Introduction

Navigating the real estate market in the Beehive State can be daunting, but understanding how to get a mortgage is the first real step toward homeownership. Many prospective home buyers start their journey by exploring the financial landscape of home loans —the real competitive edge comes from securing a mortgage pre-approval. This document proves to sellers that a mortgage lender has already vetted your finances and is ready to back your offer.

To start the process, you should research the best mortgage companies and best mortgage lenders available in the state of Utah. Experts encourage you to get a mortgage quote from several different sources to ensure you get the best deal. While some buyers prefer large national banks, others have found that working with a local mortgage broker offers help with the local markets and a more personalized experience.

What You Need to Get Pre-Approved

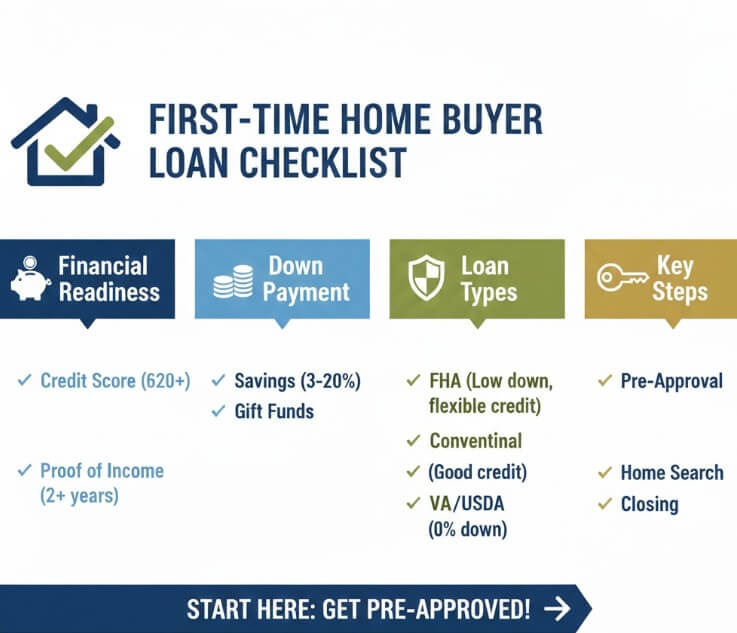

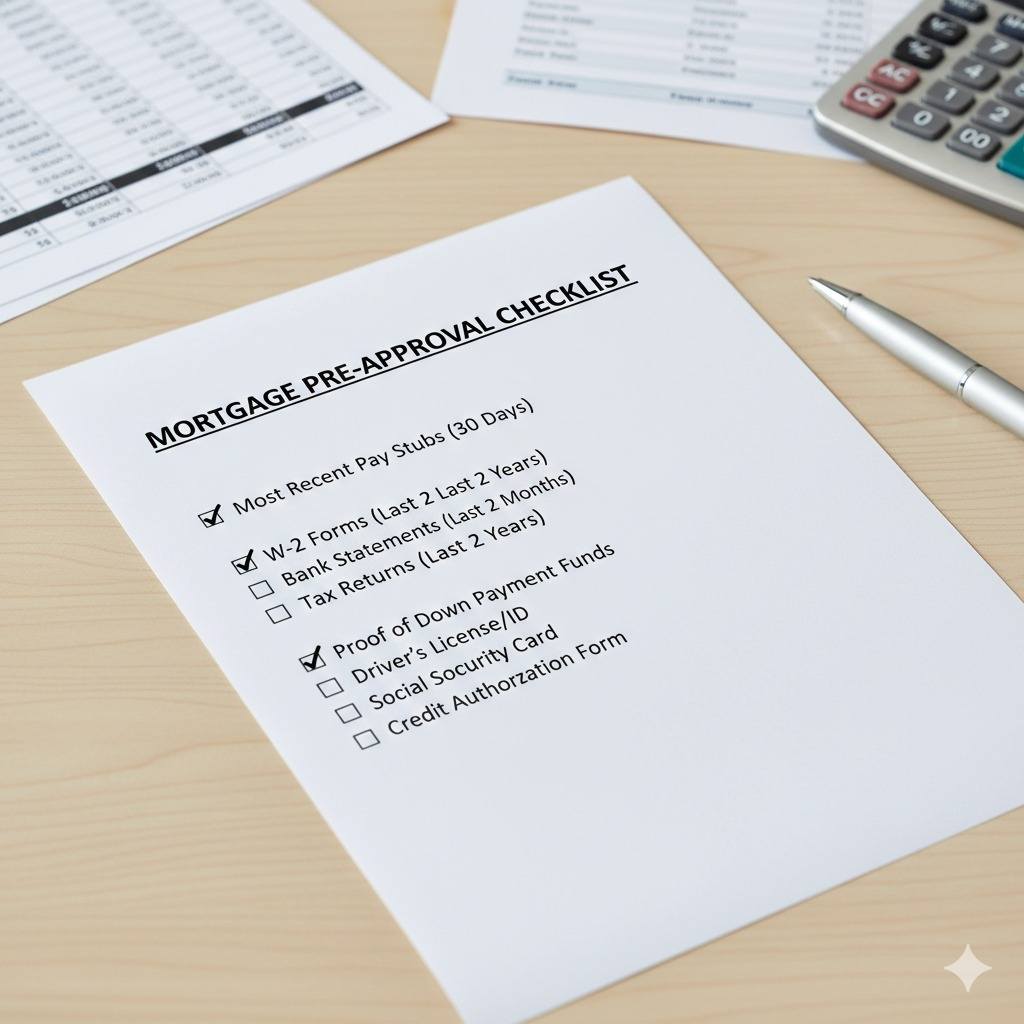

When you sit down with a professional to discuss your mortgage application, you might ask, “What will I need to get a mortgage?” Generally, you will need to provide proof of income (such as W-2s and tax returns) and evidence of assets for a down payment. Knowing specifically what you need for pre-approval saves time and stops the underwriting process from stalling.

Once you have gathered your documents, the next question is timing. When should I apply for the mortgage loan paperwork? Ideally, this should happen before you even set foot in an open house. When should a lender pre-approve my mortgage loan? Most experts recommend getting your letter 3 to 6 months before you intend to buy. This gives you time to fix any credit issues that might arise during the steps to buying a house. When should you get a mortgage pre-approval? As soon as you are serious about entering the market.

Understanding Home Loan Interest Rates and Programs

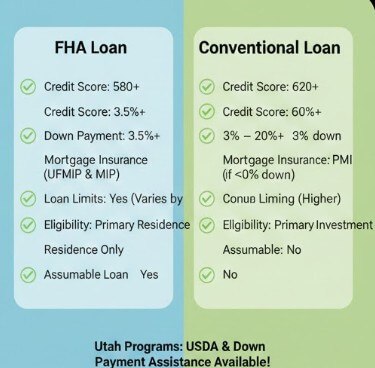

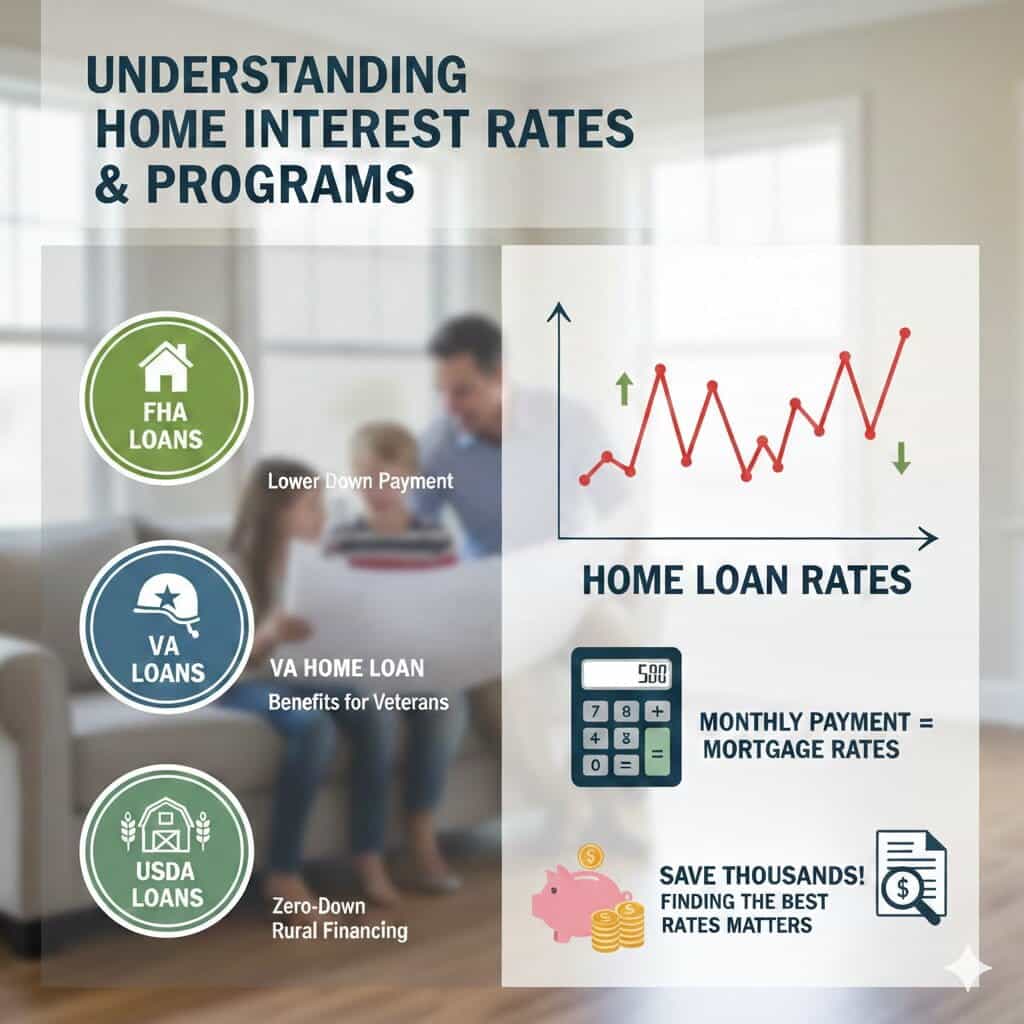

Your choice depends on your financial situation and specific program requirements. For many, FHA loans are an excellent entry point because they offer lower down payment options. Veterans should always look into a VA home loan, which provides significant benefits for those who have served. In more rural Utah communities, USDA loans are another powerful tool for zero-down financing.

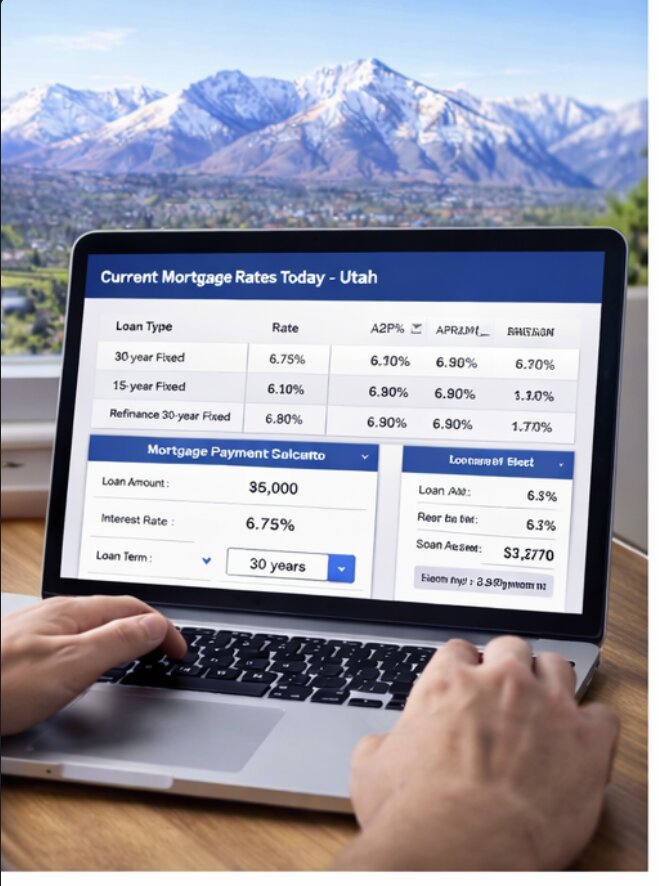

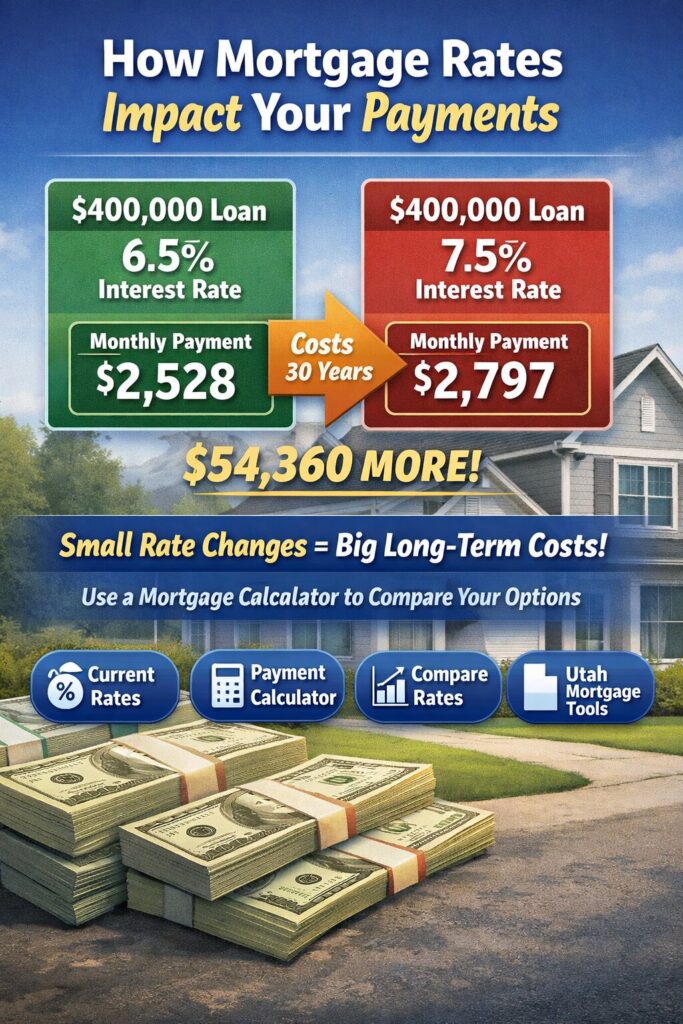

Regardless of the program, current mortgage rates and home loan interest rates dictate your monthly payment. It pays to be diligent; finding the best mortgage or home loan rates can save you thousands of dollars over the lifetime of your loan. Keep a close eye on home loan rates, as they fluctuate with market conditions.

Finalizing Your Mortgage Pre-Approval in Utah

It is important to understand the difference between securing a home loan approval and obtaining a prequalification for a home. A pre-qualification is a surface-level look at your debt, while a pre-approval is a deep dive into your credit score. Most sellers in Utah will not even look at an offer without a formal pre-approval letter. As you finalize your plans, continue to monitor current mortgage rates and stay in close contact with your lender. Following these steps will position you to secure your dream home. Whether comparing lenders or quotes, preparation is the key to success.