Self-employed borrowers face unique challenges when qualifying for a home loan. Traditional underwriting models were built for salaried employees, not entrepreneurs with fluctuating income. Fortunately, programs like bank statement home loans and other Non-QM options now make being self-employed and getting a mortgage far more accessible.

If you’ve been wondering, can a self-employed person get a mortgage? — This guide explains exactly how.

Bank Statement Home Loans for Self-Employed Borrowers

A mortgage for the self-employed with bank statements allows borrowers to qualify using 12–24 months of bank deposits instead of tax returns.

Unlike conventional loans, bank statement mortgage loans calculate income based on actual deposits, not net income after deductions. This makes them ideal for business owners who maximize write-offs.

How Bank Statement Mortgage Lenders Calculate Income

Most bank statement mortgage lenders:

- Review 12–24 months of personal or business bank statements

- Apply an expense ratio (often 50%)

- Average monthly deposits to determine qualifying income

This structure makes bank statement home loans one of the most popular options among the best mortgage lenders for self-employed borrowers.

Best Mortgage Lenders for Self Employed in 2026

Choosing the best mortgage lenders for self employed borrowers requires finding lenders that specialize in Non-QM products.

When comparing lenders, consider:

- best bank statement mortgage lenders

- best no doc mortgage lenders

- best non qm lenders

- best mortgage company for self employed

- best lender for self employed

- best mortgage broker for self employed

- best mortgage provider for self employed

The best in mortgage lenders for entrepreneurs understand fluctuating income and business deductions.

Internal Link Suggestion

If you have a Non-QM page, link like this:

Explore all Non-QM options here:

https://www.yourwebsite.com/non-qm-mortgage-programs

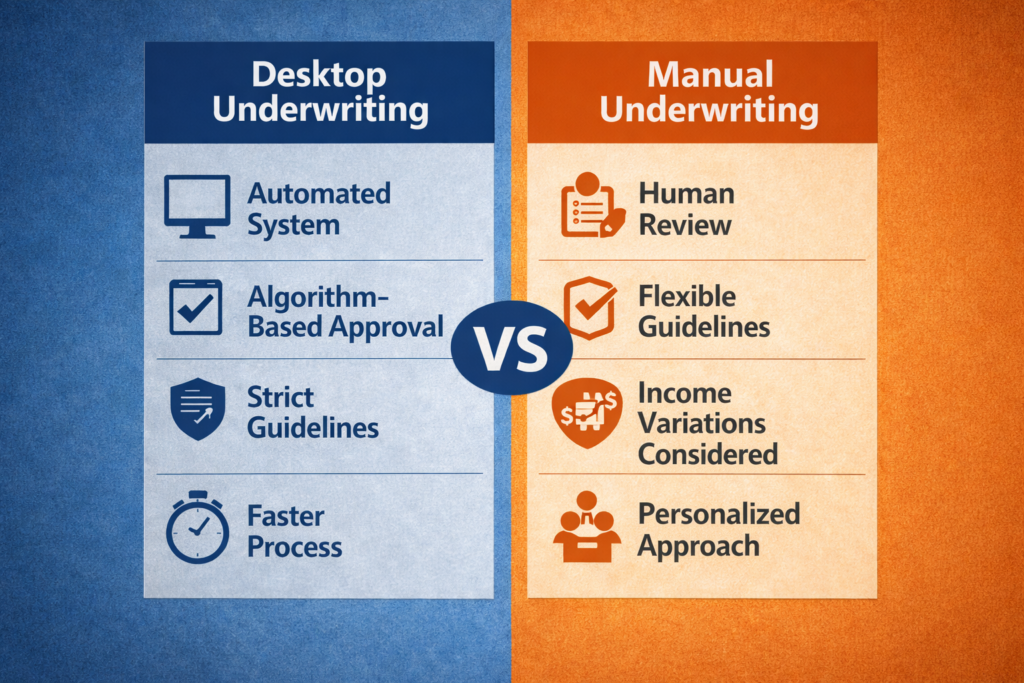

Desktop Underwriting vs Manual Underwriting

Understanding Desktop Underwriting vs Manual Underwriting can dramatically affect approval outcomes.

Desktop Underwriting (DU)

- Strict documentation requirements

- Automated approval system

- Used for conventional loans

Manual Underwriting

- Human review process

- Greater flexibility

- Ideal for self-employed borrowers

Many of the best home lenders for self-employed use manual underwriting when income is complex.

DSCR Loans for Real Estate Investors

If you own rental property, DSCR loans for real estate investors may be better than income-based loans.

Instead of verifying personal income, lenders qualify you based on rental property cash flow.

This makes DSCR programs a strong offering from the best non qm lenders.

Internal Link Suggestion

Learn more about DSCR loan programs here:

https://www.yourwebsite.com/dscr-loans-for-real-estate-investors

Anchor text suggestion: DSCR loans for real estate investors

ITIN Home Loans for Non-Citizens

Self-employed borrowers without a Social Security number may qualify for ITIN home loans for non-citizens.

These programs:

- Accept Individual Taxpayer Identification Numbers

- Often paired with a bank statement, mortgage lenders

- Provide alternative documentation options

Best Mortgage Refinance for Self-Employed Borrowers

Refinancing can help entrepreneurs access equity or lower rates.

Borrowers often search for:

- best mortgage refinance companies for self-employed

- best mortgage refinance for self employed

- best refinance companies for self employed

If your tax returns show limited income due to deductions, refinancing with bank statement mortgage loans may offer better qualification terms.

The best mortgage for self employed borrowers depends on the income structure.

You may prefer:

- bank statement, home loan,s if you maximize deductions

- DSCR loans for real estate investors if you scale rental properties

- ITIN home loans for non-citizens if you lack an SSN

- Manual underwriting if automated systems decline your file

If you previously researched the best mortgage for self employed 2021 or best mortgage for self employed 2022, you’ll find that today’s programs are more flexible and competitive.

Working with the best home loan lenders for self-employed individuals ensures your application is structured correctly from the beginning.

Can a Self-Employed Person Get a Mortgage?

Yes — and more options exist than ever before.

Whether you’re comparing:

- bank statement mortgage lenders

- best mortgage lenders for self employed

- best no doc mortgage lenders

- best mortgage provider for self employed

- best refinance companies for self employed

There is a solution that aligns with your business income.

If you’re serious about qualifying, start by speaking with the best lender for self-employed borrowers who understands how entrepreneurs earn, deduct, and grow income.