Veteran Administration home loans are a type of mortgage backed by the U.S. Department of Veterans Affairs, designed to help eligible veterans, active-duty service members, and certain members of the National Guard and Reserves achieve homeownership. These loans offer several advantages, including no down payment, no private mortgage insurance (PMI), and competitive interest rates. With these benefits, veterans can overcome the challenges of today’s housing market, where the current VA mortgage rates in Utah can vary. In this article, we will provide complete VA loans information with insights on the following topics: ‘Benefits of VA Home Loans’, ‘Current VA Mortgage Rates in Utah’, ‘Utah VA Home Loan Options’, and ‘How to Submit a VA Request for Certificate of Eligibility’.

Benefits of Veteran Administration Home Loans

One of the most significant benefits of Veteran Administration home loans is the ability to purchase a home without a down payment, which saves veterans thousands of dollars upfront. Moreover, VA mortgage rates in Utah are generally lower than those of conventional loans, which helps veterans save even more over the life of the loan. Another advantage is that these loans do not require private mortgage insurance (PMI), making monthly payments more affordable. The flexible VA eligibility criteria also make it easier for veterans to qualify for home loans than traditional financing options.

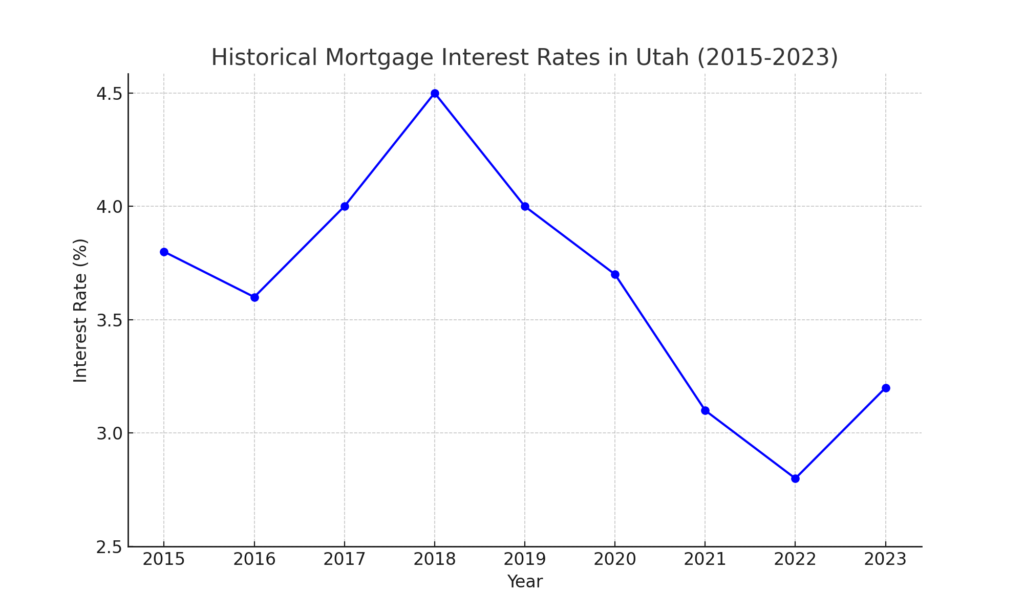

Current VA Mortgage Rates in Utah

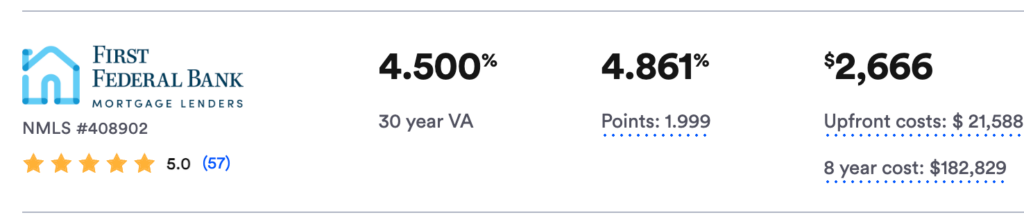

As of September 20, 2024, mortgage rates for Utah veterans seeking VA home loans start as low as 4.5%. However, these rates fluctuate based on various factors, such as economic conditions and individual creditworthiness. It is essential to regularly check the current VA mortgage rates Utah and compare them with other loan products. This will ensure you secure the best possible interest rate when applying for a loan. Veterans should also consider VA refinance rates if they are looking to adjust the terms of an existing VA loan for a better rate.

30-Year VA Mortgage Rate as of September 20, 2024

Utah VA Home Loan Options

Veterans in Utah have a range of mortgage options, including conventional loans, FHA loans, and USDA loans. However, for eligible veterans, the Utah VA home loan remains one of the most attractive choices. Not only do these loans offer lower interest rates, but the best VA mortgage lenders also provide flexible terms tailored to veterans’ needs. Additionally, understanding VA credit score requirements and VA appraisal requirements is crucial for navigating the loan process. Veterans should compare the various loan types and evaluate which option best fits their circumstances and financial goals.

How to Submit a VA Request for Certificate of Eligibility for a Home Loan

To apply for a VA home loan, veterans must obtain a VA certificate known as the Certificate of Eligibility (COE). This document verifies that you meet the necessary VA eligibility requirements to access the benefits of the loan program. The VA request for Certificate of Eligibility can be submitted online via the VA’s eBenefits portal, by mail, or through your lender. Along with your service dates and discharge status, this certificate is a key document for processing the loan. Veterans should also be mindful of the VA credit score requirements and VA appraisal requirements to ensure a smooth loan approval process.

Conclusion: Exploring Resources and GI Bill Benefits

In conclusion, the Utah VA home loan program offers a fantastic opportunity for veterans to achieve homeownership with minimal financial barriers. By taking advantage of no down payment, no PMI, and the competitiveness of VA mortgage rates, veterans can secure a home loan that meets their needs. For more information, explore our resources on first-time homebuyer tips and understanding the home loan process. To learn more about GI Bill benefits, Veterans Affairs resources, and additional VA loan information, be sure to visit the official Veterans Affairs website. Properly utilizing these benefits can make all the difference in your homeownership journey.

Did you hear that? They’ve shut down the main reactor. We’ll be destroyed for sure. This is madness! We’re doomed! There’ll be no escape for the Princess this time. What’s that? Artoo! Artoo-Detoo, where are you? At last! Where have you been? They’re heading in this direction. What are we going to do? We’ll be sent to the spice mine of Kessel or smashed into who knows what! Wait a minute, where are you going? The Death Star plans are not in the main computer.

Home Buyers Need to Know This

Terminate her…immediately! Stand by, Chewie, here we go. Cut in the sublight engines. What the…? Aw, we’ve come out of hyperspace into a meteor shower. Some kind of asteroid collision.

Some kind of asteroid collision. It’s not on any of the charts. What’s going on? Our position is correct, except…no, Alderaan! What do you mean? Where is it? Thats what I’m trying to tell you, kid. It ain’t there. It’s been totally blown away. What? How? Destroyed…by the Empire! The entire starfleet couldn’t destroy the whole planet.

It’s a short range fighter. There aren’t any bases around here. Where did it come from? It sure is leaving in a big hurry. If they identify us, we’re in big trouble.

Looking to learn more information about First-time Home buying quicker, and from those living around you about their thoughts? Follow these links below to solve some of your commonly asked questions.

First-Time Homebuyer Grants and Assistance Programs in Utah

If you are a first-time home buyer that is looking for assistance programs for down payments, closing costs, or to reduce your interest rate. ClickHEREto find more programs that can help assist you in this journey.

Utah’s 3 Best Neighborhoods to Live in

Exploring Utah’s neighborhoods can be an exciting adventure, especially for first-time home buyers. Here are the top three of the best areas to consider living in. Click HERE to find out more.

Best School District of First Home Owners

If you are a first-time home buyer in Utah, choosing a house with excellent schools is a top priority. There are several districts in Utah that stand out for their quality of education and support for students. Click HEREto find out more.

Pros and Cons of Buying a Condo vs. a Single-Family Home in Utah

Deciding between a single-family home and a condo can be challenging in Utah, here are some things to consider. ClickHERE to find out more.

Top 3 Affordable Suburbs of Salt Lake City

Want to buy a home near SLC? There are plenty of options to consider when looking for affordable housing. Click HERE to find out more.

What does a Home Inspection Cover in Utah

If you want to find out more about what an inspector is looking at, and why you should have them look at your house you are moving in, clickHEREto find out more and see what other people think too.

To sell a home in Utah is a significant milestone, whether you’re a first-time buyer or an experienced homeowner. Utah’s real estate market is thriving, offering unique opportunities and challenges. This guide will walk you through essential tips for both buying and selling homes in Utah, ensuring a smooth and successful experience. If you’re looking to sell a home in Utah, it’s important to understand the local market dynamics and pricing trends. Our comprehensive guide covers everything you need to know to sell a home in Utah, from staging tips to closing costs. Working with a knowledgeable real estate agent can significantly boost your efforts to sell a home in Utah quickly and efficiently.

Understanding Utah’s Real Estate Market

Utah’s real estate market is known for its strong growth and competitive nature. Key factors driving this include a robust job market, high quality of life, and beautiful natural surroundings. Understanding these market dynamics is crucial whether you’re buying or selling

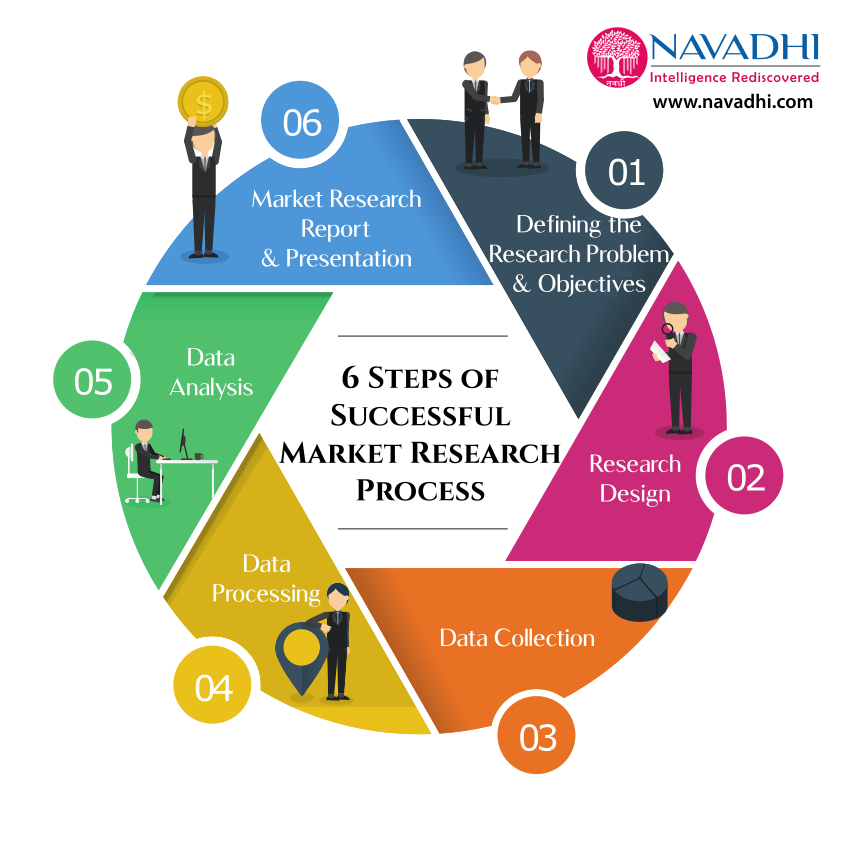

Market Research

Understanding your local market is crucial. Look at recently sold homes comparable to yours to get a sense of a fair asking price. Pay attention to the prices or availability of homes, market predictions, and average home values. First-time homebuyers you may feel inexperienced and need some guidance in navigating the mortgage process. Even existing homeowners you may be looking for information about different mortgage refinance options or even the process of how to sell your home. Real estate investors want knowledge of investment property financing and maximizing returns. By catering to these specific needs, Mortgage Rate Utah can provide all the information needed for Utah homebuyers. We want to be your one stop shop for learning about your mortgage options here in Utah!

Tools

There are various websites that can be used to discover market trends and reports for the housing market. These include your popular sites like Zillow or Redfin. If you’re looking for localized information visit local real estate website like Utah Real Estate. Information on the latest housing trends can be found at various locations, including local news channels. These channels may offer news regarding fluctuations in prices or availability of homes, market predictions, and average home values. Local market trends, economic reports, and detailed information specific to the Utah and Salt Lake housing market can be found on local websites and associations. Practical advice on buying & selling, mortgage options, and financial advice can be found for first-time buyers in Utah.

Preparing Your Home

Before you welcome potential buyers, it’s important to make your home well-presented. First impressions are key, so maintain a well-kept lawn, trimmed greenery, and a welcoming entrance. Get rid of any excess furniture and personal items to create a sense of spaciousness. Potential buyers should be able to envision themselves living in your home, not overwhelmed by your belongings. Stage your furniture strategically to enhance flow functionality of your home. A clean and inviting home showcases its potential to buyers.

Listing Your House

Once your home is market-ready, it’s time to officially put it on the market. This involves partnering with a real estate agent who will handle the listing process. They will take professional photos to showcase your home online as well as creating an appealing listing description highlighting its key features. This information will be uploaded to a Multiple Listing Service, which ensures maximum exposure to potential buyers and their agents. Your agent will also schedule open houses and individual showsing to allow buyers to tour your property. Throughout this process, you’ll work with your agent to review and potential negotiable offers to secure the best possible sale price for your home.

Closing

Closing represents the final hurdle in your home selling journey. It typically takes place in a title company’s office with all relevant parties present. This usually includes yourself, the real agent, the buyer’s agent, and a closing agent. Here, loan documents, title transfers, and closing disclosures will all be thoroughly reviewed and signed. Once everything is in order and all parties have signed, the deed is officially transferred to the buyer, and you’ll receive the sale proceeds minus any closing costs. You’ve successfully navigated the home selling process.

Tips for First-Time Home buyers

Ensure your credit score is in good standing. A higher score can help you secure a better mortgage rate. Your credit score significantly impacts your mortgage options. Obtain a free credit report and review it for errors. Aim for a score of 620 or higher for most conventional loans, but higher scores can qualify you for better rates.

Lenders look at your debt-to-income (DTI) ratio to determine your ability to manage monthly payments. Calculate this by dividing your total monthly debt payments by your gross monthly income.

Factor in all the costs of your new home, closing costs, property taxes, matience and repairs, and utilities and HOA fees.

Many states, including Utah, offer programs that provide down payment assistance, low-interest loans, or tax credits to first-time buyers.

Research other loan options designed for first-time buyers. Such as, the Utah Housing Corporation which offer options with lower downpayments and favorable terms for you first-time buyers.

Tips for Existing Home Owners

Determine the equity you have in your current home. This is the difference between your home’s market value and the remaining balance on your mortgage. Your equity can significantly impact your budget for the new home.

Review the terms of your existing mortgage. Understand any penalties for early repayment or conditions for portability, which allows you to transfer your mortgage to a new property.

Conduct a comparative market analysis (CMA) to estimate your home’s current market value. Your real estate agent can assist with this, considering recent sales of similar properties in your area.

Plan for selling costs, agent commisions, staging and repairs, and closing costs.

Decide how much of your home equity you will use as a down payment for the new property. Consider leaving some equity untouched for financial flexibility. If there is a gap between selling your current home and buying a new one, consider a bridge loan. This short-term loan can help you cover the down payment on the new property.

Utilize budgeting apps and tools to track your income, expenses, and savings. This helps you stay organized and ensures you’re on track with your financial plan.

Conclusion

Buying or selling a home in Utah is an exciting journey, filled with opportunities and challenges. Whether you’re a new homebuyer eager to plant roots or a seasoned homeowner looking to make a change, understanding the local market, preparing thoroughly, and seeking professional guidance are key to a successful transaction. By following these tips, you can navigate the process with confidence and achieve your real estate goals.

Buying your house is a milestone that comes with a mix of emotions, like excitement, anticipation and some uncertainty. Navigating Utah’s housing market can be overwhelming for newcomers. This blog offers tips to help you confidently start your journey as first-time homebuyers in Utah. Learn about mortgages, manage finances, and understand real estate to make informed choices for your goals and lifestyle.

Fixed Rate Mortgages:

For first-time homebuyers in Utah, having a grasp of mortgage options is essential. Consider two mortgage types: fixed-rate and adjustable-rate (ARMs). Each type has its advantages and disadvantages that can impact your stability and monthly payments.

With these loans, you’ll have payments throughout the loan term, which typically lasts for 15 or 30 years. This stability simplifies budgeting and ensures your payments remain steady, giving you peace of mind.

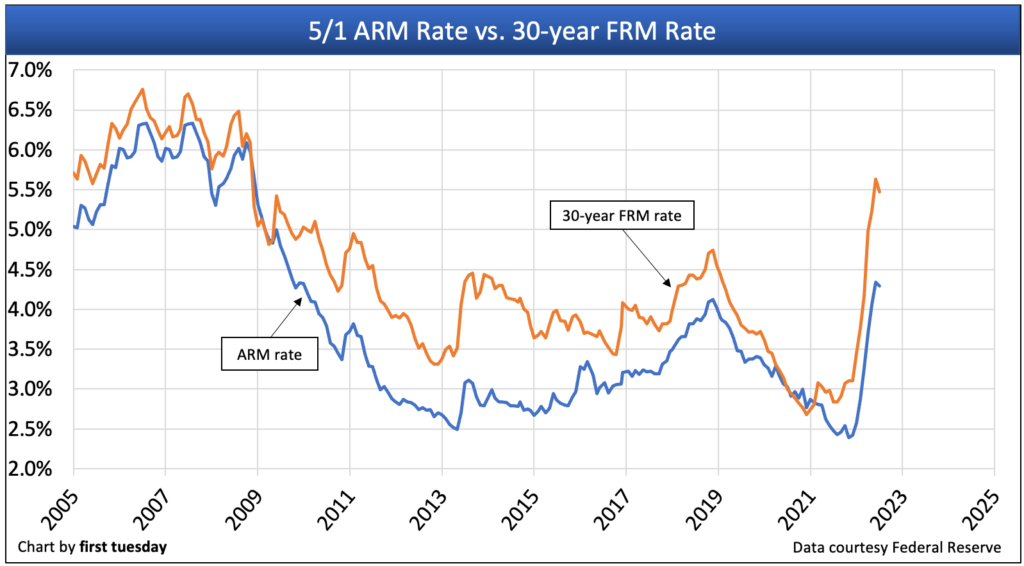

Adjustable Rate Mortgages (ARMs); ARMs usually start with interest rates that can change based on market conditions after a fixed period. While ARMs may offer payments there’s a risk of facing higher payments, down the line.

Fixed rate home loans work well for individuals intending to live in their homes for a period and prefer the stability of payments. On the other hand, adjustable rate mortgages (ARMs) may be more suitable for those planning to relocate within a year or foresee an increase in income enabling them to take advantage of lower initial rates.

When selecting a mortgage it’s crucial to assess your status, future goals, and comfort level with risks. Consulting a mortgage specialist can provide personalized advice for your situation. Achieving homeownership starts with proper financial management.

Budgeting Tips:

Saving for a Down Payment; Aim to put down 20% to avoid PMI and get better loan terms. Nonetheless there are loan options that require down payments if reaching 20% proves challenging.

Understanding Closing Expenses; Besides the payment budgeting should account for closing costs, which typically range from 2% to 5% of the loan amount. These expenses cover charges related to appraisals, inspections, title insurance and other administrative fees.

Preparing for Costs; Homeownership entails expenses, like property taxes, homeowners insurance premiums and upkeep expenditures.

Creating an Emergency Fund; Unexpected repairs and maintenance can crop up unexpectedly. Having an emergency fund, to three to six months of living expenses can provide a financial safety net and peace of mind.

A thorough budget ensures you are financially ready for all aspects of owning a home. In addition to the purchase costs it is essential to include expenses for home maintenance and safeguarding your investment. Understanding real estate trends is vital for making decisions. Utah’s housing market is shaped by job growth, population trends, and regional economic conditions. For a deeper understanding to help you buy and sell your home, check out another one of our blog posts: https://www.mortgagerateutah.com/how-to-sell-or-buy-a-home-in-utah/

Expert Interview: Jane Doe, Real Estate Specialist

To gain insights we consulted Jane Doe, a real estate professional with over two decades of experience in the Utah market.

Q; What are the trends in the Utah housing market?

Jane Doe: The Utah housing market is witnessing growth due to a robust job market and an influx of new residents. There is a rising demand for homes, in areas as more individuals look for residences and outdoor spaces. Prices have been going up. There are still chances for people buying a home for the time especially in up and coming neighborhoods.

Q; Which neighborhoods are seeing property values rise and which areas might be good for long term investment?

Jane Doe: Places like Sugar House and The Avenues are in demand. Have experienced significant value growth. For long term investing consider neighborhoods such as South Salt Lake and Midvale which are currently more affordable yet showing growth due to new developments and improved amenities.

Q; What tips do you have for first time homebuyers in Utah?

Jane Doe: Begin by getting pre approved for a mortgage to understand your scope. Collaborate with a real estate agent with the market. Take your time and research neighborhoods and properties thoroughly. Lastly, don’t rush your decision; ensure that the home aligns with your needs and budget.

In conclusion, Jane Doe emphasizes staying updated on market trends and collaborating with experts. Being aware of which areas are experiencing value appreciation can aid you in making an investment that will pay off in the term.

Embarking on the journey of purchasing a home in Utah is an adventure filled with both opportunities and obstacles. Learn about mortgages, manage finances wisely, and understand the housing market to navigate home buying confidently. Owning a home means creating a space for your future, cherishing memories, and feeling a sense of belonging.

Steps to Successfully Purchase Your Utah Home

Although purchasing a home may appear daunting at glance having the right information and support can make it more approachable and fulfilling. Here’s a summary of steps and advice to assist you along the way:

Explore Your Mortgage Options: Decide whether a fixed rate or adjustable rate mortgage aligns with your circumstances and future goals.

Manage Your Finances Wisely: Set aside savings for a payment account for closing expenses and establish a plan that considers ongoing costs along with an emergency fund.

Stay Updated on Local Real Estate Trends: Collaborate with housing specialists to explore neighborhoods and identify promising investment opportunities.

Obtain Pre Approval: Get pre-approved for a mortgage to know your limits and make your offer more appealing to sellers.

Engage with a Real Estate Professional: Partner with a Utah real estate agent for guidance through the process.

Remember to be patient and thorough: Research thoroughly to find a home that fits your needs and budget.

Think about the run: Consider future impacts like property value appreciation and potential home upgrades when making your purchase.

First time homebuyers in Utah? Head over to Mortgage Rate Utah for resources, expert advice and tools to support you at every stage. Our detailed guides, interactive tools and local insights are tailored to make the process smoother and more enjoyable, for first time homebuyers.

Conclusion

Purchasing a home is a decision that requires careful consideration. Use Mortgage Rate Utah’s tips and resources to confidently navigate the homebuying process. Whether you’re beginning to save for a down payment or actively searching for properties, having a plan and understanding the market will set you up for success. For first-time homebuyers in Utah, it’s about finding a place that truly feels like home. With planning, informed choices and appropriate assistance you can turn your dream of owning a home in Utah into reality. Happy searching for your dream home!

When it comes to buying your first home, it is vital to understand home interest rates in Utah. First, there are two different kinds of interest rates we can take a look at, fixed vs. adjusted mortgages. Understanding the advantages and circumstances in which fixed interest rates can help you the most can be the best financial decision when you get home. Fixed interest rate is a mortgage loan interest rate the remains the same over the entire course of the loan. This is a consistent option that can make budgeting easier when it comes to long term planning. If you are a buyer that prefers a more predictable financial plan, plan to stay in your home for a long period of time, this is the plan for you. Adjustable rate mortgage (ARMs) is a unique offer than can greatly benefit first time buyers under the right circumstances. ARM’s offer an initial lower interest rate the is adjustable over time. They tend to start with a lower rate compared to fixed loans. However, the rate and monthly payment can change annual after the initial fixed period of time. This is the best option if the buyer is planning to move or refinance within just a few years. This can help buyers save up money within the period of time there is the lower initial rate. It is also important to take these initial rates can also allow the buyer to qualify for a larger loan amount, which can be beneficial in the competitive market Utah has to offer.

Over the past five years, Utah’s home prices have surged by 72%. In just the two years between 2020 and 2022, the median home prices in Utah saw almost a 50% increase. In June of 2022, prices began to decline. As of February 2024, the median home price in Utah was $542,000. With that comes the minimum down payment at 3% comes to $16,275. The average down payment is 16.4%, coming to $43,488. This number can be infeasible for first time home buyers. Which is why there are first time home buyer programs that exist. The is the conventiional 97, offered by Freddie Mac. With 3% down and a 620 minimum credit score, you are able to stop paying mortgage insurance after a few years. There are no income limits, however, it is meant just single unit residents only. FHA loans are backed by the Federal Housing Administration, requiring 3.5% down and a minimum of 580 credit score. This is a great option of you are rebuilding your credit score or in need of making smaller payments. This loan allows for properties with up to four living units. Lastly, there are USDA loans for those with low to moderate incomes buying in rural areas. Individuals with a 640 credit score, allow for low insurance rates. There is no downpayment required. It is important to get multiple quotes. Go to at least 3 different lenders to find the best rate for you. Your bank may not offer the best rates! Compare your loan estimates, look for APRs, monthly payment rates, locked fees, and closing costs. These are all factors that play into understanding home interest rates in Utah, especially when it comes to being a first time home buyer.

When my husband and I purchased our first home in Salt Lake City, Utah, it seemed like there were endless forms to fill out and too many documents to sign, followed by at least an hour of signing more closing document to wrap up the sale. The amount of paperwork involved with buying a home feels endless. However, It’s important to know what documents you’re signing at closing, and why you’re signing them because purchasing a home is a huge investment!

Don’t drown in closing document confusion! Read on for help.

I want to help first-time homebuyers understand what they’ll be reviewing during closing, and/or give experienced homebuyers a friendly reminder. So, below is a list of the most common closing documents you’ll encounter and a brief description of what they entail. Documents are in order alphabetically, by name.

The Affidavit of Title

The Affidavit of Title is a legal document which establishes that the seller holds the title to the property. The new homeowner will sign this document upon taking ownership. Also, it includes any information about liens or other title issues for that property.

The Certificate of Occupancy

The Certificate of Occupancy is a document that’s provided to the homebuyer and contains the address and description of the property. It verifies that it us up to code, which serves as proof that the property is fit to live in and fit for its purpose. This document only applies to new-build homes, therefore anyone closing on an existing home doesn’t need to worry about this one.

The Closing Disclosure

A Closing Disclosure is a form for the new homebuyer which gives the final details of the mortgage loan. It includes the loan terms, projected monthly payments, and how much the new homebuyer will pay in fees and other costs to get the mortgage (closing costs).

The Deed

A Deed is a legal document that transfers ownership of home from the current owner to the new buyer. It also contains a description of the property boundaries and any real property that it contains. Therefore, it is crucial to review this document for accuracy. Every real estate deed must be notarized and filed with the local government in order for the new homebuyer to sell the property, refinance the property, or obtain a line of credit on it. The title insurance company generally performs this task, but it’s important for the homebuyer to verify the process.

The Home Inspection Report is a detailed list of the the condition of the home and its components. It generally includes the following: foundation, exterior, bathroom fixtures, appliances, roof, plumbing, HVAC system, gas system, and electrical system. An inspector will visually examine the home and then provide the report. This is done prior to closing so that the buyer can review the document and request fixes to be made or even change their mind about purchasing the property.

The Homeowners Insurance

Lenders in Utah require homeowners insurance, and will ask for proof of insurance as one of the closing documents. Lenders want proof that their investment is protected.

The Initial Escrow Statement

The Initial Escrow Statement also goes by the name of the “Initial Escrow Disclosure”. This document outlines how the escrow account is set up and what expenses it covers. It covers common elements such as property taxes, mortgage insurance, homeowners association dues, etc.

The Loan Application

The Loan Application is the homebuyer’s acknowledgement that they understand the terms of the loan and their financial obligation to repay it. The new homebuyer will review this document along with the mortgage application. Therefore, it is important to review for accuracy and notify of any changes.

The Mortgage

The mortgage also goes by the name “The Deed of Trust.” This is an agreement between the new homebuyer and a lender that allows the homeowner to borrow money to purchase or refinance a home. The mortgage legally allows the lender to put the home up as collateral for the loan.

The Promissory Note describes the homebuyer’s commitment and responsibility to the mortgage loan. It will state the amount of the loan, the interest rate, repayment schedule and any consequences of defaulting.

The Purchase Agreement

The Purchase Agreement is sometimes called a “Purchase and Sale Agreement” or a “Real Estate Purchase Contract (REPC)”. It is a legally binding document between the buyer and seller for real estate purchases. The Purchase Agreement contains details such as: new homebuyer info, purchase date, purchase price, purchase details (property and any included amenities), how it will be paid for (loan, cash, etc.) It also contains details such as appraisals, conditions of purchase, etc. Utah law requires licensed Real Estate agents to use the REPC form, although the home buyer and home seller can agree to alter or delete its provisions, or to use a different form.

The Sellers Disclosure

The Sellers Disclosure is a document that lists in detail any issues with a home. In the state of Utah, a seller is required by law to disclose material defects and latent defects. Material defects are things you can easily see or find. Latent defects are not easily seen or not obviously apparent.

The Title Document is a list of all previous owners of the home and any liens or other clouds on the title. You’ll need to pay off any additional/existing liens in order to have a free and clear title. It’s important to review this document to prevent delays in the closing process. When you buy a home, you acquire the title, which represents your ownership rights.

The Title Insurance Policy

The Title Insurance Policy is a document that outlines protections for the lender. Hidden title hazards can emerge after purchasing a home, but title insurance can offer protection against them.

The Transfer of Tax Declaration

The Transfer of Tax Declaration is a document that lists the taxes owed for the transfer of the property. Utah does not charge a real estate transfer tax, therefore this is not a concern for Utah homebuyers as it is not a required closing document.

Thanks for Reading!

I hope this article was helpful! Now you’ve seen a quick summary of the closing documents you’ll encounter when buying a home. Also, depending on which state you’re purchasing a home in, there may be more or fewer documents to sign. If you want more details or additional information, then please check out these posts as well!

As a first-time homebuyer in Utah, navigating the mortgage world can seem very overwhelming. Understanding the various home loan options available to you is important in making a credible decision that best fits your pocket. We will explore the major types of mortgages available, like fixed-rate, adjustable-rate, FHA, and VA loans, which will get you started on the way to becoming a homeowner.

Fixed-Rate Mortgage

The fixed-rate mortgage is the most popular choice of many first-time homebuyers. In this kind of loan, your interest rate doesn’t move during the life of the loan. Because of this, your monthly payment will be predictable. This stability makes it easier to budget and provides peace of mind that your payments won’t change over time. Checking current mortgage rates can help you determine if a fixed-rate mortgage is the right choice for you.

Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage enables a lower interest rate at the beginning compared to fixed-rate mortgages. However, it may be changed according to the market conditions after an initial fixed period. ARMs are good if you think you will sell or refinance before the adjustable period kicks in; however, you are also risking increasing interest rates. Using a mortgage payment calculator can help you estimate potential changes in your monthly payments with an ARM.

FHA Loans

The Federal Housing Administration insures FHA loans, which are generally used by first-time homebuyers and help buyers with slightly worse credit scores or those wanting to pay a smaller down payment. Because the requirements in qualifying are laxer, an FHA loan does open up the possibility of homeownership to buyers who otherwise would not be able to qualify for conventional loans. It’s important to regularly check FHA loan rates as they can vary and impact your decision.

VA Loans

VA loans are for veterans, active duty, and eligible spouses. They are guaranteed by the Department of Veterans Affairs and therefore come with no down payment, no private mortgage insurance, and competitive interest rates. VA loans are a great option for eligible first-time homebuyers. Checking current mortgage rates specifically for VA loans can provide you with an accurate picture of the benefits.

USDA Loans

Another excellent rural Utah first-time homebuyer option is the USDA loan. The United States Department of Agriculture guarantees these loans with no down payment and lower interest rates, also cutting mortgage insurance costs. Offering an excellent entry point to begin homeownership outside center cities, USDA loans aim to provide for low- to moderate-income purchasers in eligible rural areas.

Conclusion

First in the process for successful Utah homeownership is an understanding of your options when it comes to mortgages. It’s all about weighing the pros against the cons of a fixed-rate mortgage, an adjustable-rate mortgage, an FHA loan, or a VA loan as they best fit your financial situation and long-term plans. By making this informed decision, you will most definitely be on your way to owning your dream home in Utah. Utilizing tools such as a loan calculator and regularly checking mortgage rates can help you make a more informed and confident decision.

Discover the true costs of homeownership beyond mortgage rates and calculators. Learn about property taxes, insurance, PMI, and more

When I purchased my first home in 2018 and joined the ranks of homeownership, I thought I had it made. Purchasing a home is one of the most significant financial decisions one can make. I remember sitting down at my MacBook and putting numbers into a mortgage calculator trying to figure out how much a loan I could qualify for. I swam through a sea of acronyms FHA, VA, HELOC, PMI, and it felt like a million others. In the end I was confused and couldn’t determine where to turn. I felt like a needed to hire a certified financial analyst to clear up my understanding.

My first house wasn’t quite as nice as this one.

The Basics: Mortgages Rates and Loan Calculators

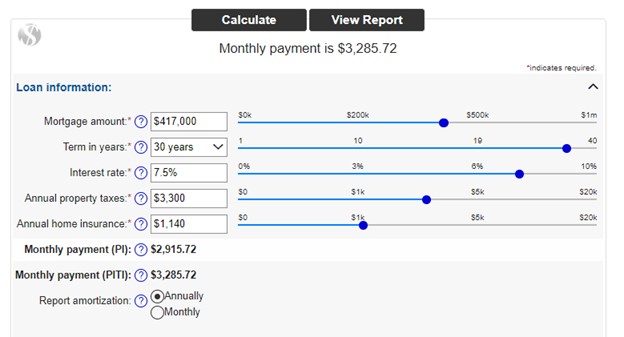

A good mortgage calculator estimates your mortgage payment by using the home’s price, loan interest rate, loan term, estimated credit score, and down payment.

When most people think about buying a home, they start with the monthly payment to the bank often the largest outgoing expense. A good mortgage calculator estimates your mortgage payment by using the homes price, loan interest rate, loan term, estimated credit score, and down payment to calculate an estimated monthly payment. They will often help provide an estimate of monthly taxes and private mortgage insurance (PMI) as well. You can find an example of a mortgage calculator here. Another great, but slightly more technical calculator is the Zions Bank calculator. It provides estimated amortization and allows you to modify the terms lengths and customize the calculator. I prefer the Zion’s calculator because it gives you a solid report that provides all the details. To learn more about which mortgage provider is right for you check out this article.

Mortgage Payment Calculation Example:

Buying a home in Utah is expensive. Per Zillow the average Utah home value is hovering around $522k. https://www.zillow.com/home-values/55/ut/ . Buying this home with a 20% down payment means the mortgage amount would be ~$417k with a $104k down payment. Property taxes in Utah hover around 0.64% or for our home about $3,300 yearly. Insurance in Utah averages $1140 per year according to a NerdWallet analysis. Plugging these values into our mortgage calculator we get an estimated payment of $3,285.72

Screenshot from the Zions Bank Mortgage Calculator. Showing the Example Calculations for the average Utah Mortgage.

A lot of people stop here and assume this is the total cost of owning a home. However, in reality this is just the beginning.

Beyond the Basics: Understanding the Additional Costs of Homeownership in Utah

While the mortgage payment itself is significant other costs can add up quickly as well. Here are some of key additional expenses you should consider.

Property Taxes:

These taxes are based on the assessed value of your home and can vary widely depending on the location. Obviously, differences in tax rates between counties and cities can have a considerable impact on the overall tax rate. Local government websites typically provide information on the property tax rates for your area. One thing to remember is that assessed tax values do not always match the price you’re paying.

Homeowners insurance is a must-have to protect your investment. The cost of insurance can vary depending on the location, value of the home, and level of coverage you choose. Standard policies typically protect against fire, theft, and some natural disasters. Factors that a lot of people don’t consider are distances from fire hydrants and fire stations, proximity to wooded areas, or if the property is in the flood plain. As a result, purchasing insurance for a home that is in a wooded area next to a river can be significantly more expensive then buying insurance for a comparably priced home in the suburbs.

Private Mortgage Insurance (PMI):

If your down payment is less then 20% of your home purchase price, you will likely need to pay for PMI. This insurance protects the lender in case you fail to pay the loan. The cost of PMI can range from 0.3% to 1.5% of the original loan amount annually and highly depends on the credit score and size of the down payment. Fortunately PMI can often be removed as a requirement early if the homes value increases. Following up with your mortgage provider or lender after a year or two can save thousands of dollars if the PMI requirements are dropped.

Homeowners Association (HOA) Fees:

Purchasing a home in a community with a HOA can be a blessing or a curse. These fees typically cover the cost of maintaining common areas and amenities, such as swimming pools, club houses, gyms, parks, and landscaping. These fees vary widely by the type of community. Always do your due diligence and ensure that these types of fees are included in your home budget.

Repairs and Maintenance: The Hidden Costs

Owning a home means that you are responsible for all maintenance and repairs. Unlike renting, where the landlord is responsible for ensuring the home is in tip-top shape, homeowners must budget for the routine upkeep and unexpected repairs.

Regular Maintenance:

Typically these types of repairs are not that expensive, but are ongoing. For myself the real cost here is the tools or “toys” that I’ve acquired to do the maintenance. Mowing the lawn has always been one of my favorite pastimes. At my first home I bought a $300 lawn mower from Walmart and I felt like I was giving up a kidney. This last summer I spent “a lot” more on a zero turn mower. Things like pressure washers, impact drivers, saws, and batteries for everything can be thousands of dollars in total. You don’t have to purchase everything all at once, but overtime you will likely find significant resources going towards these routine projects.

Major Repairs:

Once in a while the unthinkable happens and something major breaks. For me it was my basement freezer kicking the bucket on hot day and water leaking into and ruining the flooring and wall. It was a few thousand dollars to replace the appliances, make a few minor repairs to the walls/flooring. Luckily we were ready for it. I’ve always had a emergency fund set aside for these types of issues. Other common problems people face are water damage, roof repairs, foundation repairs, and plumbing/heating issues. Insurance may be able to cover some of these costs if they exceed the deductible, but depending on your policy you may need to front the first few thousand dollars before the insurance policy can kick in.

Improvements:

When my wife and I looked at our first home we saw a lot of potential, but unfortunately we didn’t budget for it. We discussed remodeling the kitchen and bathrooms, breaking down walls, and redoing flooring; but at our first home we never found the wiggle room to make any of that happen. We did a lot of the easy improvement, but we didn’t budget for anything major.

When my wife and I looked at our first home we saw a lot of potential, but unfortunately we didn’t budget for it. We discussed remodeling the kitchen and bathrooms, breaking down walls, and redoing flooring; but at our first home we never found the wiggle room to make any of that happen. We did a lot of the easy improvement, but we didn’t budget for anything major.

The Role of a Financial Professional

Navigating the complexities of homeownership can be challenging, and consulting with a financial professional can provide valuable guidance. A Certified Financial Planner (CFP) specializes in helping clients with comprehensive financial planning. They can assist in budgeting for homeownership, managing debt, and planning for future expenses. Their expertise can be invaluable in ensuring you make informed decisions throughout the home buying process.

Many home buyers will look to their real estate agent for financial guidance. It’s important to remember that real estate agents, although they are experienced in helping buy and sell homes, are not financial professionals. Their role ends at the point of purchase and their goals and motivations may not align with your future homeownership. This year a major court ruling pointed out an inherent conflict of interest that real estate agents face when aiding the clients.

Tips for effective Financial Planning:

To ensure that you can afford the home of your dreams and associated costs, effective financial planning is essential. Here are some tips to help manage the process.

Create a detailed budget: outline your current monthly expenses. Determine which expenses will continue to exist after you buy a home and which will go away. Estimate the mortgage, repair, taxes, and other costs of owning a home as well as allowing for building an emergency fund and additional savings. Compare this to your income to ensure that you can comfortably afford your home without stretching too thin.

Start Building an Emergency Fund: Get some funds set aside for homeownership. In both homes I’ve purchased we discovered some repairs needed to be made within the first six months living in the home. You never know if the sprinklers aren’t going to work, or the furnace won’t ignite, or if shower has a leak until you’ve lived there for a couple of months.

Consider Future Expenses: If you’re planning on remodeling the basement to build the ultimate man cave, you should start planning for it now. The cost of homeownership doesn’t end when the mortgage documents are signed. Plan now so that you can meet your future needs later. If you’re looking to start saving money CD’s could be a great place to start.

Review Your insurance needs: Evaluate the risks and assets and you need to protect. Ensure that what maybe a giant inconvenience doesn’t turn into a financial disaster through proper risk management.

Conclusion: Beyond The Cost

Purchasing a home is a monumental financial commitment that extends far beyond the simple calculation of mortgage rates and monthly payments. As we’ve explored understanding a prepaying to the myriad of costs are crucial steps to ensuring that homeownership is financially sustainable and enjoyable.

A street of modern houses on a development south of Salt Lake City in Utah, USA.

Navigating Home Interest Rates in Utah: Your Comprehensive Guide

When it comes to purchasing a home, understanding the nuances of home interest rates in Utah is crucial. Whether you’re a first-time homebuyer or looking to refinance, being informed about Utah mortgage interest rates can save you money and help you make the best financial decisions. In this guide, we’ll dive deep into mortgage interest rates in Utah, what influences them, and how you can secure the best rates possible.

Understanding Utah Mortgage Interest Rates

Utah mortgage interest rates are determined by various factors, including the Federal Reserve’s rate decisions, inflation, and the overall economic climate. Local factors such as Utah’s housing market trends and regional economic conditions also play a significant role. Mortgage lenders in Utah assess these factors to offer rates that reflect both national and local economic conditions.

Current Trends in Mortgage Interest Rates in Utah

As of the latest data, mortgage rates in Utah have been relatively stable, but they can fluctuate due to several reasons. Keeping an eye on these trends is essential for potential homebuyers and those looking to refinance. Currently, Utah mortgage interest rates are influenced by:

Economic Indicators: Employment rates, consumer confidence, and economic growth in Utah can impact mortgage rates. A robust economy typically leads to higher rates.

Federal Policies: The Federal Reserve’s policies on interest rates significantly affect mortgage rates. Any changes in the federal interest rate can lead to immediate adjustments in Utah mortgage interest rates. For more information, please visit Federal Reserve Economic Data (FRED).

Inflation: Higher inflation usually leads to higher mortgage rates as lenders need to maintain their profit margins.

How to Secure the Best Mortgage Rates in Utah

Securing the best mortgage interest rates in Utah requires a strategic approach. Here are some tips to help you get the best deal:

Improve Your Credit Score: Lenders offer lower rates to borrowers with higher credit scores. Check your credit report for any errors and work on improving your score by paying off debts and making timely payments. For more information, check out the Consumer Financial Protection Bureau (CFPB).

Compare Offers: Don’t settle for the first offer you receive. Compare rates from multiple lenders to ensure you’re getting the best deal. Utilize online tools to compare Utah mortgage interest rates from various lenders, such as Zillow Mortgage Rates.

Consider the Loan Term: Shorter loan terms often come with lower interest rates. While a 15-year mortgage might have higher monthly payments, it can save you money in the long run due to lower interest rates.

Lock in Your Rate: If you find a favorable rate, consider locking it in to protect yourself from potential increases in mortgage rates in Utah. Rate locks typically last for 30 to 60 days.

The Impact of Utah Mortgage Rates on Homebuyers

Understanding mortgage interest rates in Utah is vital for homebuyers as it directly affects their monthly payments and overall affordability. Lower rates mean lower monthly payments, which can make homeownership more accessible. Conversely, higher rates can increase your payments and limit the amount you can borrow.

For example, on a $300,000 mortgage, a 1% difference in interest rate can change your monthly payment by approximately $150. Over a 30-year mortgage term, this difference can amount to significant savings or costs.

Conclusion

Staying informed about home interest rates in Utah is essential for anyone looking to buy or refinance a home. By understanding the factors that influence Utah mortgage interest rates and implementing strategies to secure the best rates, you can make more informed decisions and potentially save thousands of dollars over the life of your mortgage. Remember, the key to navigating mortgage rates in Utah successfully is to stay educated, compare offers, and act when you find a favorable rate. Happy house hunting!