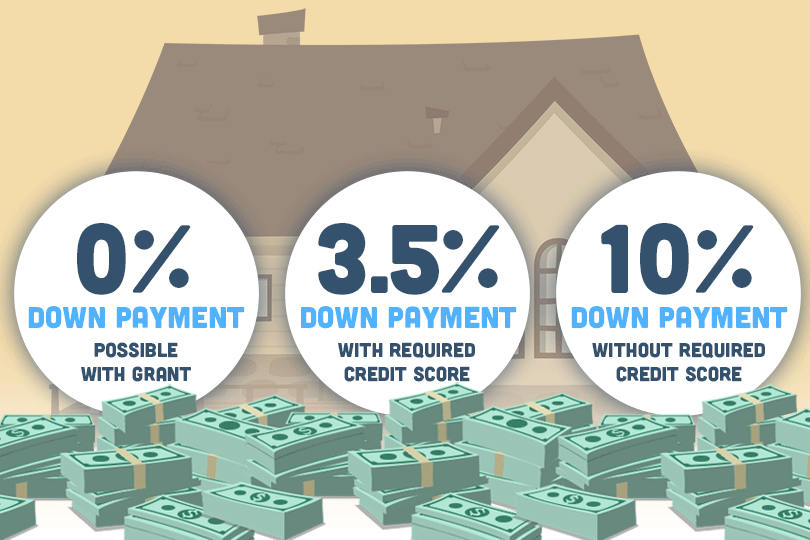

A VA home loan is a mortgage option available to veterans, active-duty military members, and their families, guaranteed by the U.S. Department of Veterans Affairs (VA). In Utah, VA loans provide several key benefits, including no down payment, no private mortgage insurance (PMI), competitive interest rates, and flexible credit requirements. They also limit closing costs and allow veterans to reuse their benefits. To qualify, applicants must meet specific service criteria, such as active duty during wartime, peacetime, or service in the National Guard or Reserves. In Utah’s competitive housing market, particularly in high-cost areas like Salt Lake City, VA loans can help veterans secure homes with more favorable terms. With the state’s growing real estate market, these loans are especially helpful for veterans looking to buy homes in both urban and rural parts of Utah, making them crucial financial tools for those who have served.

Varieties of VA Home Loan Options

When it comes to VA home loans, there are several flexible and unique options available to veterans, active-duty service members, and their families. Each loan type is designed to cater to specific financial needs and goals, making homeownership more accessible and affordable. Whether you’re purchasing a new home, refinancing an existing mortgage, or looking to tap into your home’s equity, VA loans offer competitive rates and favorable terms. Below, we break down the different types of VA home loan options.

VA Purchase Loan

This loan type allows qualified buyers to purchase a home without needing a down payment, and it often comes with lower Utah mortgage rates than conventional loans.

VA Cash-Out Refinance

This option lets you replace your current mortgage with a new VA loan, helping you access cash by tapping into your home’s equity, with the potential to benefit from Utah VA refinancing rates.

VA Interest Rate Reduction Refinance Loan (IRRRL)

Also known as a streamlined refinance, this loan is designed to help reduce your monthly payments by securing a lower VA loan interest rate Utah on an existing VA loan.

VA Home Loan Lenders in Utah

Finding the right VA home loan lender in Utah is essential for veterans, active-duty service members, and their families looking to take advantage of their VA benefits. Utah has a variety of experienced lenders who specialize in VA loans, offering competitive rates and terms tailored to the unique needs of military borrowers. These lenders understand the specific requirements of VA loans, including no down payment options, lower interest rates, and no private mortgage insurance, making home ownership more affordable. For a full list of reputable lenders offering VA and other mortgage options,

Choosing a trusted VA lender ensures you get the support and expertise needed throughout the home-buying process. Ensuring you’re partnering with the right bank is crucial before making an important decision such as a mortgage.

Visit our guide on the best banks for mortgages in Utah. https://www.mortgagerateutah.com/category/mortgage-loans/best-mortgage-banks-in-utah/

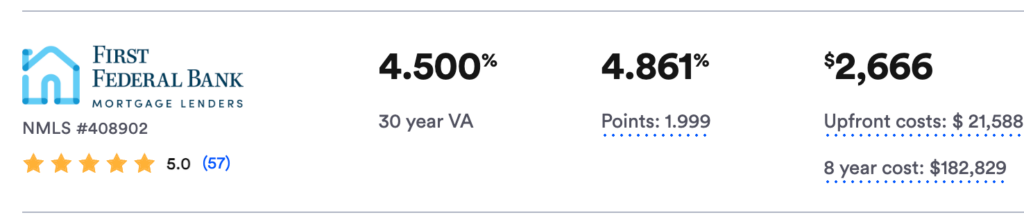

Utah Military Mortgage Rates

As in other states, Utah military mortgage rates are frequently linked to VA loans, which provide a number of advantages to qualifying spouses, veterans, and active-duty military personnel. Military families find VA loans to be an appealing alternative since they often have lower interest rates than regular mortgages, no down payment requirements, and no private mortgage insurance (PMI). Both home purchases and mortgage refinancing are possible with these specific loans in Utah. VA loan Utah requirements are typically straightforward and designed to meet the financial needs of service people, but VA loan interest rates Utah can vary depending on the lender, the borrower’s credit history, and the state of the market.

Summary:

Guaranteed by the U.S. Department of Veterans Affairs, a VA home loan Utah is a great option for veterans, active-duty members, and their families. In Utah specifically, these loans are especially useful because of the benefits they offer, including lower interest rates, no private mortgage insurance (PMI), and no down payment. Adding to that, they are also extremely flexible and can be tailored specifically to meet diverse financial needs and circumstances. These options not only enhance affordability but also empower veterans to make smart financial decisions while homebuying. Considering Utah’s highly competitive real estate market, these types of loans are especially great for those who are seeking a home.

On the website Mortgagerateutah.com, they provide lists of the best mortgage banks and brokers in Utah. The page is designed to be intuitive and easy to navigate, which can help veterans access VA home loans with ease. The website also offers specific tabs dedicated to VA loans, showing insights into lenders who specialize in the field, along with additional resources to help the navigation/decision process for military families. The variety of options reflects a commitment to helping veterans achieve their dream home-buying experience.

For more details on the benefits and general information on VA loans

Here we highlight the benefits of VA loans, whether you qualify for one, and how to apply.

Other Places to Help:

This subreddit is a community for veterans to navigate their finances after serving our country. The members discuss a wide variety of topics, with VA home loans being a large piece of it, so this subreddit makes sense to attract readers to connect and ask questions with others in similar situations.