Why 2025 Might Be the Right Time to Buy a Home in Utah

Economic Outlook & Housing Market Trends

Wondering when to buy a home in Utah? The Utah housing market has undergone significant transformation in the past decade. As we enter 2025, the state continues to enjoy strong job growth, a diversified economy, and a stable real estate environment. Employment rates are high across tech, health, and education sectors, especially in areas like Salt Lake City and Provo. This economic strength contributes to a buyer-friendly atmosphere as more individuals qualify for home loans and local governments introduce initiatives aimed at making housing more accessible.

Rising vs. Falling Interest Rates in Utah

Interest rates are a critical factor for home buyers. After reaching historic highs in 2023, mortgage rates began to cool in mid-2024. Analysts predict continued stabilization in 2025, making now an opportune time for buyers to lock in relatively low rates before any future increases. A lower rate can mean thousands in savings over the life of a loan. Additionally, fixed-rate mortgages are gaining popularity for their predictability and long-term savings potential.

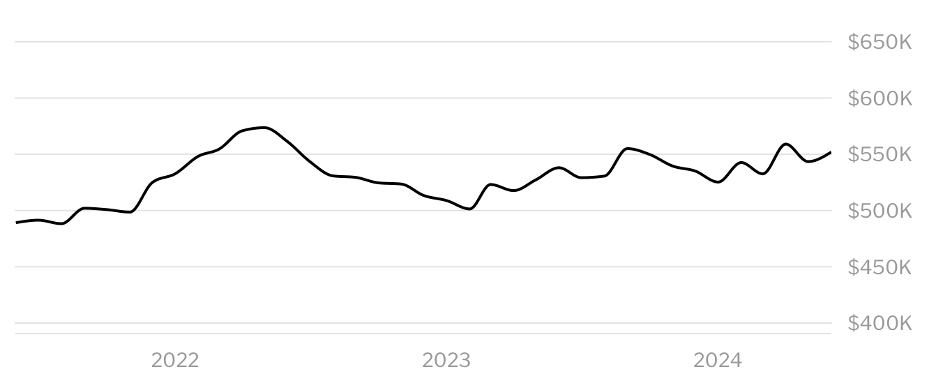

Utah’s Housing Inventory and Affordability

The rise in new construction and reduced demand from investors have opened up more inventory for first-time buyers. Suburban developments near Ogden, Layton, and Spanish Fork are offering homes in more affordable price ranges. Though prices remain higher than pre-pandemic levels, the growth has slowed. Combined with local incentives and improved loan access, homes in 2025 are more within reach for many buyers than just a year or two ago.

Financial Preparation and Credit Score Tips

Before you even browse listings, it’s crucial to assess your financial health. Your credit score is one of the most important indicators lenders will evaluate. A score of 620 or higher can open doors to better interest rates, though programs like FHA loans may accept scores as low as 580. Pay down credit card balances, avoid new debt,

and review your credit report for errors before applying.

Creating a Realistic Home Buying Budget

Setting a realistic budget means looking beyond the sale price of a home. Use a mortgage calculator to factor in property taxes, homeowner’s insurance, and private mortgage insurance (PMI), if applicable. Determine what you can comfortably afford monthly, not just what the bank approves. Budgeting conservatively ensures you won’t be

‘house poor’ and allows room for savings and unexpected costs.

Documents You’ll Need Before You Start

To get pre-approved, gather documentation including:

- W-2s or 1099s

- Tax returns from the past two years

- Recent pay stubs

- Bank statements

- ID

Organizing these ahead of time will streamline the mortgage process and reduce delays when making offers.

First-Time Home Buyer Loans in Utah: What Are Your Options?

FHA Loans and Their Requirements

The Federal Housing Administration (FHA) backs loans with lower down payment requirements and flexible credit guidelines. These loans are popular with first-time buyers who may not have saved a 20% down payment. With only 3.5% down and credit requirements starting at 580, FHA loans are among the most accessible options in

Utah.

Utah Housing Corporation Loan Programs

Utah Housing offers programs specifically tailored for first-time buyers such as the FirstHome Loan and HomeAgain Loan. These programs provide competitive fixed rates and assistance with down payments or closing costs. Some even allow you to finance up to 100% of the purchase price.

USDA, VA, and Conventional Loan Comparisons

For those in rural areas, USDA loans require no down payment. VA loans, offered to veterans and active-duty military, eliminate PMI and provide favorable terms. Conventional loans offer more flexibility for buyers with higher credit scores and larger down payments, and may carry lower overall costs if you meet the criteria.

How to Get Pre-Approved for a Home Loan in Utah

Pre-Approval vs. Pre-Qualification Explained

Pre-qualification is an informal estimate of how much you can borrow, while pre-approval involves a deeper review of your financial documents. Sellers view pre-approval as a sign of serious intent and it can significantly strengthen your negotiating position.

Steps to Secure a Pre-Approval Letter

Start by choosing a lender and submitting financial documentation. The lender will perform a credit check and verify your income and employment. Once approved, you’ll receive a pre-approval letter valid for 60–90 days, helping you shop within your means.

What Lenders Look for in Utah Applicants

Lenders will assess your credit score, income stability, debt-to-income ratio (DTI), and savings. A DTI under 43% is preferred. They’ll also check your employment history and may ask for explanations about large deposits or

financial inconsistencies.

Simple Mortgage Calculator: Plan Your Payments

Monthly Payment Estimation

A mortgage calculator is a powerful budgeting tool. Enter your loan amount, interest rate, loan term, and down payment to estimate your monthly obligation. Include estimated property taxes, insurance, and HOA fees for accuracy.

Principal, Interest, Taxes & Insurance Breakdown

Your mortgage payment isn’t just your loan. It typically includes principal, interest, taxes, and insurance (PITI). Understanding this full breakdown helps avoid budget surprises and plan long-term finances effectively.

Smart Steps to Buy Your First Home in Utah

2025 is shaping up to be a strategic time for first-time home buyers in Utah. With steadying rates, expanding loan options, and more inventory, the timing couldn’t be better. Work with trusted professionals at MortgageRateUtah.com to get pre-approved, explore tailored mortgage solutions, and turn your homeownership

dream into reality.