Navigating the real estate market in the Beehive State can be daunting, but understanding how to get a mortgage is the first real step toward homeownership. Many prospective home buyers start their journey by exploring the financial landscape of home loans —the real competitive edge comes from securing a mortgage pre-approval. This document proves to sellers that a mortgage lender has already vetted your finances and is ready to back your offer.

To start the process, you should research the best mortgage companies and best mortgage lenders available in the state of Utah. Experts encourage you to get a mortgage quote from several different sources to ensure you get the best deal. While some buyers prefer large national banks, others have found that working with a local mortgage broker offers help with the local markets and a more personalized experience.

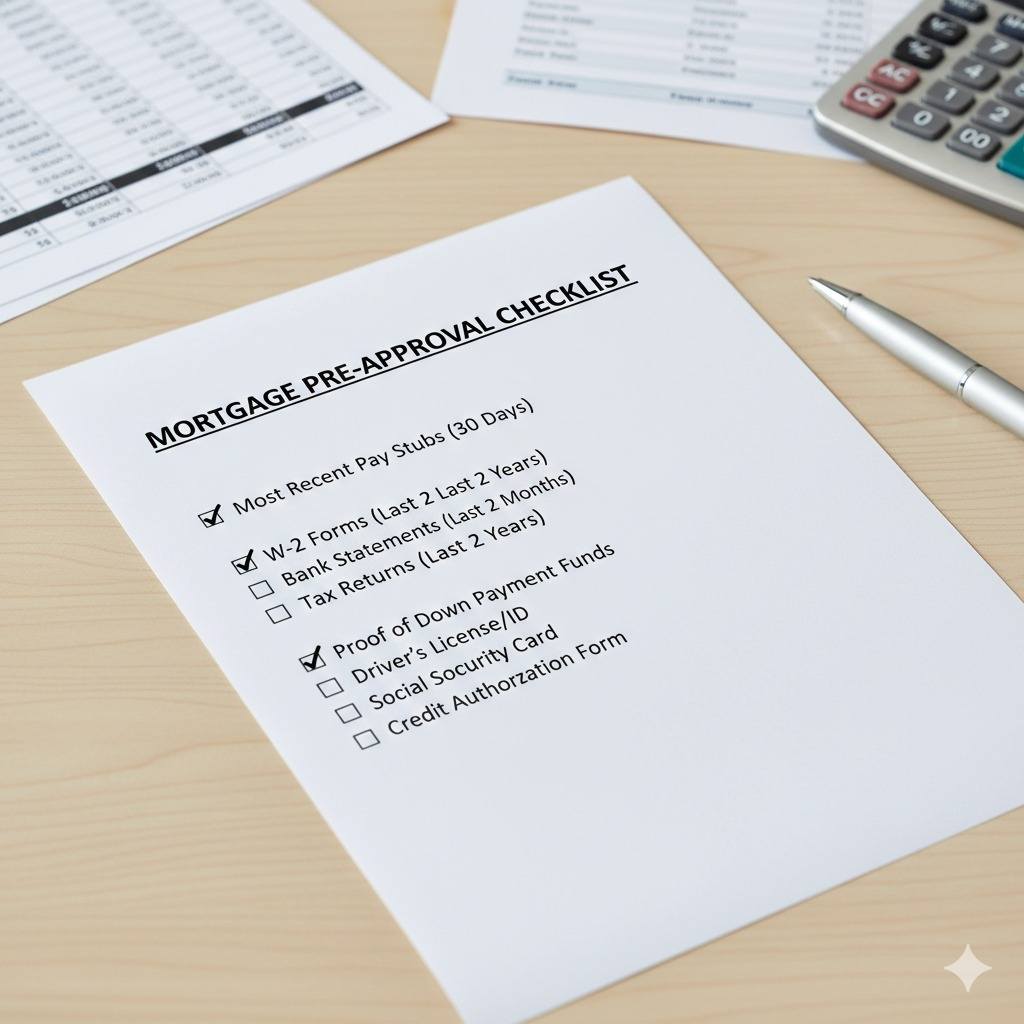

What You Need to Get Pre-Approved

When you sit down with a professional to discuss your mortgage application, you might ask, “What will I need to get a mortgage?” Generally, you will need to provide proof of income (such as W-2s and tax returns) and evidence of assets for a down payment. Knowing specifically what you need for pre-approval saves time and stops the underwriting process from stalling.

Once you have gathered your documents, the next question is timing. When should I apply for the mortgage loan paperwork? Ideally, this should happen before you even set foot in an open house. When should a lender pre-approve my mortgage loan? Most experts recommend getting your letter 3 to 6 months before you intend to buy. This gives you time to fix any credit issues that might arise during the steps to buying a house. When should you get a mortgage pre-approval? As soon as you are serious about entering the market.

Understanding Home Loan Interest Rates and Programs

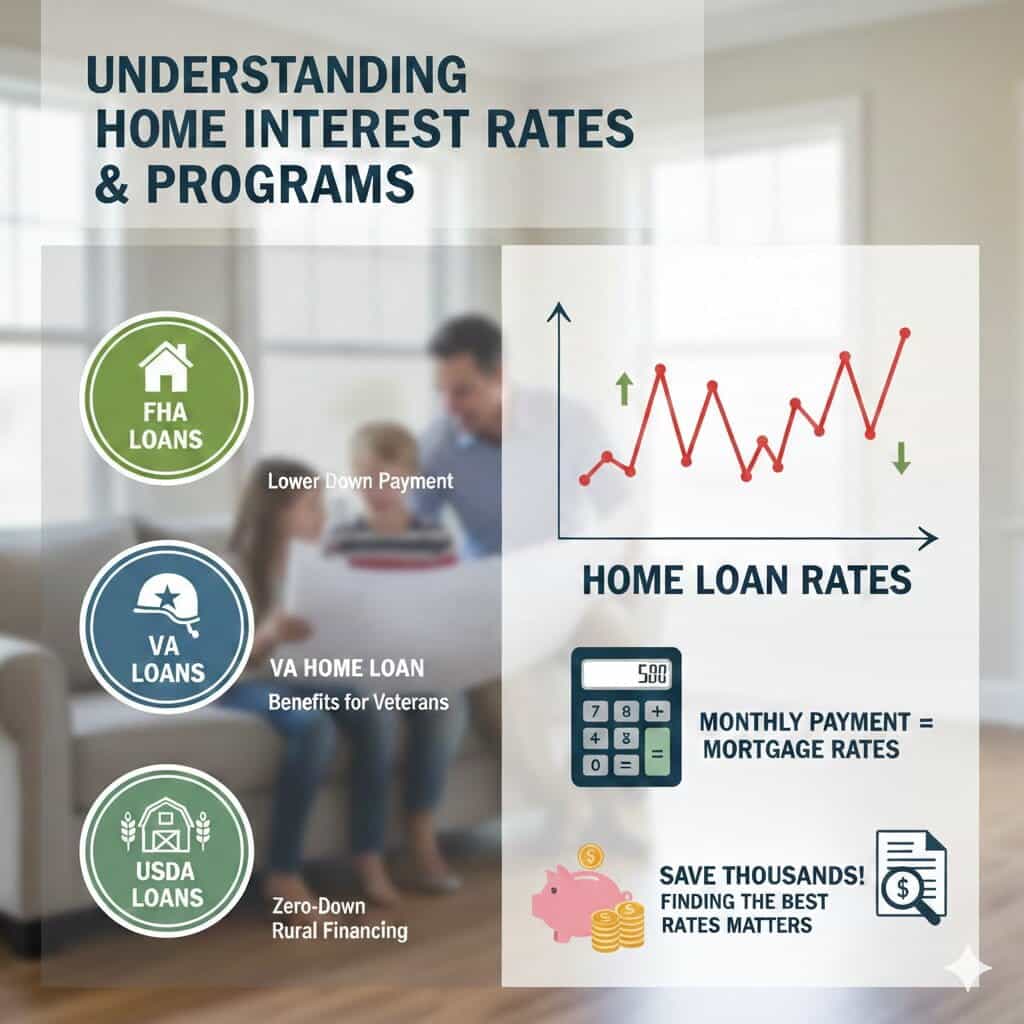

Your choice depends on your financial situation and specific program requirements. For many, FHA loans are an excellent entry point because they offer lower down payment options. Veterans should always look into a VA home loan, which provides significant benefits for those who have served. In more rural Utah communities, USDA loans are another powerful tool for zero-down financing.

Regardless of the program, current mortgage rates and home loan interest rates dictate your monthly payment. It pays to be diligent; finding the best mortgage or home loan rates can save you thousands of dollars over the lifetime of your loan. Keep a close eye on home loan rates, as they fluctuate with market conditions.

Finalizing Your Mortgage Pre-Approval in Utah

It is important to understand the difference between securing a home loan approval and obtaining a prequalification for a home. A pre-qualification is a surface-level look at your debt, while a pre-approval is a deep dive into your credit score. Most sellers in Utah will not even look at an offer without a formal pre-approval letter. As you finalize your plans, continue to monitor current mortgage rates and stay in close contact with your lender. Following these steps will position you to secure your dream home. Whether comparing lenders or quotes, preparation is the key to success.

Utah homeowners have seen incredible appreciation in property values over the last few years. For seniors aged 62 and older living in the Beehive State, your home is likely your largest financial asset. But having wealth tied up in home equity doesn’t always help with daily living expenses or retirement goals. This is where the best reverse mortgage products come into play. A reverse mortgage, specifically a Home Equity Conversion Mortgage (HECM), allows older homeowners to convert part of their home equity into cash without having to sell the home or take on new monthly mortgage payments. If you are looking to supplement retirement income, cover medical costs, or fund home repairs, understanding this financial tool is essential. This guide will walk you through how to get a reverse mortgage in Utah, define eligibility requirements, and help you identify reputable reverse mortgage lenders.

What Is a Reverse Mortgage and How Does It Work?

Before diving into applications, many Utah seniors ask: Where can I get a reverse mortgage, and how does it actually work?

Unlike a traditional “forward” mortgage where you make monthly payments to a lender to build equity, a reverse mortgage works in reverse. The lender pays you. You can receive these funds as a lump sum, fixed monthly payments, a line of credit, or a combination of these options.

Crucially, you are not required to make monthly principal and interest payments for as long as you live in the home as your primary residence. The loan is typically repaid when the last surviving borrower passes away, sells the home, or moves out permanently.

While most people use these loans to tap existing equity, some current HECM holders find that rising Utah property values allow them to refinance reverse mortgage obligations they already have to access additional funds.

How to Qualify for a Reverse Mortgage: Eligibility for Utah Seniors

The most common question we receive is simple: Can I get a reverse mortgage?

To qualify for reverse mortgage products that are insured by the FHA (which most are), you must meet specific criteria set by the Department of Housing and Urban Development (HUD).

Here are the basic requirements to determine exactly how to qualify for a reverse mortgage:

Age Requirement: The youngest borrower on the title must be at least 62 years old.

Property Type: Your home must be your primary residence. This usually includes single-family homes, specific condos, and some manufactured homes that meet FHA standards.

Equity Position: You must have significant equity in your home—typically at least 50%—or own the home outright.

Financial Assessment: While there are no credit score minimums in the traditional sense, lenders must verify that you have the financial capacity to continue paying property taxes, homeowners insurance, and HOA fees (if applicable).

How to Apply for a Reverse Mortgage: A Step-by-Step Application Guide

Once you determine eligibility, the next step is understanding the mechanics of how to apply for a reverse mortgage. It is a more involved process than a standard home loan due to federal consumer protections.

If you are ready to apply for a reverse mortgage, anticipate these steps:

Step 1: HUD-Approved Counseling Before a reverse mortgage application can even be processed, federal law requires you to attend a counseling session with an independent, HUD-approved agency. This ensures you fully understand the obligations and alternatives.

Step 2: Choosing Providers You will need to select reverse mortgage providers to work with (more on that below) and submit your formal application.

Step 3: Appraisal and Underwriting The lender will order an FHA appraisal to determine the current market value of your Utah home. An underwriter will review your financial information to ensure you meet HUD guidelines to get a reverse mortgage.

Step 4: Closing Once approved, you will sign closing documents. If it is a refinance or a new HECM on an existing home, there is a mandatory three-day right of rescission period before funds are disbursed.

Understanding Reverse Mortgage Interest Rates

Like any loan, the cost of borrowing money matters. Finding the best reverse mortgage rates can significantly impact how much equity you retain over time.

Reverse mortgage interest rates can be fixed or adjustable.

Fixed rates are usually only available if you take the lump-sum payout option at closing.

Adjustable rates are typically chosen by borrowers who want a line of credit or monthly payments.

Because these loans involve compounding interest that is added to the loan balance over time, securing the best reverse mortgage rates for seniors is crucial for long-term estate planning.

Finding Reputable Reverse Mortgage Lenders in Utah

Knowing how can I get a reverse mortgage is half the battle; knowing who to get it from is the other half.

When looking for where to get a reverse mortgage, you generally have three categories of professionals to choose from:

Traditional banks.

Non-bank mortgage lenders specializing in HECMs.

Reverse mortgage brokers, who shop multiple lenders on your behalf.

Trying to find the top rated reverse mortgage company or the best bank for reverse mortgage products requires due diligence. You want to ensure you are dealing with reputable reverse mortgage lenders who are NRMLA (National Reverse Mortgage Lenders Association) members and adhere to strict ethical codes.

Don’t just settle for the first offer. We recommend comparing fees and service levels from several best reverse mortgage lenders active in the Utah market.

Is a Utah Reverse Mortgage Your Best Path Forward?

Tapping into your home equity is a major financial milestone, and for many Utah retirees, it’s the key to staying in the neighborhood they love while enjoying a comfortable retirement. However, the best reverse mortgage for one person might not be the right fit for another.

If you’re ready to see how the numbers look for your specific home, the next step is to compare reverse mortgage interest rates and get a professional reverse mortgage quote. By doing your homework and choosing reputable reverse mortgage lenders, you can ensure your home continues to take care of you for years to come.

Shopping for current mortgage rates can feel like trying to hit a moving target, especially when national headlines, local Utah market conditions, and lender pricing all shift week to week. The truth is that “the rate” you see online is rarely the rate you actually qualify for. Your credit score, down payment, loan type, and even the property itself can change pricing. That’s why the smartest way to shop is to compare apples-to-apples loan scenarios and collect multiple mortgage interest rate quotes before making a decision.

Borrowers often start with aggregator sites like bankrate mortgage rates to see national averages, but Utah buyers and homeowners get the best results when they combine that research with personalized quotes from local lenders. Whether you’re buying your first home, looking at a VA loan, or considering a refinance, this guide explains how to interpret home loan rates of different banks, what’s driving federal reserve mortgage rates influences, and how to choose a strategy that fits your goals.

Mortgage Rates Today: 30-Year Fixed and 30 Year Mortgage Rates

For many Utah households, mortgage rates today: 30-year fixed are the default starting point because the payment stays predictable for decades. 30 year mortgage rates are typically higher than 15-year rates, but the monthly payment is lower, which can be helpful if you’re prioritizing cash flow or qualifying for a specific home price.

When comparing 30-year offers, don’t just look at the interest rate. Ask lenders for the full loan estimate, including points, lender fees, and required escrows. A “low” rate with expensive points can cost more than a slightly higher rate with lower fees. This is where using a mortgage interest calculator can save you from guessing: plug in the interest rate, fees, and loan amount to estimate both monthly payment and total interest paid.

Tip for Utah buyers: if you’re competing in a hot market, ask about locking options early. A lock won’t guarantee the best long-term deal, but it can protect you from short-term volatility while you’re under contract.

Refinance Mortgage Rates Today and Cash Out Refinance Rates

Homeowners watching refinance mortgage rates today usually fall into two groups: (1) those trying to lower their payment or rate, and (2) those trying to access equity. If you’re tapping equity, you’ll be comparing cash out refinance rates with second-lien products like home equity loans.

A rate-and-term refinance replaces your current mortgage with a new one designed to reduce the interest rate, shorten the term, or switch loan types. A cash-out refinance does the same, but you borrow more than you owe and receive the difference as cash, often used for renovations, debt consolidation, or major expenses.

Since cash-out loans have different risk pricing, cash out refinance rates can be higher than standard refinance pricing. Your best move is to request multiple mortgage interest rate quotes for both structures and compare them side-by-side using a mortgage interest calculator. You’re not just shopping for the lowest rate, you’re shopping for the best overall outcome.

Rocket Mortgage VA Loan Rates, Jumbo Loan Rates, and Investment Property Mortgage Rates

Not all loans are priced the same. Borrowers eligible for VA financing often look up rocket mortgage va loan rates as a reference point, but you should still compare local lenders, credit unions, and brokers for the best terms. VA loans can be extremely competitive because they typically don’t require mortgage insurance and can offer attractive pricing depending on lender overlays.

For higher-balance properties, jumbo loan rates can differ from conforming loans. Jumbo underwriting often requires stronger credit, higher reserves, and stricter debt-to-income guidelines. In exchange, some borrowers may find jumbo pricing surprisingly competitive, especially with strong borrower profiles.

If you’re buying a rental, investment property mortgage rates are usually higher than owner-occupied rates because lenders treat them as higher risk. If you’re comparing options for a rental, don’t forget to model realistic cash flow. A slightly higher rate might still be worth it if the property’s rental income and appreciation potential are strong.

Mortgage Companies With Lowest Interest Rates and Mortgage Lenders With Lowest Rates

Many people search for mortgage companies with lowest interest rates, mortgage lenders with lowest rates, or mortgage companies with best interest rates, but those phrases can be misleading without context. The “lowest rate” is often tied to a perfect borrower profile (high credit score, large down payment, low DTI, primary residence, and sometimes paying points). That doesn’t mean those rates aren’t real; it means you need to compare rates based on your actual scenario.

A practical way to compare lenders is to gather quotes from:

A local Utah lender or broker (often competitive on service and speed)

A bank or credit union (sometimes strong on fees)

A large online lender (often strong on convenience)

Then compare the effective cost, not just the headline rate. If you’re trying to find mortgage companies with lowest interest rates, ask each lender to quote the same loan amount, down payment, occupancy type, and lock length. That’s the fastest way to figure out who actually offers mortgage companies with best interest rates for you.

Private Mortgage Insurance Rates, Mortgage Insurance Rate Finder, and Mortgage Pre Approval Interest Rate

If you put down less than 20% on a conventional loan, you’ll likely pay private mortgage insurance rates (PMI). PMI is not one-size-fits-all. It’s driven by your credit score and loan-to-value ratio, and it can move your effective monthly cost more than a small rate difference.

Before you lock anything in, request your mortgage pre approval interest rate so you know what you can realistically afford and what pricing tier you’re in. Many buyers skip this step and fall in love with a payment they can’t replicate once the real numbers come in.

To estimate PMI, you can use a mortgage insurance rate finder (or ask lenders to show you the PMI line item in the quote). In many cases, improving your credit score or increasing your down payment slightly can reduce PMI enough to materially change your monthly payment.

Best Interest Only Mortgages, Accelerated Mortgage Payment, and Home Equity Loan Rates

Some borrowers explore best interest only mortgages to keep payments lower during an initial period. These can be useful in specific situations, like uneven income, short-term liquidity needs, or strategic investing, but they require discipline. Once the interest-only period ends, payments can rise significantly because you start paying principal too.

On the flip side, if your goal is to pay off debt faster, an accelerated mortgage payment strategy can reduce interest and shorten your timeline. Biweekly payments or adding extra principal each month can make a noticeable difference over time, especially if you start early.

If you’re not trying to replace your first mortgage, compare home equity loan rates to refinancing. A home equity loan may let you keep your original rate while borrowing against equity separately. The best choice depends on your current rate, how much you need to borrow, and how long you plan to keep the home.

Federal Reserve Mortgage Rates and Mortgage Rates Will Go Down

A common question is whether mortgage rates will go down. While it’s impossible to predict perfectly, mortgage pricing often reacts to inflation expectations, bond markets, and signals from the Federal Reserve. People sometimes refer to federal reserve mortgage rates, but the Fed doesn’t set mortgage rates directly. Instead, its policy moves influence borrowing costs across the economy, which can flow through to mortgage pricing.

The smartest approach is to avoid trying to “time the bottom.” If the monthly payment works for your budget and the loan supports your financial goals, it can still be a good move, even if rates shift later. If rates drop meaningfully, you can evaluate refinancing at that point.

Current Mortgage Rates and 40-Year Mortgage Refinance Options

If you’re returning to the market again, remember that current mortgage rates change not only by day, but by borrower profile and loan type. And for homeowners who need payment relief, some lenders offer long-term options such as a 40-year mortgage refinance. This can reduce monthly payments by extending the loan length, though you’ll typically pay more interest over the life of the loan.

Before you choose a 40-year option, compare it against alternatives like a standard refinance, a home equity loan, or changing your payment strategy. The “best” loan isn’t always the one with the smallest monthly payment, it’s the one that matches your timeline and keeps your long-term costs reasonable.

The Utah housing market is shifting, and in 2026, the traditional path to homeownership is being rewritten. For many residents, securing a Mortgage no longer means walking into a bank with a simple W-2. As the “Silicon Slopes” continue to foster a culture of independence, more buyers are entering the market as self-employed professionals, a 1099 contractors, or a Gig-worker.

While these roles offer freedom, they often complicate the Pre-approval process. Understanding the specific Eligibility requirements for non-traditional Income is the first step toward moving from a rental to a home you own.

Utah Mortgage Strategies for the Self-Employed and 1099 Earners

For a Self-employed individual, the biggest hurdle is often proving a stable Income when tax write-offs reduce your “on-paper” earnings. In 2026, lenders have become more flexible, offering Bank Statement loans that look at actual deposits rather than net tax figures. This is a game-changer for the Gig-worker who may have multiple revenue streams.

When applying, having a CPA-prepared P&L (Profit and Loss statement) can significantly boost your Credit profile’s credibility. Whether you are looking for a Conventional loan or a government-backed FHA product, documenting your financial health accurately ensures you don’t hit unexpected Limits during underwriting.

First-Time Buyer Grants and Downpayment Assistance

If you are a First-time buyer in Utah, you have access to some of the most aggressive financial Assistance in the nation. The state continues to offer significant Grants and Subsidies designed to bridge the gap between savings and rising home prices.

Currently, a popular Utah program provides up to $20,000 for a Downpayment, which can be applied to newly built Construction. For those with a military background, VA loans remain the gold standard, often requiring $0 down. Similarly, buyers looking at rural or suburban growth boundaries may find that USDA loans offer zero-down Eligibility for those who meet specific household Income benchmarks.

Investor Opportunities and DSCR Loan Limits

The 2026 market isn’t just for primary residents; it’s a prime environment for the savvy Investor. If you are looking to acquire a rental property but want to avoid the strict debt-to-income ratios of a Conforming loan, a DSCR (Debt Service Coverage Ratio) loan is the ideal tool.

DSCR loans qualify the property based on its own potential rental Income rather than your personal salary. This allows investors to bypass traditional Mortgage hurdles, making it easier to build a portfolio of Utah real estate. Even if you are a Veteran investor or a professional with a complex 1099 tax history, these asset-based loans provide a streamlined path to closing.

Refinance and Market Outlook

As we move through the year, many homeowners are keeping a close eye on the market to refinance existing high-interest debt. Whether you are looking to lower your monthly payment on a Conventional loan or tap into equity for home improvements, understanding the current Utah rate environment is essential. From the specialized needs of the Self-employed to the broad Assistance available for a First-time buyer, the 2026 housing landscape is built on flexibility. By mastering your Credit and choosing the right loan product—be it FHA, VA, or DSCR—homeownership in the Beehive State is more attainable than ever.

The Utah housing market has experienced significant movement in recent years. If you’ve been watching mortgage rate trends in Utah state, you’re likely wondering what 2026 could bring — and whether now is the right time to act to lock at the best mortgage rate.

Whether you’re looking into how mortgage interest rates are determined, reviewing mortgage rates today, tracking mortgage rates daily and mortgage rate trends in Utah overall, or trying to determine the best time to lock mortgage rate, understanding both the bigger picture and the practical implications can help you make smarter financial decisions.

How Mortgage Interest Rates Are Determined

Before evaluating mortgage rates forecast 2026, it’s important to understand how mortgage interest rates are determined.

Mortgage rates are largely driven by national economic forces rather than local state policy. Key factors include inflation trends, Federal Reserve decisions, and movements in the 10-year U.S. Treasury yield. When inflation rises, investors demand higher returns, which pushes current mortgage interest rates and current housing interest rates higher. When inflation stabilizes, rates often ease.

This relationship explains why housing interest rates today and interest rates today 30 year fixed can move even if Utah’s local housing demand stays strong. For broader context, see Fannie Mae Economic Forecast, which outlines how economic conditions influence long-term projections.

Understanding these forces makes it easier to interpret overall mortgage rate trends and changes reflected in a mortgage rates today chart.

Current Mortgage Rates Utah and National Comparisons

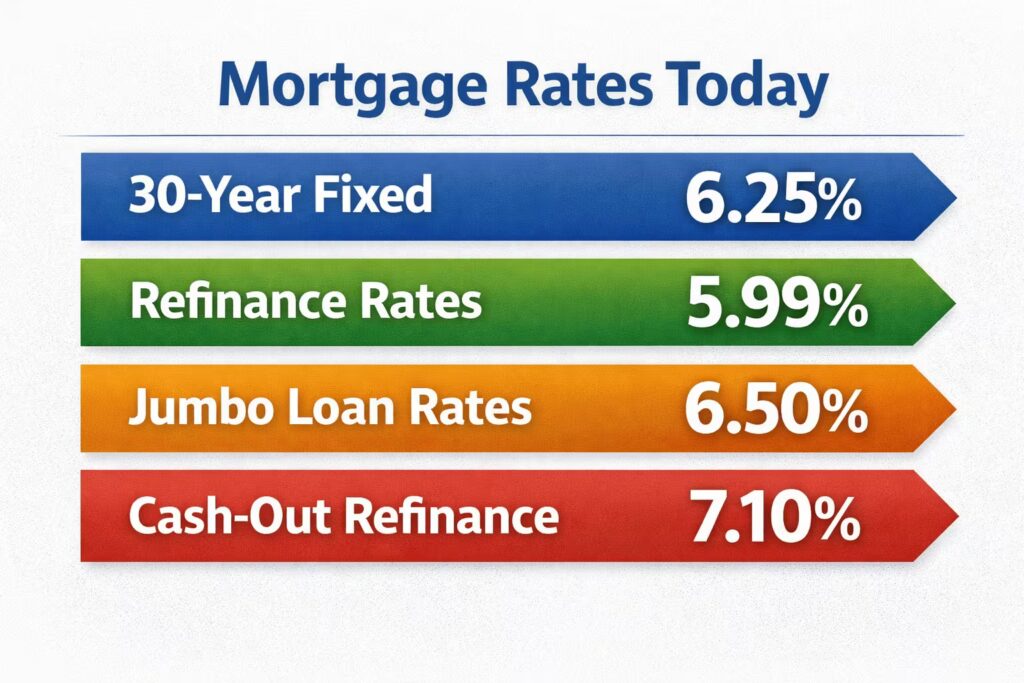

So what do rates look like right now? According to Freddie Mac Primary Mortgage Market Survey (PMMS), recent 30 year mortgage rates today have generally ranged in the mid-6% range, depending on weekly market conditions.

Here in Utah, current mortgage rates Utah typically mirror national averages, though your personal rate depends on credit score, loan type, and down payment. For example:

Usually, mortgage rates today 30 year fixed usually provide lower monthly payments but higher long-term interest costs.

Mortgage rates today 15 year fixed tend to offer lower interest rates but higher monthly payments.

For eligible military borrowers, current VA mortgage rates may be more competitive.

Even a small difference in current mortgage rates 30 year fixed can significantly affect total loan cost over 30 years. Comparing current mortgage rates and interest rates today 30 year fixed across lenders can help you find meaningful savings.

Mortgage Rates Forecast 2026: When Will Mortgage Rates Drop Again?

A common question right now is: when will mortgage rates drop again?

Most industry analysts suggest that mortgage rates forecast 2026 may show gradual stabilization or modest easing if inflation continues cooling. However, this does not necessarily mean a sharp drop. Instead, borrowers should expect moderate fluctuations influenced by economic data releases.

If you’re comparing refinance mortgage rates today 30 year fixed or reviewing mortgage rates today refinance options, it’s helpful to watch inflation reports and Federal Reserve announcements, since these events often trigger short-term movement.

For Utah-specific market expectations, review Utah Mortgage Rates 2025 Outlook, which provides regional context that may influence timing decisions.

How Mortgage Rate Trends Affect Monthly Payment

Understanding how mortgage rates affect monthly payment is critical before making a decision.

For example, a 0.25% increase in current housing interest rates can add thousands of dollars in total interest over the life of a 30-year loan. Even modest changes in current mortgage rates 30 year fixed can meaningfully alter monthly affordability.

Many buyers ask, what credit score gets best mortgage rates? Generally, higher credit scores qualify for lower mortgage interest rates today, which reduces both monthly payments and overall borrowing costs.

Tracking a mortgage rates today chart can help you visualize whether rates are trending upward or downward before committing.

Best Time to Lock Mortgage Rate in 2026

Choosing the best time to lock mortgage rate requires balancing risk and certainty.

If mortgage rate trends in Utah are rising steadily, locking your rate protects you from additional increases before closing. On the other hand, if rates are trending downward and your lender offers flexibility, you might wait. However, there is a possibility that markets could reverse unexpectedly.

When monitoring mortgage rate trends in Utah, look for daily updates alongside key economic indicators. Such examples are inflation reports and Federal Reserve policy decisions, which can provide valuable insight into short-term direction.

If you’re evaluating home refinance rates today or comparing refinance mortgage rates today 30 year fixed, locking at the right time can lower your long-term cost significantly. The goal isn’t to perfectly “time the bottom,” but to secure a rate that aligns with your comfort level.

Conclusion on Mortgage Rate Trends in Utah

For Utah buyers and homeowners, 2026 may offer a more predictable environment compared to recent volatility. While mortgage rate trends suggest gradual stabilization, financial preparation remains essential.

Whether you’re reviewing mortgage rates today, current mortgage rates, current mortgage rates 30 year fixed, interest rates today 30 year fixed, mortgage rates today 15 year fixed, current VA mortgage rates, or exploring mortgage rates today refinance options, informed timing and lender comparison can make a meaningful difference.

By understanding how mortgage interest rates are determined, monitoring mortgage rates forecast 2026, and locking the mortgage rate strategically, Utah borrowers can move forward with greater confidence.

If you’ve been watching Utah mortgage rates in 2026, you know the market moves fast. Whether you’re searching for the best mortgage lenders in Utah or exploring Salt Lake City home loans, the right information is your greatest advantage. It also helps you make sense of Utah real estate trends before you commit. This guide covers everything from locking in a low rate to navigating first-time buyer programs.

Utah Home Loans: Rates and What You Need to Know

Finding the best current mortgage rates in Utahstarts with comparing your options across multiple Utah mortgage brokers. Rates vary significantly depending on your loan type, credit score, and down payment, so shopping around is essential.

Here’s what to know about loan types currently available in Utah:

Utah conventional loans are best for buyers with strong credit and at least 5–20% down.

Utah jumbo loans are designed for higher-priced properties that exceed conforming loan limits.

Utah fixed-rate mortgages lock in your rate for the life of the loan, ideal if you want payment stability.

Utah adjustable-rate mortgages (ARMs) typically offer a lower starting rate, but adjust over time.

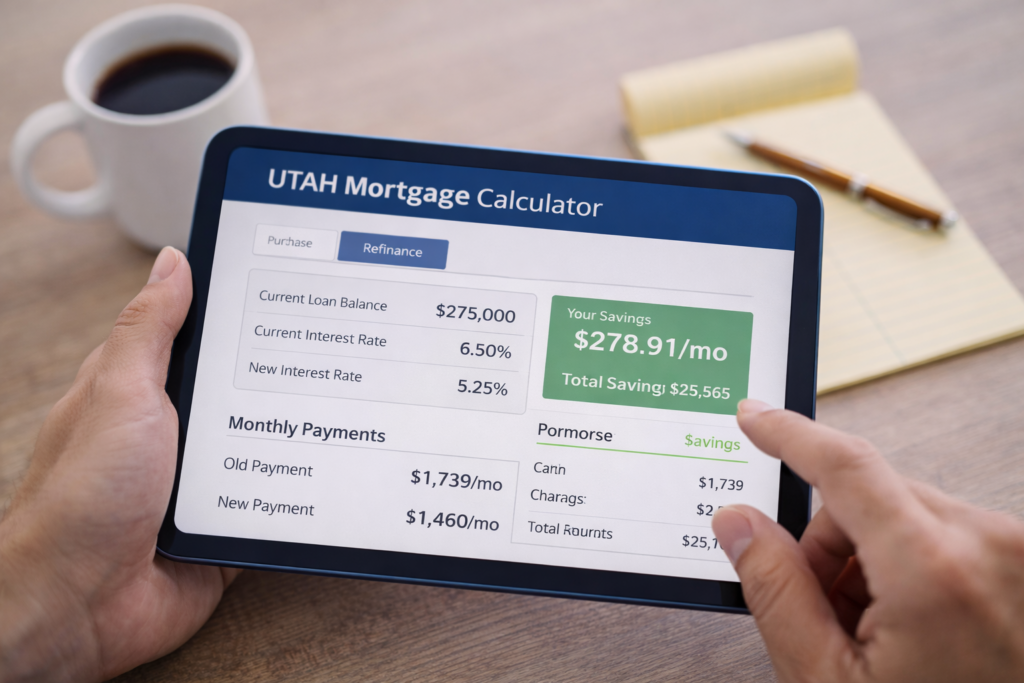

Use a Utah mortgage calculator to model your monthly payment before committing to a loan type. Don’t overlook Utah mortgage closing costs either. They typically range from 2–5% of the loan amount and can affect whether a new loan makes financial sense.

First-Time Home Buyer Utah: Programs and Grants

Many first-time buyers in Utah are surprised to learn they don’t need a 20% down payment. For a first-time home buyer in Utah, several programs can significantly reduce your upfront costs. Utah housing grants through the Utah Housing Corporation (UHC) offer down payment and closing cost assistance. Utah FHA loans require as little as 3.5% down and come with more flexible credit requirements. If you put less than 20% down, lenders will typically require Utah mortgage insurance (PMI). You can remove it once you build sufficient equity.

Understanding Utah mortgage requirements before you apply will put you in a much stronger position. These include debt-to-income ratios, minimum credit scores, and income limits for certain programs. Whether you’re looking at Provo home loans, St. George mortgage rates, or properties along the Wasatch Front, there’s a program designed to help.

Refinancing in Utah for Long-Term Wealth

If you already own a home, refinancing in Utah could be one of the most impactful financial moves you make in 2026. The key is to weigh your potential monthly savings against your Utah mortgage closing costs to determine your break-even point. Many homeowners refinance to switch from a high-rate ARM to a stable Utah fixed-rate mortgage. Others pursue a Utah mortgage refinance simply to lower their monthly payment. Refinancing is also a smart way to access home equity for renovations or education, or to shorten your loan term and build wealth faster.

With rates shifting throughout the year, keeping an eye on Utah mortgage news and acting when rates dip can save tens of thousands of dollars over the life of your loan.

Explore first-time home buyer mortgage Utah options, including mortgage rates Utah, FHA loan requirements Utah, Utah down payment assistance programs, and how to get pre-approved today.

First Time Home Buyer Mortgage Utah Guide (2026)

Buying your first home can feel overwhelming, but understanding the first-time home buyer mortgage process in Utah makes it far more manageable. From comparing mortgage rates in Utah to reviewing FHA loan requirements in Utah and local assistance programs, today’s buyers have more tools than ever to make smart financial decisions.

Many buyers begin by checking mortgage rates today and researching mortgage rate forecast trends. While timing matters, preparation matters more. Understanding affordability, loan programs, and credit requirements will position you for success whether rates rise or fall. Using a mortgage calculator in Utah can help estimate payments early and determine a comfortable budget.

first-time-home-buyer-utah.jpg

Mortgage Rates Utah and 30 Year Mortgage Rates Utah Today

Tracking mortgage rates in Utah is one of the most important steps for any buyer. Many borrowers monitor mortgage rates today, especially 30 year mortgage rates Utah, since the 30-year loan remains the most common option.

When reviewing mortgage rates forecast projections, remember that markets change quickly. Many buyers ask, are mortgage rates expected to drop in Utah or should they move forward now? Rather than waiting indefinitely, evaluate affordability and payment stability.

Using a mortgage calculator with extra payments can show how making additional principal payments reduces total interest. Buyers also frequently compare mortgage rate lock vs float strategies. If rates appear volatile, locking may protect your budget. If trends suggest improvement, floating may offer savings.

First Time Home Buyer Programs Utah and Utah Down Payment Assistance Programs

Saving for a down payment is often the biggest obstacle. Fortunately, several first-time home buyer programs in Utah and Utah down payment assistance programs exist to support new buyers.

These programs may include:

Down payment grants

Closing cost assistance

Reduced mortgage insurance

Education incentives

Many first-time home buyers search for Utah mortgage rates for first-time home buyers to find programs with competitive interest rates. Pairing assistance with favorable rates can dramatically improve affordability.

If savings or credit are limited, FHA loan requirements Utah often provide flexible qualification options. FHA programs allow lower down payments and can be paired with Utah down payment assistance programs for additional support.

home-buyer-programs-utah.jpg

FHA Loan Requirements Utah and Minimum Credit Score for Mortgage Utah

Understanding of loan requirements Utah is essential for buyers with moderate credit or limited savings. FHA financing is popular because it allows more flexible guidelines than many conventional loans.

Buyers frequently ask about the minimum credit score for the mortgage Utah standards. While requirements vary by lender, improving your credit score, reducing debt, and maintaining stable employment strengthen approval chances.

Veterans should also review VA loan eligibility Utah. VA loans often provide competitive interest rates and reduced down payment requirements for qualified borrowers.

If credit challenges exist, consider searching for mortgage lenders for bad credit or a mortgage broker near me for bad credit to identify specialized lending options. Many mortgage lenders with the best rates also offer consultation on improving approval strength before applying.

How Much House Can I Afford in Utah?

Before shopping for homes, calculate affordability. Many buyers search for ” how much house can I afford Utah to determine realistic price ranges.

Helpful tools include:

mortgage calculator Utah

mortgage calculator with extra payments

debt-to-income analysis

tax and insurance estimates

Using these tools helps align expectations with financial comfort. Just because you qualify for a certain amount does not mean you should spend the maximum. Responsible borrowing ensures long-term stability.

Mortgage Pre Approval Utah First Time Buyer

Getting mortgage pre approval the first time buyer, documentation completed early provides a strong advantage. Sellers take pre-approved buyers more seriously, and you will understand your exact price range.

The pre-approval process typically includes:

Credit evaluation

Income verification

Asset review

Employment confirmation

Many buyers search for ” mortgage broker near me reviews or mortgage broker near me first time home buyer to find trusted local professionals. Comparing mortgage lenders near me ensures competitive pricing and service. Some buyers also compare mortgage lenders for bad credit if credit improvement is needed before closing.

Choosing Between Mortgage Lenders Near Brokers and Me

Working with experienced professionals can simplify the process. Searching for mortgage lenders near me or mortgage lenders with the best rates allows you to compare options and find competitive financing.

Mortgage brokers often provide access to multiple lenders, which may help buyers with unique credit or income situations. Whether working with a broker or a direct lender, transparency and communication are key.

When Should I Lock My Mortgage Rate?

Many buyers wonder:

When should I lock my mortgage rate

Are mortgage rates expected to drop utah

mortgage rate lock vs float

Locking a rate protects against increases, while floating may benefit buyers if rates decline. Your decision should depend on market trends, risk tolerance, and closing timeline rather than speculation alone.

Final Thoughts on First-Time Home Buyer Mortgage Utah

Navigating the first-time home buyer mortgage process in Utah requires preparation and knowledge. By understanding mortgage rates Utah, 30 year mortgage rates Utah today, and available first-time home buyer programs Utah, buyers can move forward with confidence.

Review FHA loan requirements Utah, explore Utah down payment assistance programs, and calculate affordability using a mortgage calculator Utah. Then begin the mortgage pre approval Utah first time buyer process with trusted mortgage lenders near me.

With the right preparation and strategy, purchasing your first home in Utah can be both achievable and financially smart.

Thinking about buying a home in Utah? It’s a huge step, and the journey can feel like a maze, especially when it comes to finding the right financing. But what if you could cut through the confusion and get straight to the facts? What if you could confidently find a loan that not only fits your budget but also feels like a win? This guide is your roadmap, written by local Utah experts who know this market inside and out. We’ll show you exactly how to find the best mortgage rates Utah has to offer, turning a complicated process into a simple, step-by-step plan.

Fixed vs. Adjustable: Which is Right for Your Utah Home?

When you start your search, the first question you’ll face is about the type of loan you want. It’s like choosing between a sure thing and a calculated gamble. The 30 year fixed mortgage rates Utah offers are the go-to for a reason: they provide total peace of mind. Your interest rate and monthly payment will stay exactly the same for three decades, offering unmatched stability. For many, this is the smart choice, providing a predictable budget you can count on. However, if you’re a strategic thinker who plans to pay off your home faster or sell in a few years, a 15 year fixed mortgage rates Utah loan could be your best friend. While your monthly payments will be a bit higher, you’ll build equity faster and save a shocking amount of money on interest over the life of the loan. It’s an aggressive move that can pay off big.

What Are Current Mortgage Rates Today?

The mortgage market is a living, breathing thing, and what it looks like today can change tomorrow. You’re not just looking for a number; you’re looking for a snapshot in time. The current mortgage rates today are influenced by everything from global economics to local trends. Staying informed is half the battle. This is why it’s so vital to focus on the current mortgage rates Utah is seeing, as our unique economy can sometimes buck national trends. Digging deeper, you can find the current 30 year mortgage rates in Utah and start to see what’s realistically available. Location matters, too. For example, the mortgage rates Salt Lake City lenders offer might be slightly different than those in smaller, rural counties. That’s why working with a local professional who knows the ins and outs of the Utah market can give you a significant edge.

Your Personalized Path to the Best Mortgage Rates

Once you’ve got a handle on the types of loans, it’s time to get personal. Your individual financial picture is the single biggest factor in determining your rate. Lenders want to know you’re a safe bet, and they judge that with your credit score. That’s why many people immediately look up the current mortgage rates by credit score to get a realistic idea of where they stand. It’s a smart move. Never, ever settle for the first quote you get. The single most powerful thing you can do to save money is to compare mortgage rates Utah lenders are offering. Shopping around and getting quotes from at least three different sources can save you tens of thousands of dollars over the life of your loan. It may seem like a hassle, but think of it as a few hours of work that pays off for years to come.

Unlock Your Potential with the Right Tools

The good news? You don’t have to do all this math in your head. A top-notch mortgage calculator Utah can instantly do the heavy lifting for you. Simply input the loan amount, rate, and term, and you’ll know your estimated monthly payment in seconds. This lets you play with different scenarios to find the perfect fit for your budget.

And what about the future? While nobody has a crystal ball, keeping an eye on the mortgage rate forecast Utah can provide valuable context. Expert predictions based on market data can give you the confidence to move forward, rather than waiting and wondering what might happen next.

Finding the “Lowest” of the Low

Now for the best part: the hunt for the absolute best deal. Your goal isn’t just to find the average mortgage rates Utah is seeing—it’s to find the lowest mortgage rates. This is where a little extra effort can lead to a big payoff. Look beyond the big banks and find lenders who specialize in finding you the best deal. Your search for the lowest mortgage rates Utah has to offer is what separates a good deal from a great one.

Think of it this way: the best mortgage rates aren’t just handed out. You have to seek them out. By starting your search for the lowest mortgage rates near me and asking about the lowest mortgage rates available, you are taking control of the process.

For those who are ready to make a move right now, searching for best mortgage rates now and lowest mortgage rates today can lead you to lenders who are ready to offer competitive, time-sensitive deals. Don’t let a golden opportunity pass you by. Every point and every fraction of a point matters. By following this guide, you can confidently and strategically navigate the Utah housing market and secure a loan that sets you up for financial success.

Ready to Find Your Perfect Loan?

Finding your ideal mortgage can be confusing, but our team of local Utah experts is here to help you every step of the way. We’re passionate about helping our community achieve their dreams of homeownership. Contact us today for a personalized rate quote and to get all of your mortgage questions answered. Your future home is closer than you think!

Thinking of buying a home in 2025? Partnering with a trusted mortgage broker is key to navigating an evolving housing market. With mortgage rates in 2025 projected to shift due to economic trends and Federal Reserve decisions, expert guidance can help you lock in the best deal. Whether you’re searching for a “mortgage broker near me” in Salt Lake City or exploring options online, knowing how to choose the right professional can save you thousands and serious stress.

A mortgage broker acts as your guide through the maze of lenders and loan options. Instead of approaching banks one by one, a broker shops around on your behalf to secure competitive rates and terms. They can help you navigate mortgage broker vs lender decisions, explaining the pros and cons of each route. Especially in competitive markets like Utah, using a mortgage broker near me or a mortgage broker in Salt Lake City can simplify your search for the perfect loan. Many brokers offer free initial consultations, so it costs you nothing to explore your options.

A big question for homebuyers is mortgage broker vs lender. While a direct lender processes loans in-house, a mortgage broker shops around for you, seeking deals from multiple lenders. This can be especially helpful when trying to lock in the best mortgage lenders in Salt Lake City or find the best mortgage lenders near me with lower fees or faster approvals. Remember to read mortgage broker near me reviews for insights into service quality.

Start by searching online for a mortgage broker near me, or check out review sites. Pay special attention to the mortgage broker near me reviews page to see real experiences from past clients. This is crucial if you’re dealing with unique financial situations, like trying to get a mortgage with bad credit or a low credit score mortgage.

If you’re unsure where to begin, type best mortgage lenders near me into Google or browse forums like best mortgage lenders reddit, where real users share recommendations. These resources can help you identify the best mortgage lenders in Salt Lake City or the best mortgage lenders in Utah, depending on where you live.

Not all brokers have the same expertise. Some specialize in first-time homebuyer loans, while others are experts in FHA mortgage rates or jumbo loans. If you’re worried about your credit score, ask whether the broker has experience securing loans for clients with mortgage broker near me bad credit. They’ll know which lenders are more flexible and how to improve your approval odds.

One major benefit of working with a broker is access to competitive rates. With who has the best mortgage rates right now being a constant question in 2025, brokers can show you live offers from multiple lenders. They may also provide access to helpful tools like a mortgage calculator Utah, a mortgage calculator USA, or a mortgage calculator with extra payments. These calculators help you see how different loan scenarios affect your monthly payment and total interest paid over time.

Once you’ve identified a few potential brokers, schedule interviews and ask pointed questions:

What lenders do you work with most often?

How do you get compensated? (Some brokers are paid by lenders, while others charge borrowers directly.)

Do you specialize in FHA mortgage rates or other specific products?

Can you help if I’m trying to get a mortgage with student loans or other complex financial situations?

What’s the average timeline from application to closing?

If a broker refuses to disclose fees or pushes you into one lender without explaining why, that’s a red flag. The best professionals will help you compare options, including rates from the best mortgage lenders and strategies for securing low-credit-score mortgage approvals.

Finding a trustworthy mortgage broker is one of the smartest decisions you can make on your path to homeownership. In 2025, with rates and rules changing quickly, having an expert by your side can make all the difference. Whether you’re exploring mortgage rates utah, calculating payments with a mortgage calculator with extra payments, or searching for the best mortgage lenders near me, investing time in choosing the right broker will help you save money—and sleep better at night.

So start your search for a mortgage broker near me, read the mortgage broker near me reviews, and ask questions. Your future home—and your financial security—are worth it.