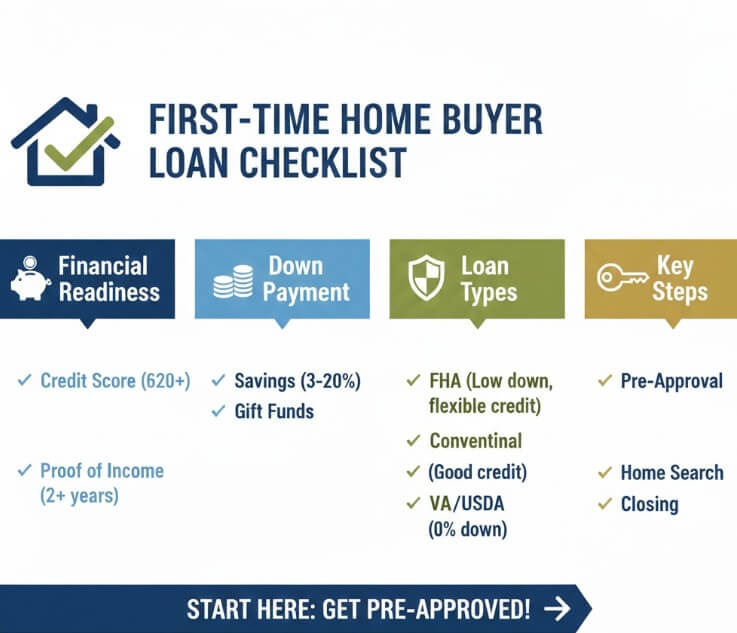

[IMAGE PLACEMENT NOTE — Hero Image]

Image Title: Mortgage Refinance Rates Today Hero

File Name: mortgage-refinance-rates-today-hero-v4.jpg

Where it goes: Directly under this H1 title at the top of the blog post

Alt text (description only): “Mortgage refinance rates today hero image showing homeowners reviewing refinance options with a home and rate visuals in the background.”

Refinancing can be a smart move when mortgage refinance rates today are lower than what you currently pay, or when you want to change your loan structure to better fit your goals. The key is making the decision with real numbers—not vibes—and that means understanding rates, costs, and how long it takes to “break even.”

If you’re trying to refinance my mortgage because your payment feels too high, you want to shorten your term, or you’re looking to pull equity out, this guide will walk you through the process in a simple way and show you how to compare lenders, calculators, and programs.

Most people start by checking current refinance rates and then running the math. That’s exactly what we’ll do here—step by step—so you can confidently decide whether to refinance my home loan now or hold off.

Current Refinance Rates: What They Mean and How to Compare Them

Current refinance rates change daily, so it helps to zoom out and compare multiple lender quotes on the same day. When people search refi rates today, they’re usually trying to answer one question: “Is today a good day to lock?”

You’ll see lenders advertise different versions of the same idea—current refinance mortgage rates, house refinance rates, and even “best” or “lowest” offers. In reality, the lowest refinance rates often assume top-tier credit, strong income, and a clean loan profile. Your rate depends on your credit score, loan-to-value, debt-to-income ratio, and whether you’re refinancing a primary home or planning a refinance investment property loan.

To compare accurately, request quotes that include both the interest rate and APR, and ask what points or lender fees are baked into the offer. That’s how you’ll know whether you’re actually seeing best refinance mortgage rates or just a marketing headline.

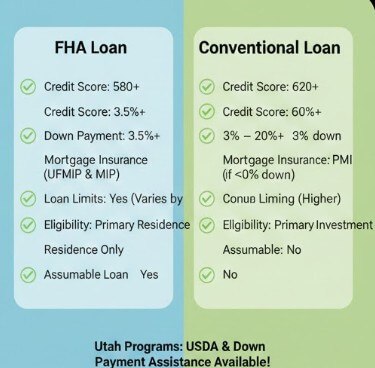

Refinance Mortgage Calculator: The Fastest Way to Know If It’s Worth It

[IMAGE PLACEMENT NOTE — Calculator Image]

Image Title: Refinance Mortgage Calculator Guide

File Name: refinance-mortgage-calculator-guide-v4.jpg

Where it goes: Directly under this H2 section title

Alt text (description only): “Refinance mortgage calculator guide showing a break-even timeline, monthly payment comparison, and estimated refinance savings.”

A refinance mortgage calculator is where clarity happens. Before you spend time gathering documents or calling lenders, run a few scenarios so you know what you’re aiming for.

A good refinance mortgage calculator (or refinance mortgage rates calculator) helps you estimate your new monthly payment, total interest over the life of the loan, and how long it takes to recover closing costs. You can also use a refi mortgage calculator if you want a quick side-by-side comparison between your current loan and a proposed refinance.

If you prefer more specific tools, you can also use a refinance home loan calculator when you’re comparing terms for a standard mortgage refinance, or a refinance house calculator if you want a simpler, homeowner-friendly layout. The best approach is to run the numbers at least three ways: conservative, realistic, and best-case.

Once you have the calculator output, you’ll be able to make a clean decision: refinance for payment relief, refinance to reduce long-term interest, or don’t refinance at all.

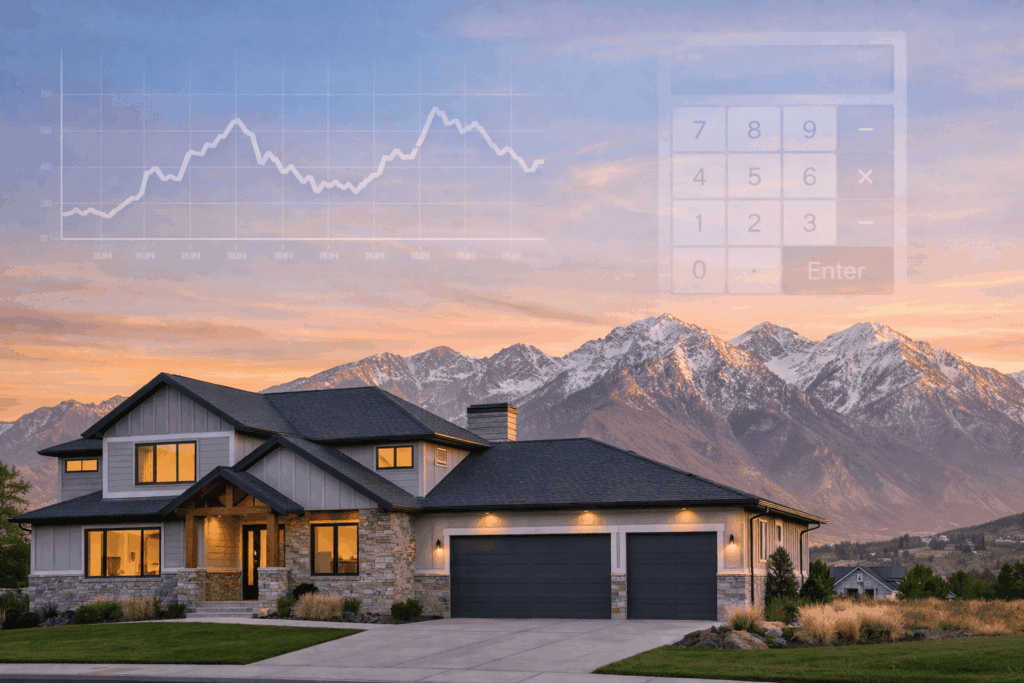

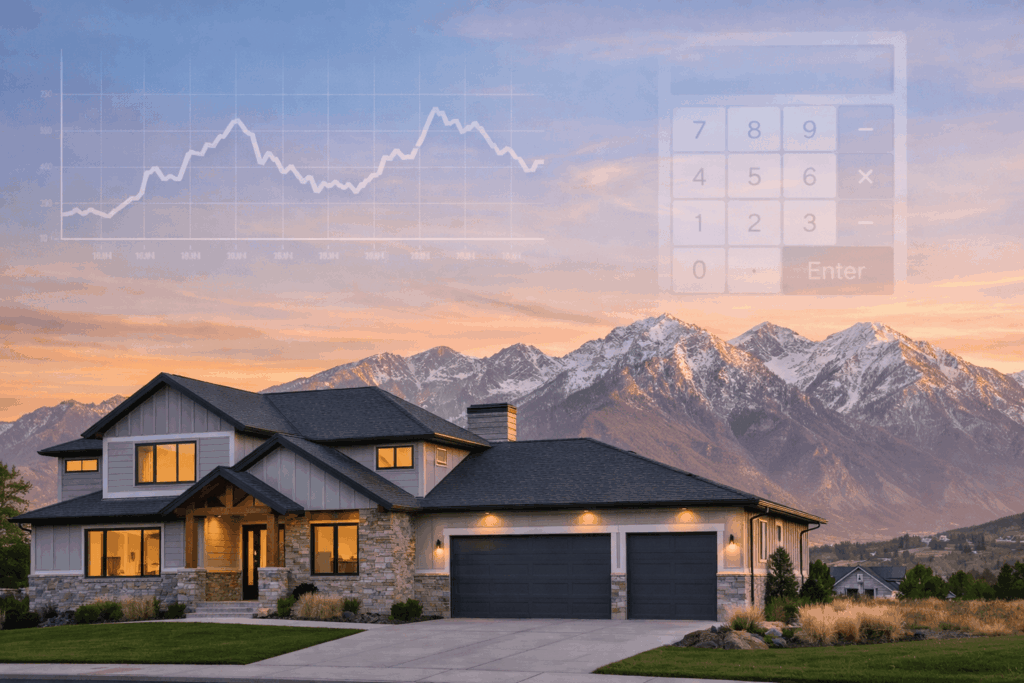

Cash Out Refinance Calculator: How to Tap Equity Without Guessing

[IMAGE PLACEMENT NOTE — Cash-Out Image]

Image Title: Cash Out Refinance Calculator

File Name: cash-out-refinance-calculator-v4.jpg

Where it goes: Directly under this H2 section title

Alt text (description only): “Cash out refinance calculator visual showing home equity access, cash-out amount, and refinance options including FHA cash out refinance and VA cash out refinance.”

If you want to convert home equity into cash, a cash out refinance calculator is your best starting point. It shows how much you might be able to access after paying off your current loan balance (and factoring in loan-to-value limits).

After you estimate your cash-out amount, compare cash out refinance rates with standard refinance rates. Cash-out loans can sometimes come with slightly higher pricing because the lender is taking on more risk.

Two common cash-out paths are fha cash out refinance and va cash out refinance. FHA options can be useful for borrowers who need more flexible credit guidelines, while VA cash-out programs may offer strong terms for eligible service members and veterans. Either way, the calculator step comes first—because it keeps your expectations realistic and your planning tight.

VA Refinance Rates and FHA Options: Picking the Right Program for Your Situation

VA refinance rates can be very competitive, and VA programs often have borrower-friendly features. If you’re eligible, it’s worth comparing VA quotes against conventional quotes to see which option gives you the best combination of rate and fees.

If you’re looking at an fha cash out refinance, pay close attention to mortgage insurance costs. FHA can open doors, but the insurance premiums can change the “true cost” of the loan. This is where a refinance mortgage rates calculator (and a careful APR comparison) can make the decision obvious.

The goal is not just to refinance—it’s to refinance into the right structure for your financial life.

No Closing Cost Refinance: Convenient, But Not Always Cheaper

A no closing cost refinance can be helpful if you don’t want to pay fees upfront. But “no closing cost” usually means the costs are shifted somewhere else—either rolled into the loan amount or offset by a higher interest rate.

Use a refinance home loan calculator to compare a no-cost option against a standard refinance with fees paid at closing. If you plan to sell or refinance again soon, no-cost can make sense. If you’re staying long-term, paying costs upfront might deliver bigger lifetime savings.

Best Refinance Companies: How to Choose and What to Ask

Choosing between the best refinance companies isn’t just about who has the lowest advertised rate. You’re picking a partner to handle underwriting, timelines, documentation, and funding. The best refinance lenders usually win because they’re transparent about fees, fast with communication, and consistent during the closing process.

When comparing lenders, ask:

- What are the total lender fees and third-party costs?

- How long is the rate lock, and what happens if closing is delayed?

- Can you provide a full Loan Estimate?

- Do you specialize in my scenario (self-employed, high DTI, refinance investment property, etc.)?

Also compare refinance home loan rates across at least three lenders on the same day. That’s how you’ll see what’s truly competitive in the market and identify which offer actually matches the current refinance mortgage rates environment.

Refinance My Mortgage: A Simple Step-by-Step Plan

If your goal is to refinance my mortgage without wasting time, here’s a simple plan that works:

- Check mortgage refinance rates today and confirm the general trend.

- Run a refinance mortgage calculator to estimate savings and break-even.

- Decide your purpose: lower payment, shorten term, or cash-out.

- Collect quotes and compare current refinance rates and fees side-by-side.

- Pick your lender, lock the rate, and submit documents quickly.

- Review the Loan Estimate and Closing Disclosure carefully before you sign.

If you’re doing this to refinance my home loan for a better monthly payment, focus on break-even time and total costs. If you’re doing it for cash-out, focus on new loan balance and long-term affordability.

{kind=link}

{kind=link}

{kind=link}