Buying a home is one of the most important financial steps you’ll ever take, and the first thing you need is information. With the right tools—like a mortgage calculator free, mortgage estimator based on income, or mortgage estimator tool—you can confidently plan your next move in Utah’s competitive housing market. Whether you’re a first-time buyer, investor, or planning to refinance with bad credit, we’ve gathered everything you need to make smarter decisions. Use our free mortgage estimator to be up to date on Utah Home Loan tools and advice.

Mortgage Estimator Tools Every Buyer Should Use

Before you reach out to a lender, use a free mortgage estimator tool to estimate your monthly payments. Most calculators allow you to input your down payment, loan term, and interest rate. More advanced platforms like the mortgage estimator Zillow or a mortgage estimator based on income offer deeper insights based on your salary and debt ratio.

Want to go deeper? Try a how much mortgage can I afford calculator to know your exact buying power before you apply online.

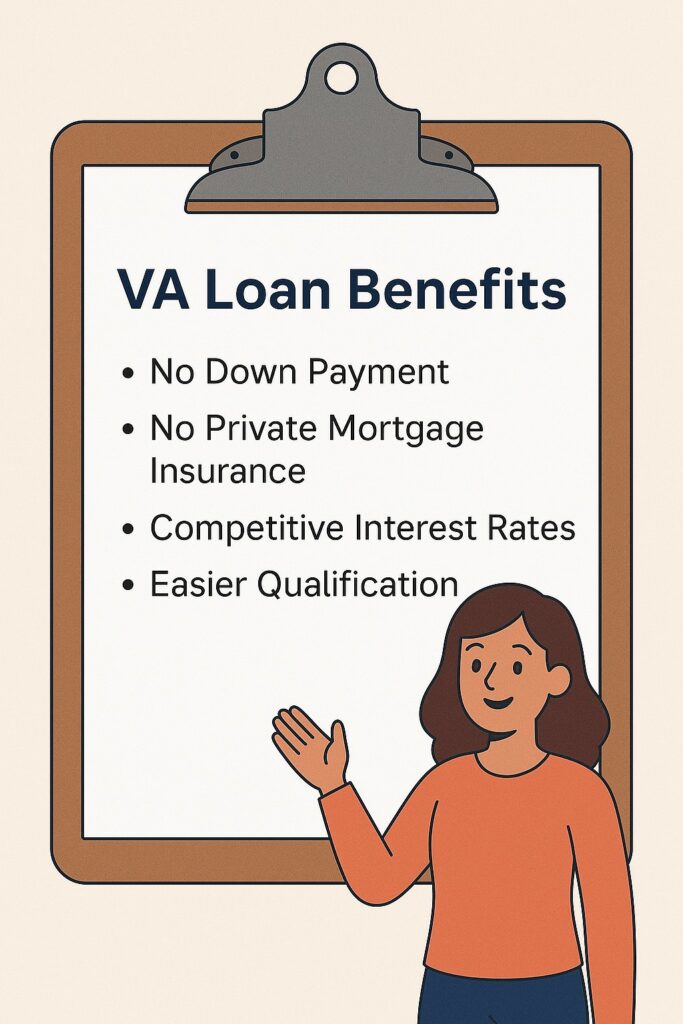

First-Time Buyers: Mortgage Tips for Utah Residents

Shopping for a mortgage for first time buyers in Utah? You’re in luck. There are dozens of home loan assistance [state] programs that offer grants, lower down payments, or reduced closing costs. To find the best mortgage for new home buyers, look for fixed-rate terms, low fees, and flexible credit requirements.

Don’t forget to learn how to qualify for a mortgage first time buyer. Most programs require proof of income, job stability, and sometimes a credit score over 620.

Refinancing Your Home, Even with Bad Credit

Many Utah homeowners benefit from a refinance, whether to lower monthly payments or change loan terms. Start by comparing mortgage refinance rates and learning how to refinance my mortgage based on your goals. Even with poor credit, refinance with bad credit options exist.

The key is working with the best lenders for refinancing, especially local mortgage lender near me options or a mortgage broker in [city] who understands Utah’s market.

Understanding Home Equity Loan vs HELOC

Many Utah homeowners tap into their home’s value to cover renovations or major expenses. The most common options are a home equity loan vs heloc. A home equity loan with good credit is ideal for those who want fixed monthly payments. If you’re less creditworthy, a home equity loan with bad credit may still be possible, but rates will be higher.

Need more flexibility? A home equity loan vs line of credit comparison will help you understand whether you want a lump sum (loan) or revolving credit (HELOC).

Investment Properties and DSCR Loans

Looking beyond your primary residence? You’ll want to consider a mortgage for second home or a loan for real estate investment. If you’re investing in rental property, a dscr loan for investors may be the best option—it’s based on rental income, not your personal debt-to-income ratio.

Application Tips and Staying Informed

Apply anytime with a mortgage application online and speed up the process. Use a mortgage pre approval tool to strengthen your offer and avoid surprises during underwriting. Staying informed through mortgage news and regularly checking the best mortgage rates in [city] can save you thousands over the life of your loan.

Need help choosing the right partner? Ask local home loan providers for quotes or schedule time with a mortgage broker in [city].

Conclusion

Whether you’re applying for a mortgage for first time buyers, considering a home equity loan vs heloc, or looking for home loan assistance [state], you don’t have to do it alone. Use every tool at your disposal—from a mortgage estimator free to a mortgage application online—and compare options wisely.

Don’t forget: your financial future begins with knowledge. Bookmark this page, check back for mortgage news, and reach out to local home loan providers to get started today.