How to Find the Best Mortgage Rates Utah Has to Offer

Buying a home is a major milestone—especially for a first-time home buyer in Utah. Understanding how mortgage rates in Utah work is key to making smart, long-term financial decisions.

While national averages provide a general idea, the current mortgage rate in Utah depends on local housing demand, lender competition, and economic trends. By comparing multiple Utah mortgage lenders, you can secure the best mortgage rates Utah and save thousands over your loan’s lifetime.

Why Compare Mortgage Rates in Utah?

When you’re searching for a home loan in Utah, it’s not enough to rely on national numbers—you need local mortgage rate comparisons. Even a small change in your rate can greatly affect your monthly payment and total interest paid.

Working with an experienced mortgage broker in Utah helps you compare offers from various lenders, identify flexible loan options, and find the best mortgage company Utah for your financial goals.

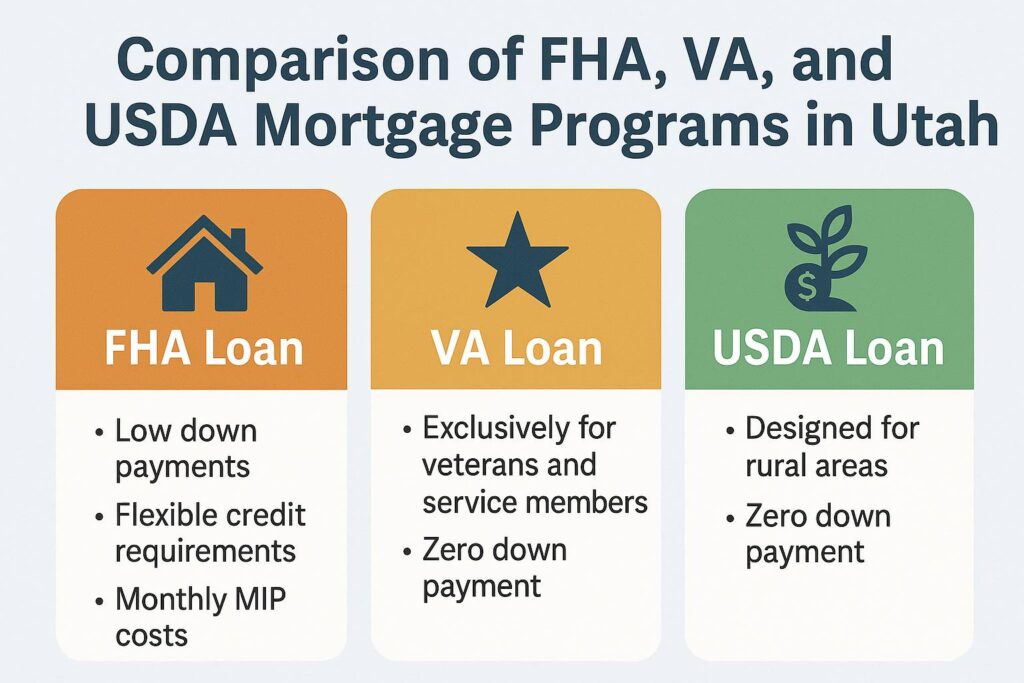

If you’re searching for a mortgage broker near me, local experts can analyze fixed vs. adjustable loans, guide you through FHA programs, and help you qualify for first-time home buyer loans with zero down in Utah.

Learn More about our Utah mortgage broker services: Best Mortgage Rates Utah | Home Loans, VA Lenders & First-Time Buyer Programs Stay updated with – freddiemac.com: Best Mortgage Rates Utah | Home Loans, VA Lenders & First-Time Buyer ProgramsFinding the Best Mortgage Company for First-Time Buyers

The best mortgage lenders in Utah offer more than low rates—they deliver personalized service and expert guidance. For a first-time home buyer Utah, that support makes a huge difference.

Partnering with the best mortgage company for first-time home buyers Utah ensures you receive help from pre-approval to closing.

For veterans, VA mortgage rates Utah often come with even better terms. The best VA loan lenders Utah offer flexible credit requirements, no private mortgage insurance, and dedicated support for service members.

Many national lists recognize the top-rated VA mortgage lenders Utah for their exceptional service and specialized loan products.

First-Time Home Buyer Programs and Down Payment Assistance

One of the biggest challenges for new buyers is saving for a down payment. Thankfully, first time home buyer programs Utah exist to bridge that gap. Many include down payment assistance programs Utah, which can reduce or even eliminate upfront costs. Some lenders also provide first time home buyer loans with zero down Utah, making it easier to purchase a home without waiting years to save.

To make the most of these opportunities, work with the top mortgage lenders Utah who specialize in pairing clients with programs like those offered by the Salt Lake City Housing Authority. These lenders are often also recognized as the best mortgage lenders for first time home buyers Utah, because they ensure you don’t miss out on state and federal resources.

Check out USA.gov – Buying a Home for nationwide programs.: Best Mortgage Rates Utah | Home Loans, VA Lenders & First-Time Buyer Programs Check out haslcutah.org – Housing Authority of Salt Lake City: Best Mortgage Rates Utah | Home Loans, VA Lenders & First-Time Buyer Programs

Steps to Secure the Best Mortgage in Utah

- Review your credit score – A higher score often qualifies you for lower mortgage rates Utah.

- Compare lenders – Look at offers from banks, credit unions, and Utah mortgage brokers.

- Check eligibility – Apply for first time home buyer programs Utah or grants if you qualify.

- Explore loan types – From FHA to VA loans, find the best fit for your situation.

- Lock your rate – Once you find the best mortgage rates Utah, secure them quickly to avoid market changes.

Final Thoughts

Finding the best mortgage rates Utah doesn’t have to be overwhelming. With the right strategy, you can compare offers, take advantage of first time home buyer programs Utah, and explore down payment assistance Utah to make homeownership achievable. Whether you’re a first time home buyer Utah or a veteran looking for the best VA loan lenders Utah, working with trusted professionals ensures you’ll get the best home loan rates Utah for your future.