The median home sales price in May 2024 has increased in the past 3 months to $545,900. That’s up 3.1% and $16,300 higher than May 2023 of last year. That is higher than the national median home sales price of $439,716.

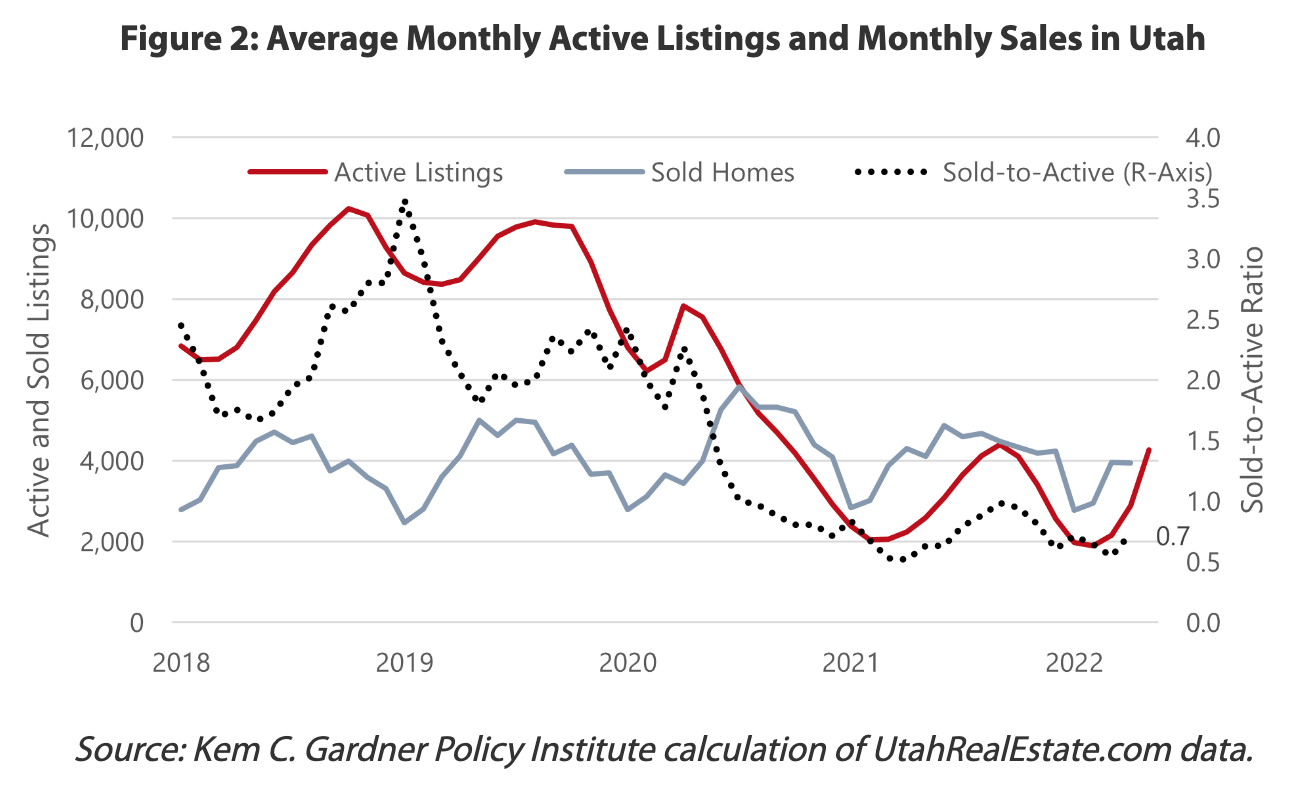

How many houses are available in Utah?

The real estate market in Utah had 9,935 homes for sale in May 2024 and is up from 9004 homes for sale the month prior and up from 8,286 homes in May 2023 which is 19.9% up.

How many houses are sold in Utah?

There were 3468 homes sold in May 2024, trending up from 3116 homes sold a year ago. This is up 352 homes and 11.3% since May 2023.

How long does it takes to sell a house in Utah?

Homes in Utah are staying on the market for 35 days. That’s 4 days slower than the median in May 2023, which is 12.9%. This shows that the market is less competitive today.

Utah Housing Market in 2025

Impact of Mortgage Rates

Our forecast for existing home sales through 2025 has been modestly revised downward due to expectations of higher mortgage rates. Rates are expected to remain close to 7% through the end of the year before potentially trending downward in 2025.

Yearly Comparisons

In 2023, the growth rate was 6.6%, and for 2024, we forecast a 4.8% increase. By 2025, the growth rate will dip to 1.5%, well below the long-run average of 3-5% annual increases.

Comparing January and May Forecasts

In January, a lot of real estate professionals predicted a 3.2% increase in home prices for 2024. By May, this forecast was revised to 4.8%. For 2025, the January forecast was a 3% increase, which was later adjusted to 1.5% in May.

Historical Context

The average number of existing home sales per year since 1989 is just over 5 million. The 2025 forecast of 4.5 million is about 500,000 less than this historical norm.

Purchasing a home is an accomplishment that everyone hopes to look forward to in their life. Ensuring that you secure the right mortgage for you is crucial to be comfortable financially while enjoying your new home. Trying to sort and calculate through the numerous mortgage banks in Utah can be a confusing and intimidating experience. However, if you approach it by analyzing your options and informing yourself the best you can, you will hopefully be able to make a decision that benefits you and your home.

Assess Your Financial Situation

When deciding which mortgage bank you should choose, you should first assess your own financial situation. Take time to understand your credit score and how that will affect the interest rate and terms you will be offered by different Utahbanks. Double check your credit score history for any mistakes that could have been made. After doing so, work to calculate your debt-to-income ratio. This will give you a good idea of how much you can afford to borrow. For reference, many banks prefer a debt-income ratio of 43% or lower.

Research Mortgage Types: what makes the most sense for you?

Once you analyze your financial situation, it is important to educate yourself on the different mortgage types available and which one will work best for you. Most of these mortgages will have both advantages and disadvantages which is why it is needed to weigh all your options before coming to a decision. Here is a brief overview of the most common types of mortgages that you may encounter.

Fixed-Rate Mortgages: You can expect these loans to have a consistent interest rate throughout the term. This is often preferred as it provides stability in monthly payments.

Adjustable-Rate Mortgages (ARMs): These loans normally start with a lower fixed rate for the first couple of years. Afterwards, you will see the rate adjusted based on the market’s conditions.

FHA Loans: This type of loan is provided by The Federal Housing Administration. These loans are usually preferred for first-time homebuyers that have a lower credit score.

VA Loans: These loans are available to veterans and active military members. They offer loans at a competitive rate and require no down payment.

Jumbo Loans: This is the loan that you would want for a property that exceeds the conforming loan limit. Jumbo loans are a great option for people who need them, but along with the larger lump sum of money comes higher interest rates and stricter requirements.

Compare Mortgage Rates and Terms

Having a reasonable interest rate is a vital detail to ensure that you will be comfortable with the overall cost of your mortgage. To find the best rate it is important that you compare the offers and terms from multiple institutions. Reach out to banks for a personalized mortgage quote and compare the Annual Percentage Rate (includes the interest rate and additional fees) as that will give you the best overall view of the loan. After analyzing the interest rates, reading and evaluating the loans terms and conditions is just as important. Consider factors such as:

Loan Fees: This can include origination fees, closing costs, and other charges that can unexpectedly add up. Ensure you understand all costs associated with the bank.

Prepayment Penalties: Some banks will have loans penalties for paying off your mortgage early. This is something you want to make yourself aware of, especially if you plan to sell or refinance before the end of the loan. Try to avoid these penalties if possible.

Flexibility: When a bank offers flexibility in payment scheduling and rate locks it could be end of being very helpful in the future. It is worth checking out each bank’s options.

Do your research on who you are trusting your money with

After combing through the rates and terms of each bank, it is important to ensure that the institution you are going through will be reliable and safe with your money. Reading through other people’s reviews from their personal experiences is a great way to understand more about the mortgage bank’s reputation and how your experience with them will likely go. Look into banks with a strong reputation for customer satisfaction as you will more likely have a smooth experience with their institution.

Utilize Utah’s financial resources

Once you have completed your research into your own financial capability and into the banks that you are considering it is always a good idea to get a professional opinion as well. Utah has many different resources that can help guide homebuyers. For first-time homebuyers, The Utah Housing Corporation offers programs that assist with down payments and finding competitive mortgage rates. Local credit unions and banks also offer services tailored to serve Utah homebuyers.

How to Find Your Ideal Utah Mortgage Bank

For more information on The Utah Housing Corporation click here

For more information on banks and credit unions in Utah click here

To see our recommendations for Utah mortgage banks click here

Finding the right mortgage lender is crucial if you’re looking to buy a home in Utah. With a booming real estate market and various options available, knowing where to start can be challenging. To help you navigate this important decision, here are our top five mortgage banks and brokers in Utah known for their excellent service, competitive mortgage rates, and local expertise.

1. SecurityNational Mortgage Company

SecurityNational Mortgage Company, headquartered in Salt Lake City, Utah, stands out for its comprehensive and innovative mortgage solutions. Founded in 1993, SecurityNational offers a wide range of loans designed to meet the diverse needs of Utah homeowners. Their product offerings include conventional, FHA, VA, USDA, and jumbo loans. Additionally, they provide specialized programs for first-time homebuyers, offering lower down payments and flexible credit requirements to make homeownership more accessible.

Note: Some customers have reported that the processing time can be longer than expected, which could be an issue if you need a quick closing.

Intercap Lending, based in Orem, Utah, is another leading mortgage company in Utah. Known for their streamlined processes and quick turnaround times, Intercap Lending makes the mortgage process straightforward and stress-free. They offer competitive mortgage rates and a variety of loan products, including fixed-rate and adjustable-rate mortgages, FHA and VA loans, and refinancing options. Intercap Lending’s commitment to customer satisfaction and their deep knowledge of the Utah housing market make them a top choice for many homebuyers.

Note: While they offer quick turnaround times, some clients have mentioned that communication can be inconsistent, leading to potential misunderstandings during the process.

Altius Mortgage Group, located in South Jordan, Utah, is a highly regarded mortgage broker that offers a personalized approach to home financing. As a broker, Altius works with multiple banks to find the best loan options for their clients. This flexibility allows them to offer highly competitive mortgage interest rates and a wide range of loan products.

Note: As a broker, their rates and terms are subject to the lenders they partner with, which can sometimes result in less control over the final loan conditions.

Guild Mortgage, with several branches throughout Utah, has been providing home financing solutions since 1960. Known for their strong commitment to customer service, Guild Mortgage offers a variety of loan products tailored to meet the needs of Utah homeowners. They provide conventional loans, FHA and VA loans, jumbo loans, and refinancing options. Guild Mortgage’s knowledgeable loan officers are well-versed in the local market conditions and work closely with clients to find the best mortgage solutions to fit their needs.

Note: Some borrowers have experienced higher closing costs compared to other lenders, which could affect your overall budget.

Citywide Home Loans, headquartered in Sandy, Utah, is a full-service mortgage lender with a strong presence in the state. They, like their competitors, offer a comprehensive range of loan products, including conventional loans, FHA and VA loans, USDA loans, and jumbo loans. Citywide Home Loans is highly regarded by many Utah homeowners for their exceptional customer service and competitive mortgage rates.

Note: Despite their excellent service, some customers have noted that their application process can be more documentation-heavy and rigorous than other lenders.

When selecting a mortgage lender, it’s important to consider factors such as mortgage interest rates, loan options, customer service, and the lender’s knowledge of the local market. These five mortgage companies in Utah have established themselves as leaders in the industry, offering excellent service and competitive mortgage rates to help you achieve your homeownership dreams. Be sure to contact multiple lenders, compare their offerings, and choose the one that best meets your needs and financial situation.

By selecting a reputable mortgage lender, you can navigate the home-buying process with confidence, knowing you have a trusted partner to help you every step of the way. Whether you’re buying your first home, refinancing, or investing in property, these top Utah mortgagebanks and brokers are ready to assist you in securing the best possible mortgage for your needs.

Looking to purchase your first home and need advice? Click here.

Need a mortgage rate calculator? Visit our Mortgage Rate Calculator blog here.

Great! You’ve decided to set roots in Utah, the land of stunning landscapes and vibrant communities. But before you picture yourself sipping tea on a cozy porch overlooking the Wasatch Range, there’s the hurdle of navigating the home-buying journey. This guide will provide a one-stop shop for buying a home in Utah real estate market.

Utah is known for its stunning landscapes, strong economy, and family-friendly communities. Here’s why buying a home in Utah could be one of the best decisions you make:

Booming Economy: Utah boasts a robust job market, particularly in tech and healthcare, which makes it a prime location for career growth and stability.

Outdoor Lifestyle: From skiing in Park City to hiking in Zion National Park, outdoor enthusiasts will find plenty to love. Utah’s natural beauty offers numerous recreational opportunities year-round.

Family-Friendly: With excellent schools and safe neighborhoods, Utah is a great place to raise a family. Communities are designed to be welcoming and supportive, making it an ideal place for young families.

Understanding the Utah Real Estate Market

The Utah real estate market is unique and has its own set of trends and characteristics:

Growth Areas: Salt Lake City, Provo, and St. George are some of the fastest-growing areas, attracting new residents due to their vibrant economies and desirable living conditions.

Price Trends: While prices have been rising, there are still affordable options, particularly in emerging neighborhoods across the valley. This offers opportunities for both first-time homebuyers and those looking to invest in real estate.

Overlooking shot of St. George, Utah. (Courtesy of Livability)

Utah Home Buying Statistics

Understanding the current market statistics can help you make informed decisions:

Statistics about Utah Home Buying

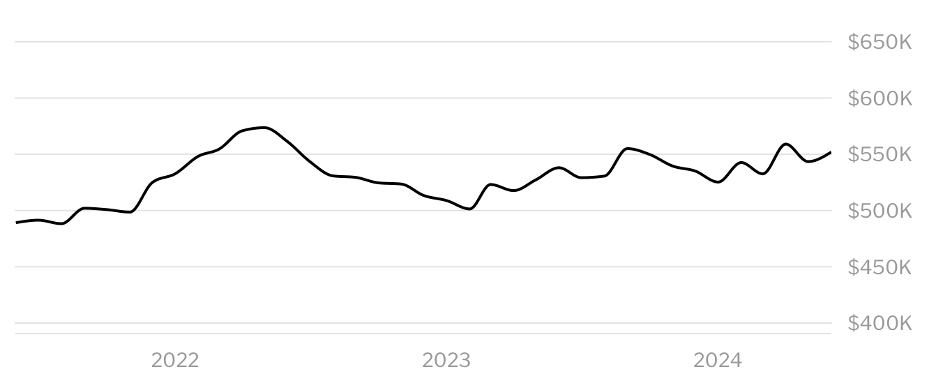

Average sale price of homes in Utah (June 2024) [i]

The Economy: Utah boasts a healthy economy, but buying a home requires sound financial planning. In June 2024, 26.6% of homes in Utah sold above list price[iv], which is something to consider when putting in an offer for a home. On the other hand, property tax rates in Utah are low. Utah has the sixth lowest property tax rate in the country at 0.55%.[v]

Getting a Mortgage: Whether you have 3% to put down on a home or 20%, finding the right lender is critical. We’ll explore top Utah lenders offering competitive rates and programs tailored to first-time homebuyers or specific needs.

Finding a Real Estate Agent: A solid real estate agent who will advocate for you in your Utah home buying journey is critical. We’ll discuss the benefits of working with an agent, along with tips for finding the perfect match who understands your needs and the local market.

Once you understand some of the important financial information, you can look at some important considerations for first-time homebuyers to make sure you’re well-prepared.

Tips for First-Time Homebuyers in Utah

Consider State Programs: Utah offers various first-time homebuyer programs and grants. Visit the Utah Housing Corporation for more information.

Budget for Closing Costs: In addition to your down payment, budget for closing costs, which can include fees for inspections, appraisals, and title insurance.

Research Neighborhoods: Take the time to research and visit different neighborhoods to find the one that best suits your lifestyle and needs.

Make sure to look into down payment assistance and loan programs that you may qualify for!

Utah Down Payment Assistance and Loan Programs

Programs

FirstHome

FHA or VA Mortgage

Conventional HFA Advantage Loan

Qualifications

– First time homebuyer – 660 or higher credit score

– Previously owned a home or first-time homebuyer – 620 or higher credit score

This program typically has lower purchase price and income limits and lower interest rates.

Homebuyers can purchase residence with up to 2 units

Financing option for this loan might have a higher interest rate but a lower mortgage insurance costs, which might result in a lower monthly payment.

Source: Down Payment Assistance and Loan Programs. (2023). In Utah Housing Corporation. Utah Housing Corporation. Retrieved July 18, 2024, from https://utahhousingcorp.org/pdf/Form211.pdf

Now that you have all of the information, you are ready for the next steps.

Next Steps to Buying Your Utah Home!

Take the next steps to buying your home!

Get Pre-Approved for a Mortgage

What are today’s mortgage rates in Utah? Check them out here.

Remember: interest rates will vary by lender and by borrower, depending on factors like credit score, loan program, down payment, etc. Compare quotes from at least 3 different lenders to make sure you’re getting the lowest rate.

Ask about down payment and closing cost assistance.

Partner with a knowledgeable real estate agent who knows the Utah market. Consider agents from reputable firms like Coldwell Banker and Re/Max.

Make sure they’re licensed, read reviews, ask questions about how they will help you, and trust your instincts to find the right person to help you buy your home.

[iii] GOBankingRates. (n.d.). The average credit score in each state — see where your state ranks. Nasdaq. https://www.nasdaq.com/articles/the-average-credit-score-in-each-state-see-where-your-state-ranks#

[v] Pitts, E. (2024, February 22). Some states have more affordable property taxes than others. Where does Utah rank? Deseret News. https://www.deseret.com/utah/2024/2/20/24078329/state-ranking-property-tax-value-utah-housing-market/