Posting and Optimizing Content – Mortgage Rate Utah

The Complete Mortgage Guide: What Every Home Buyer Should Know Before Getting a Home Loan Buying a home is one of the biggest financial decisions …

The Complete Mortgage Guide: What Every Home Buyer Should Know Before Getting a Home Loan Buying a home is one of the biggest financial decisions …

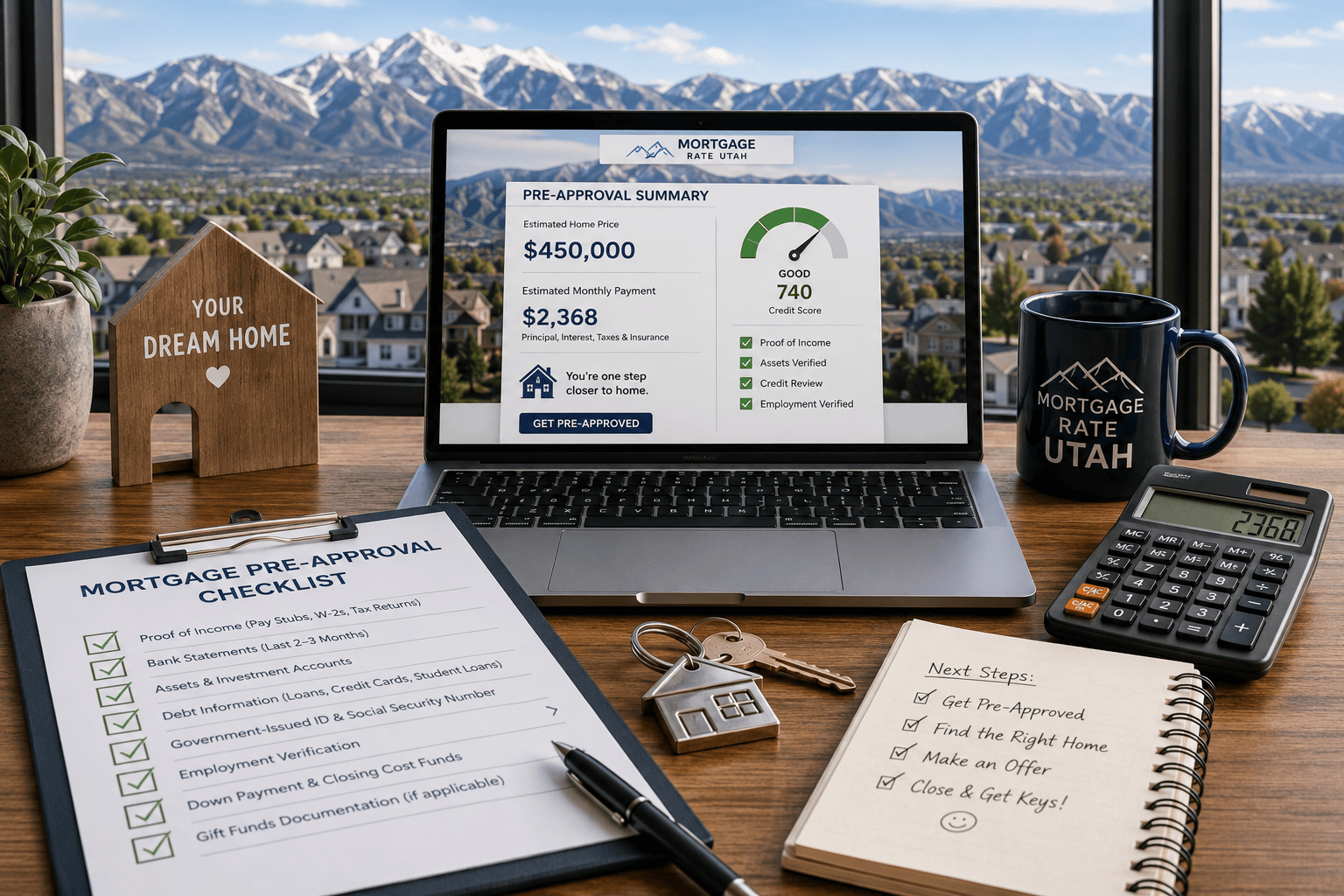

Mortgage Pre Approval Checklist: Everything You Need Before Applying Getting ready to buy a home is exciting, but it can also feel overwhelming if you …

If you have a VA home loan and interest rates have dropped since you closed, you have probably run into the term and wondered, what …

Want to understand current mortgage rates in Utah today? This guide helps you compare, calculate, and lock in the best deal using real numbers and …

VA home loans are mortgage options that private lenders provide for veterans, active-duty service members, and surviving spouses who qualify. The VA home loan program …

Do you wish to own a home one day? You, like many, also want to have a place they can call their own. But it’s …

What is a VA Loan? A VA Loan, or a Veteran Affairs loan, is a specialized mortgage program designed to provide financial assistance to eligible …