If you’re buying your first home, refinancing a current mortgage, or exploring a home

equity option, understanding mortgage rates in Utah is more important than ever in

2025. Utah’s real estate market has been one of the fastest-growing in the U.S. for

years, fueled by a young population, strong job growth, and an influx of remote workers.

But with rising interest rates and tightening lending conditions, getting the best deal on

your mortgage—or even understanding what your options are—can be challenging.

-

How to Get Pre-Approved for Mobile Home Loan

With home prices soaring, mobile homes offer an affordable alternative to apartment living. Learn how to get pre-approved for a mobile home loan in Utah today!

-

FHA Loan for Bad Credit in 2026: Mortgage Rate Forecast and Full Monthly Payment Breakdown

If you are searching for an FHA loan for bad credit in 2026, you are likely also checking mortgage rates today, reviewing the mortgage rate forecast, and calculating what your real monthly payment might look like. The good news is that an FHA loan continues to be one of the most accessible mortgage options for…

-

Utah Mortgage Rates Today: What Homebuyers and Homeowners Need to Know in 2025

Mortgage rates play a major role in determining how affordable a home is, how much buyers can borrow, and whether refinancing makes financial sense. In Utah, where population growth and housing demand remain strong, understanding current mortgage rates—and where they may be headed—is especially important for both first-time buyers and existing homeowners. This guide breaks…

This guide breaks down everything you need to know, from how to check the latest

mortgage rates this week, to using a mortgage calculator Utah lenders trust, to

finding the best home equity loan rates Utah residents can access.

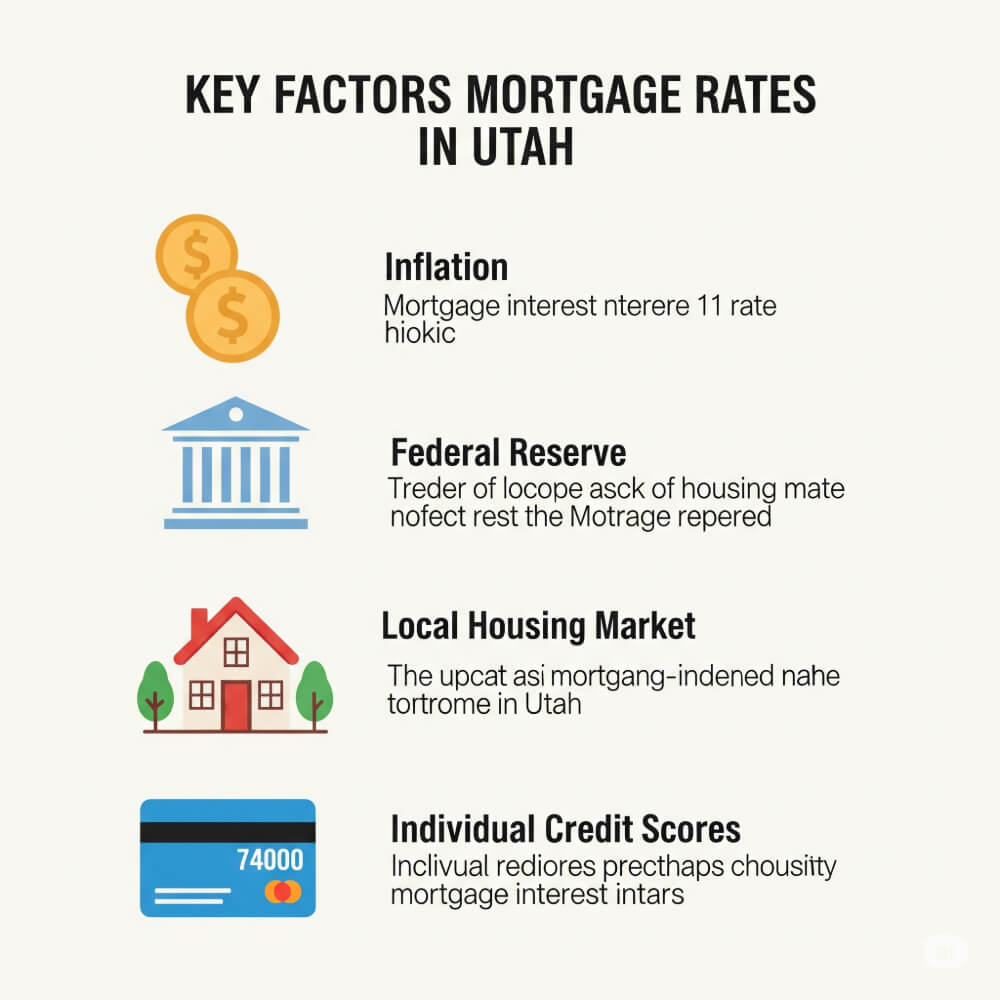

What Are the Current Mortgage Rates in Utah?

As of early 2025, mortgage rates in Utah for a 30-year fixed loan hover between 6.5%

and 7.2%, depending on your credit score, down payment, and lender. These rates may

seem high compared to the ultra-low rates of 2020–2021, but they’re fairly consistent

with national averages today. Meanwhile, 15-year fixed rates are slightly lower, ranging

from 5.8% to 6.4%.

It’s important to note that these rates change weekly. That’s why checking mortgage

rates this week is a crucial step before applying for a loan. Rates can rise or fall with

inflation reports, Federal Reserve meetings, or changes in lender policies.

Exploring VA Mortgage Rates in Utah

f you’re an active-duty service member, veteran, or surviving spouse, you may qualify

for a VA loan and that comes with serious advantages. VA mortgage rates in

Utah are typically lower than conventional loans, and they often don’t require a

down payment or private mortgage insurance (PMI). Many Utah-based lenders offer VA

loans, and competition helps keep rates favorable.

For example, institutions like Mountain America Credit Union and America First Credit

Union routinely advertise competitive VA mortgage rates with added benefits like low

closing costs and flexible underwriting for military families.

Using Mortgage Calculators for Utah Buyers

Before you even talk to a lender, it’s smart to estimate your budget using a reliable

mortgage calculator Utah residents can count on. These tools let you plug in your

expected interest rate, loan term, down payment, and estimated taxes and insurance to

get a preview of your monthly payments.

Some mortgage calculators go a step further by estimating your front-end and back-end

debt-to-income ratios, helping you understand what banks will actually approve. Look

for calculators on lender websites or platforms like Bankrate and NerdWallet.

Home Equity Options: Agreement vs. Loan

Utah homeowners sitting on built-up equity have two primary ways to access it: a home

equity loan or a home equity agreement. Both have pros and cons.

- A home equity loan is a traditional second mortgage with a fixed rate. Current

home equity loan rates in Utah are usually between 7.0% and 8.5%,

depending on the lender. - A home equity agreement, on the other hand, is a newer model. Instead of a

loan, you receive cash in exchange for a percentage of your home’s future value,

usually repayable in 10–30 years. Companies like Unison and Point offer this

option in Utah.

Using a home equity calculator can help you understand which option may be more

cost-effective based on your plans to sell or refinance in the future.

Should You Refinance Your Mortgage in 2025?

If you locked in a high rate in 2023 or 2024, you may be looking to refinance now that

the market is starting to stabilize. Refinance rates in Utah have slightly improved,

especially for borrowers with strong credit and home equity.

Still, it’s important to compare refinance mortgage rates and factor in closing costs.

Many Utah homeowners overlook hidden fees that can eat away at their savings. Tools

like a refinance calculator can help you determine your break-even point and whether

refinancing makes financial sense.

Don’t Forget About Other Rate Terms

In addition to conventional loans, many lenders offer specialized rate structures:

- House rates Utah – This term is often used to describe rates across different

housing products, including manufactured or modular homes. - Mortgage rates this week – Always compare this week’s published rates to

previous trends. - VA mortgage rates Utah – Ensure your lender is VA-approved if you qualify.

- Refinance rates Utah – Rates may be lower than purchase loans depending on

equity and credit

By understanding how these terms differ, you’ll be better equipped to ask the right

questions when meeting with a mortgage advisor.

What Is a Mortgage, Really?

It sounds basic, but many first-time buyers still ask: what is a mortgage? A mortgage is

simply a legal agreement where a lender gives you money to buy a home, and you

agree to pay it back—plus interest—over time. The lender uses your home as collateral.

If you fail to make payments, they can foreclose and take ownership of the property.

There are many types of mortgages: fixed-rate, adjustable-rate, government-backed

(like FHA or VA), and jumbo loans. Each comes with its own eligibility requirements,

rate structures, and long-term financial implications.

Final Thoughts: Be a Smart Borrower in Utah

In a competitive market like Utah, knowledge is your most powerful tool. Whether you’re

using a mortgage calculator, shopping for VA mortgage rates in Utah, or comparing

a home equity loan vs. a home equity agreement, being informed helps you avoid

overpaying.

Start by reviewing mortgage rates in Utah this week, then explore your options using

reputable lenders, online tools, and financial advisors. And don’t be afraid to ask

questions—mortgages may be complex, but they don’t have to be confusing.

Next Steps:

- Check weekly rates from trusted sources like Bankrate

- Use a calculator from NerdWallet

- Compare loan offers from local and national lenders