Utah Mortgage Pre Approval

If you’re shopping for a home in Utah, the best way to reduce stress (and write a stronger offer) is to get your financing ready before you fall in love with a listing. A real pre-approval helps you understand your budget, speeds up the offer process, and shows sellers you’re serious. This guide walks you through the process, the documents you’ll need, and how options like FHA, VA, and online applications fit in—so you can move quickly and confidently.

Mortgage Pre Approval Utah: What It Is and Why It Matters

Mortgage pre approval Utah means a lender has reviewed your financial information—typically income, assets, debts, and credit—and is willing to pre-approve you up to a certain loan amount (assuming nothing major changes before closing). This is different from a rough estimate because it’s based on documentation, not just a conversation. In many Utah markets, sellers and agents expect buyers to have a pre-approval letter ready, and it can make your offer feel safer and more credible.

If your main goal is to get pre approved Utah, start early. Even if you’re “just looking,” pre-approval gives you a realistic price range and helps you avoid wasting time on homes that don’t match your true buying power. It also gives you a chance to fix issues (like paperwork gaps or a debt-to-income problem) before you’re under pressure.

Home Loan Pre Approval vs. Pre-Qualification: Which One Do You Need?

Some buyers begin by trying to <strong>prequalify for home loan</strong> because it’s fast and low-commitment. Pre-qualification is usually an informal estimate based on what you report (income, debts, and general credit range). It can be helpful early on, and it’s why so many people search how to get prequalified for a home loan when they’re still exploring options.

But if you want to write offers, a home loan pre-approval is the stronger step because it involves verification. When you get pre-approved for a mortgage, the lender checks documents and runs credit, so the letter actually means something to sellers. If you’re serious about buying soon, you’ll typically want to move beyond pre-qualification and get pre-approved for a home loan before you start making big decisions.

Some buyers begin by trying to prequalify for home loan because it’s fast and low-commitment. Pre-qualification is usually an informal estimate based on what you report (income, debts, and general credit range). It can be helpful early on, and it’s why so many people search how to get prequalified for a home loan when they’re still exploring options.

But if you want to write offers, a home loan pre-approval is the stronger step because it involves verification. When you get pre-approved for a mortgage, the lender checks documents and runs credit, so the letter actually means something to sellers. If you’re serious about buying soon, you’ll typically want to move beyond pre-qualification and get pre-approved for a home loan before you start making big decisions.

How to Get Pre-Approved for a Home Loan in 5 Practical Steps

If you’ve been wondering how to get pre-approved for a home loan, this is the most straightforward path that works for most borrowers:

- Pick a lender and complete the application

- Upload your financial documents (income, assets, debts)

- Authorize a credit check

- Review loan options and confirm your comfortable payment range

- Receive your letter and keep your finances stable while you shop

That process is also what people mean when they ask how to get preapproval for a home loan—the goal is a written letter you can use when making offers. You’ll often see similar phrases like mortgage loan pre approval and house loan pre approval; they’re different wording for the same milestone: you’ve been reviewed and are ready to buy within a certain range.

If you’re asking how I can get pre-approved for a home loan as quickly as possible, the #1 tip is to respond fast when the lender requests clarification (like a missing page of a bank statement, proof of employment, or explanation for a deposit). Delays usually happen when documents are incomplete or unclear.

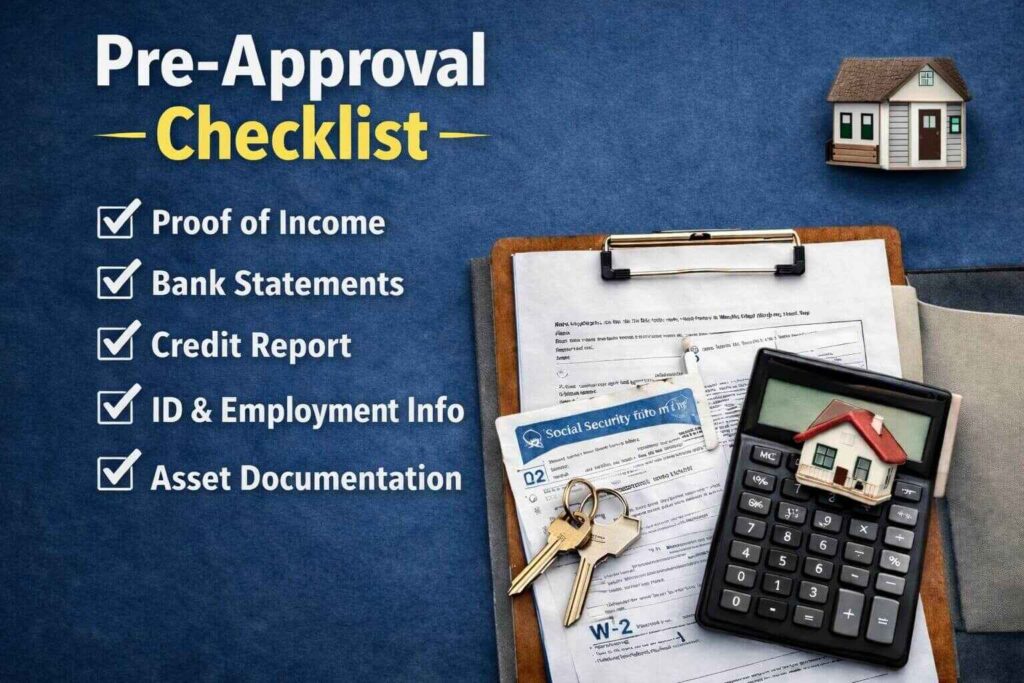

What Is Needed to Get Pre Approved for a Mortgage: Your Document Checklist

People commonly ask what is needed to get pre-approved for a mortgage because they don’t want surprises. While lenders vary, you can usually prepare for these categories:

- Identity verification (ID)

- Proof of income (pay stubs, W-2s, or tax returns if self-employed)

- Proof of assets (bank statements, retirement accounts, gift funds documentation if used)

- Employment history details

- A list of monthly debts (auto loans, student loans, credit cards)

- Credit authorization (so the lender can review score and history)

This checklist is also what helps when you’re asking how to get pre-approved for a home mortgage—you’re proving you can repay the loan, and you have funds to complete the purchase.

If your question is more specific—like how to get pre-approved for a house or how to get pre-approved for a house loan—the same checklist applies. The “house” part just means you’re using the approval to shop for a property; the lender still evaluates the borrower the same way.

FHA and VA Options: FHA Loan Pre Approval and VA Home Loan Pre Approval

Your loan program can affect details (like down payment rules and documentation), but the structure of approval stays similar.

For FHA borrowers, FHA loan pre-approval is typically focused on verifying income, assets, and credit—then pairing you with FHA guidelines. You’ll also see the shorter phrase fha pre approval used interchangeably. FHA can be a fit for some buyers because it’s designed to widen access to homeownership, but it still requires careful documentation and underwriting.

For eligible military buyers, va home loan pre-approval can be a major advantage. You may also see va mortgage pre-approval used for the same concept. VA loans often require that you confirm your eligibility (commonly through a Certificate of Eligibility) and meet lender standards for credit, income, and occupancy.

Online Speed: Online Mortgage Pre Approval and How It Works

If convenience matters, <strong>online mortgage pre approval</strong> can reduce friction because you can upload documents through a secure portal, sign disclosures digitally, and track your progress without playing phone tag. Online doesn’t mean “less real”—your lender still verifies your financial profile. The benefit is speed and organization, especially if you’re juggling work, school, or moving timelines.

Many buyers start with an estimate and prequalify for a mortgage loan online first, then transition into full approval once they’re ready. If your goal is to move from “planning” to “offer-ready,” ask the lender what they need to convert a pre-qual into a full approval letter.

FAQ: The Most Common “How-To” Questions (Answered Clearly)

Q: How to get pre-approved for a mortgage loan?

A: Apply, submit documents, authorize credit, and respond quickly to lender follow-ups. This is the cleanest path to a usable pre-approval letter.</p>

Q: Get pre-approved for a home mortgage (what should I do right now?)

A: Gather your pay stubs/tax returns, bank statements, and debt info first—then apply. Being organized speeds everything up.</p>

Q: How to get preapproval for a mortgage if my credit needs work?

A: A lender can often tell you what’s holding you back (high balances, recent late payments, or too much debt) and what to change before you reapply.

Q: Get pre approved for a mortgage and keep it valid

A: Avoid opening new credit lines, making large unexplained deposits, or changing jobs during the process. Those things can trigger re-verification.