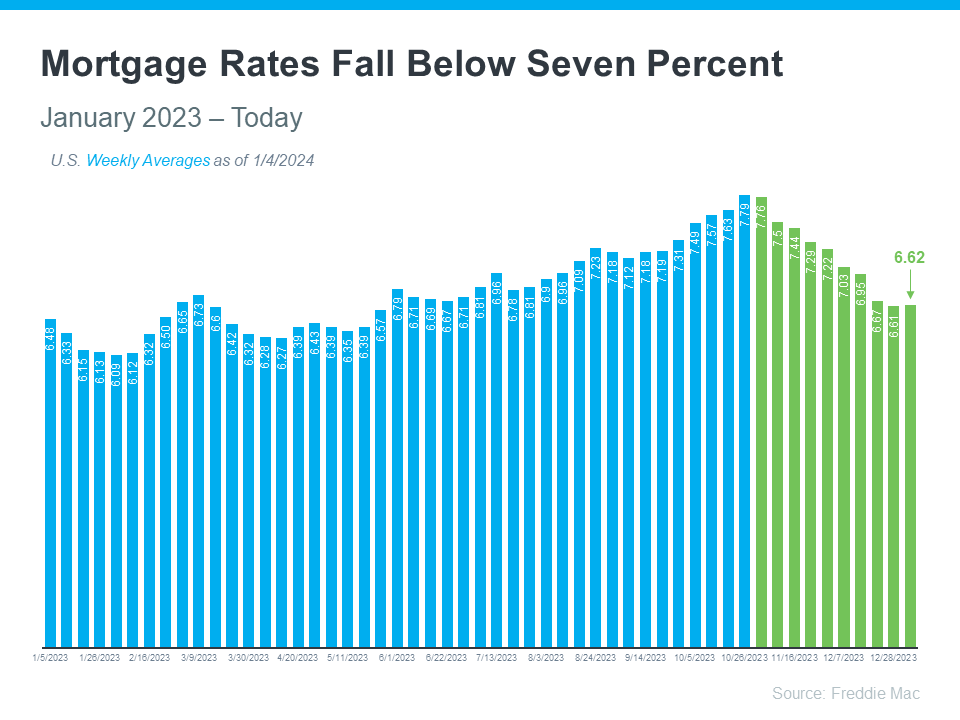

What’s the Market Like Right Now?

The housing market is shifting, but it’s not as scary as headlines make it sound. Utah mortgage rates today are still in a relatively stable place, and that means there are real

opportunities if you’re ready.

Loan thresholds have also changed. The FHA loan limits Utah 2025 increase allows you to borrow more while still qualifying for a government-backed mortgage. For veterans, VA loan lenders in Utah remain a strong option with zero down and competitive rates.

Working With Local Experts Makes a Difference

While big banks have their place, local expertise matters—especially in today’s market. A mortgage broker Ogden Utah or a mortgage lender Sandy Utah can offer advice that’s grounded in local market knowledge.

Don’t forget about credit unions. Many buyers find better terms through the best Utah credit unions for mortgages, especially when it comes to customer service and flexible underwriting.

Already Own a Home? It Might Be Time to Refinance

If you’ve been thinking about refinancing, 2025 could be your moment. Whether you want to lower your payment or tap into equity, the best place to refinance a mortgage in Utah might be right around the corner—or even your local credit union.

You might also consider a HELOC. Researching the best banks for HELOC in Utah can help you fund renovations, cover college tuition, or consolidate debt—all with more flexibility than a traditional loan.

What If You’re Not Ready to Buy?

Not everyone is ready to commit to a mortgage just yet. For those looking for a more gradual path to ownership, rent to own homes Utah offer a hybrid option—letting you live in the home while working toward ownership.

Others may be exploring investment property mortgage rates, especially with rental demand rising across the state. Or, if you’re dreaming of a mountain getaway, just make sure you’re up to speed on second home mortgage rules, which have stricter requirements than primary residences.

Planning to Buy a House in Utah in 2025?

Whether you’re gearing up for your first purchase or adding to your real estate portfolio, buying a house in Utah 2025 doesn’t have to be overwhelming. With the right programs, a trustworthy lender, and a little guidance, you can make smart choices that work for your budget—and your future.

From first time home buyer down payment assistance to investment property mortgage

rates, the tools are out there. All you need is the right roadmap.