Your Complete Guide to Rates, Lenders, and Tools

Navigating the mortgages application process can feel overwhelming, especially for first-time homebuyers. With numerous options, terms, and fluctuating mortgage rates, it’s essential to be informed before making any decisions. Whether you’re just starting to explore how to get a mortgage or ready to compare mortgage quotes, this guide will walk you through every step, using the tools and insights you need to make smart financial decisions.

Understanding Mortgages and the Application Process

The first step in home buying is understanding the mortgage application process. This process involves submitting financial documents, verifying your income, obtaining a credit report, and selecting a loan product that best suits your needs. A “mortgage broker near me” can often assist in navigating the paperwork and connecting you with potential lenders.

When comparing lenders, it’s a good idea to read mortgage lender reviews. These reviews offer insight into real customer experiences and can help you find the best mortgage lenders for first-time buyers who may need extra support and educational resources.

Tools to Help You Calculate and Compare Mortgages

Knowledge is power, and with so many tools available online, it’s easier than ever to evaluate your options. A mortgage calculator is one of the most valuable resources. This tool helps you estimate monthly payments based on principal, interest, and loan term.

There’s also the mortgage payment calculator, mortgage loan calculator, and mortgage rate calculator, each designed to give you a more detailed look at how specific rates, terms, and loan amounts will affect your monthly budget.

If you’re just beginning your home search, a mortgage estimator can give you a quick sense of your potential loan amount based on income and debt levels. These calculators are often found on lender websites and are a must-use for smart planning.

Comparing Mortgages and Their Rates

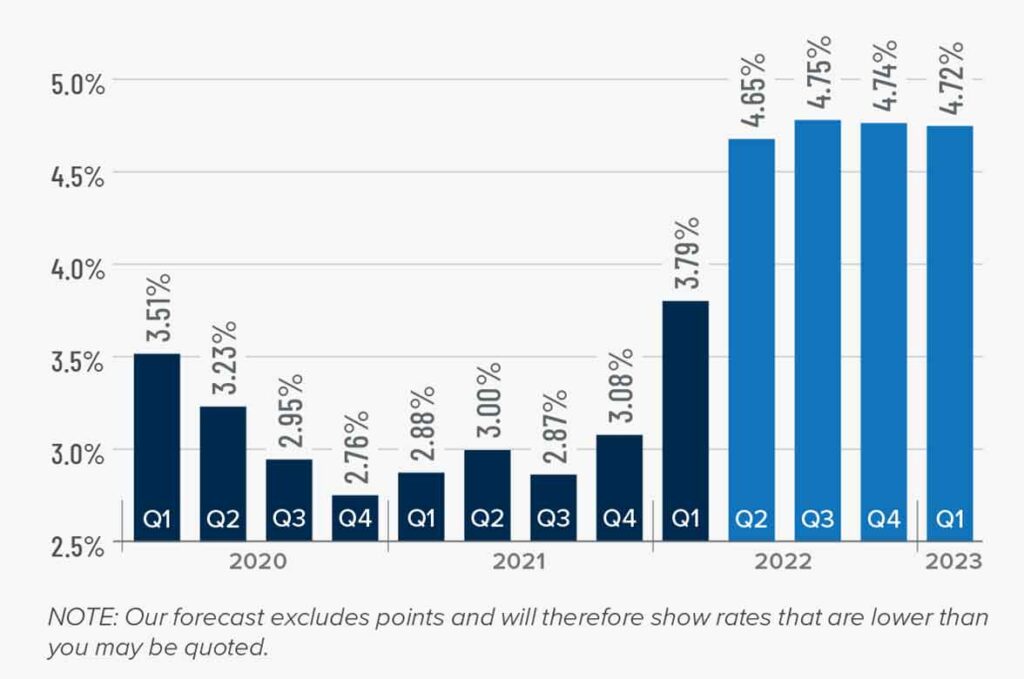

One of the most important factors when choosing a lender is the mortgage interest rate. This determines the cost of borrowing over time. Today’s rates can vary widely between lenders, so it’s important to shop around.

Check out mortgage rates today using online comparison tools or contact a “mortgage broker near me” who can compile current offers. If you’re wondering what a good deal looks like, look up the average mortgage rate as a benchmark.

Sites that offer a mortgage comparison feature allow you to view offers side by side, a great way to spot differences in closing costs, APRs, and more.

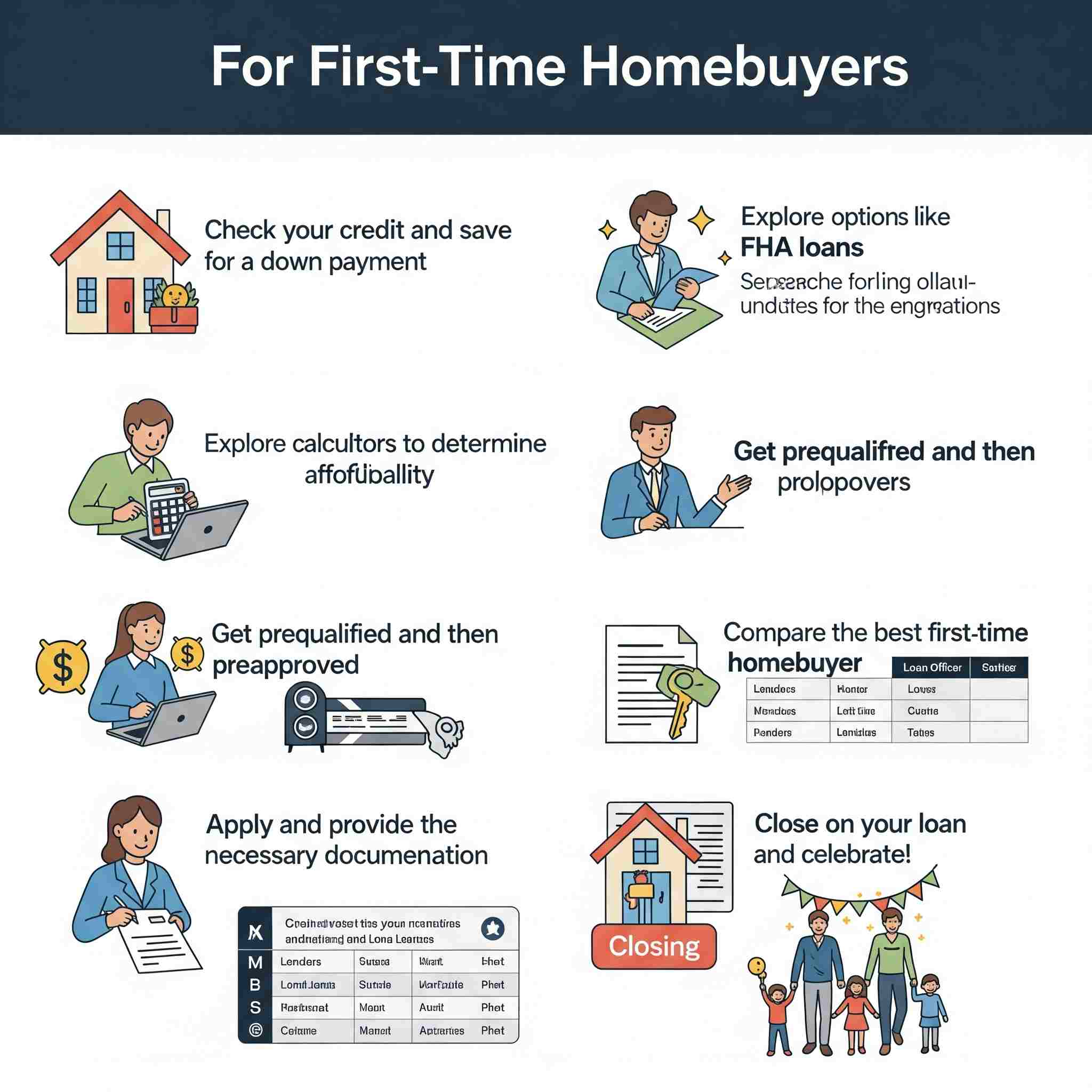

Getting Pre-Qualified and Pre-Approved for Mortgages

One way to strengthen your position as a buyer is to pre-qualify for a mortgage. This is a basic financial check that shows you’re serious and gives you a ballpark figure for your budget.

Once you’ve pre-qualified, it’s smart to get pre-approved. This required more documentation, but it puts you in a stronger position when making offers. It shows sellers that you’ve already passed a lender’s initial review.

Finding the Right Lender

Choosing a lender isn’t just about the lowest mortgage rates today; it’s about trust, support, and flexibility. Look for “mortgage companies near me” that offer personalized service, or go national if you want access to digital tools and fast underwriting.

There are many mortgage companies to choose from, so take your time researching. Don’t just go with the first bank that pre-approves you. Read mortgage lender reviews, compare quotes, and make sure you understand the terms.

The Power of Shopping Around

Rates can vary by lender and even by location. Whether you’re comparing home mortgage rates, mortgage loan rates, or looking for the best mortgage rates on the market, cast a wide net.

Online lenders often offer highly competitive rates, while local lenders may provide more hands-on service. Always request multiple mortgage quotes; even a small difference in interest rate can translate into tens of thousands of dollars over the life of the loan.

Today’s Market: What to Know

In today’s housing market, current mortgage interest rates are affected by inflation, Federal Reserve policy, and broader economic trends. Use real-time tools to track mortgage rates today, and don’t hesitate to lock in a rate if you find a favorable offer.

It’s also helpful to understand what drives the average mortgage rate nationally and regionally. This context can help you decide when to act and when to wait.

Final Thoughts: How to Get a Mortgage That Works for You

If you’re asking yourself how to get a mortgage, the answer starts with preparation. Know your credit score, gather your financial documents, and use every tool at your disposal, from the mortgage calculator to the mortgage comparison platforms, to make the most informed choice.

Whether you’re a first-time buyer or refinancing, the right combination of planning, research, and expert advice will help you secure the best possible loan. Remember: the best mortgage isn’t just the lowest rate, it’s the one that fits your financial goals and lifestyle.

By using all available tools, from the mortgage loan calculator to lender comparison websites, and educating yourself on today’s mortgage rates, you’re well on your way to homeownership success.

Everything You Need to Know About Mortgages: Your Complete Guide to Rates, Lenders, and Tools