Why Utah Mortgage Rates Today Matter More Than Ever.

In today’s competitive housing market, understanding Utah mortgage interest rates for first-time home buyers is essential for making informed decisions and securing favorable loan terms.. Whether you’re a seasoned homeowner or a first-time buyer, staying current with Utah mortgage interest rates today empowers you to lock in favorable financing terms.

Mortgage rates fluctuate based on a range of economic factors, including inflation trends, Federal Reserve policy, and lender risk assessments. While national averages provide a benchmark, Utah mortgage interest rates can vary significantly across lenders. Comparing current mortgage rates, 30-year fixed and mortgage rates today, FHA at the local level helps ensure that you secure a rate tailored to your needs.

Utah Mortgage Interest Rates Trends and 2025 Forecasts

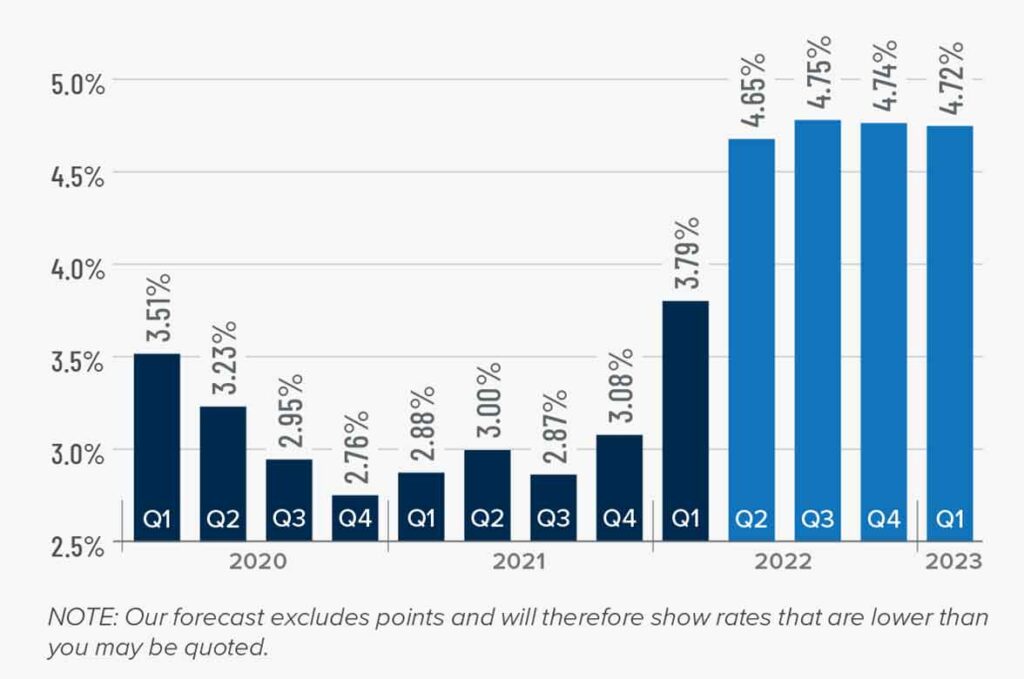

As mortgage professionals, we are often asked: What are the projections for Utah home loan rates forecast for 2025? Based on market analysis, we anticipate relative rate stability in 2025, following the fluctuations seen throughout 2024. Prospective buyers and homeowners should closely monitor Utah mortgage interest rate trends this week via trusted sources like Freddie Mac’s PMMS and Utah-based lenders such as City Creek Mortgage. Utilizing tools like a Utah mortgage refinance calculator allows you to forecast payment scenarios and assess refinancing potential as market conditions evolve.

The Best Mortgage Lenders in Utah 2025: FHA, VA, and Jumbo Loans.

Navigating mortgage products can be complex, but understanding the nuances of each option is key. When researching the best mortgage lenders in Utah 2025, consider how your financial goals align with the following programs:

Utah FHA loan limits for 2025 have increased, allowing greater access for buyers using FHA-backed financing.

VA mortgage rates in Utah today remain a strong option for qualifying veterans, often featuring lower interest rates and no down payment.

Jumbo mortgage Utah requirements continue to evolve, with lenders requiring higher credit scores and thorough income documentation.

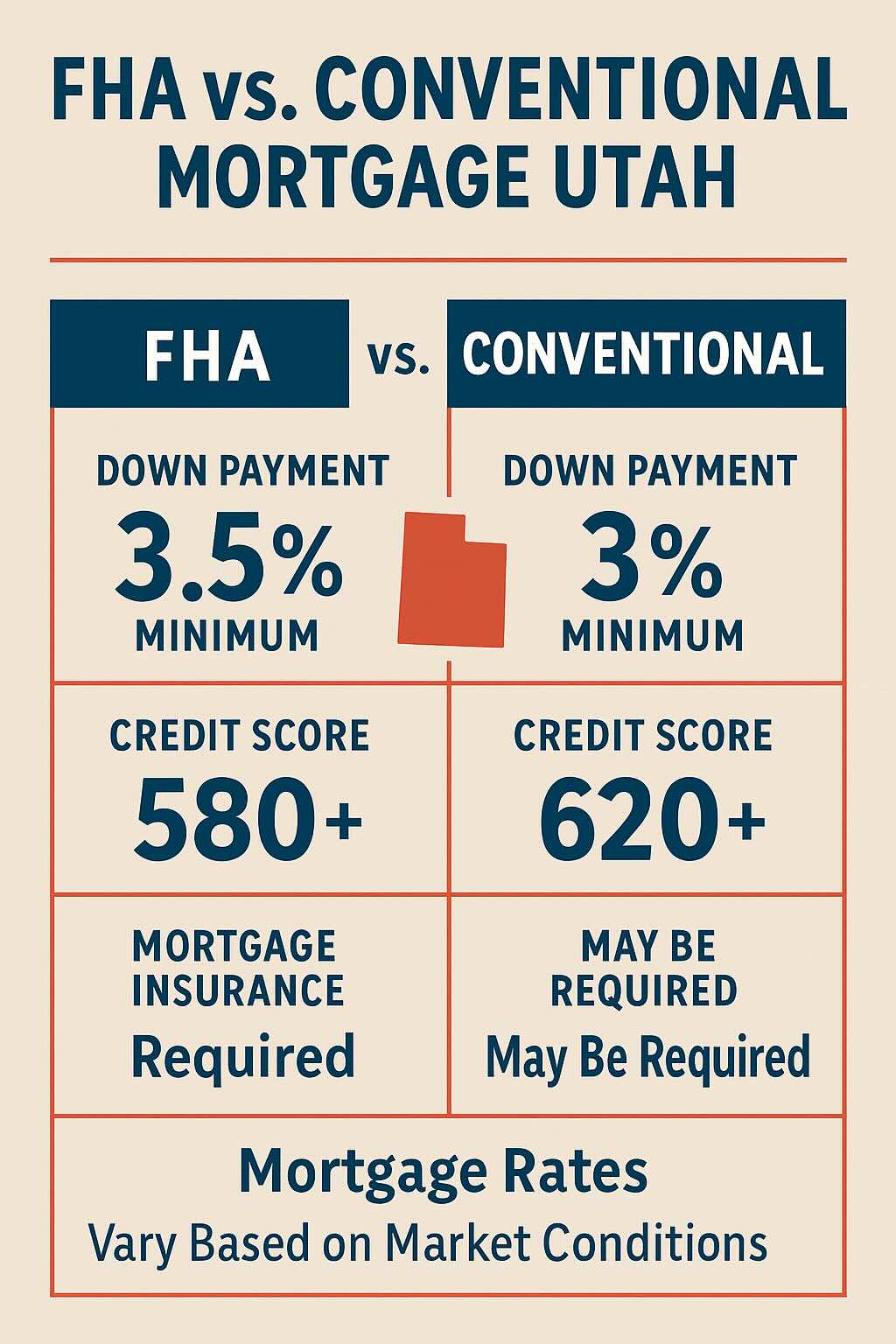

Those weighing FHA vs conventional mortgage Utah options should factor in long-term cost savings and qualification thresholds. For those with limited funds, programs offering Utah FHA down payment assistance provide critical support toward homeownership.

Getting Approved and Refinancing at Today’s Utah Mortgage Interest Rates

Knowing how to get approved for a mortgage in Utah includes maintaining a healthy credit profile, managing debt-to-income ratios, and collecting financial documentation early.

Homeowners evaluating mortgage rates refinance options should assess both cash out refinance Utah rates and traditional term refinancing. Not sure if it’s the right time? A Utah mortgage refinance calculator and platforms like FHA.com help clarify when to refinance mortgage Utah based on both market rates and your financial objectives.

Utah Mortgage Tools: Use These Calculators Before You Buy Before starting the home search, utilize tools that help shape your financial expectations.

A mortgage payment calculator Utah estimates your monthly obligation, while a home affordability calculator Utah factors in income, debt, and projected interest rates.

These resources are especially valuable if you’re exploring home equity loan interest rates or considering a move into Utah’s housing market for the first time.

FAQ – Utah Mortgage Interest Rates

Q: What are the current Utah mortgage rates for first-time buyers? A: Rates vary based on credit score, loan type, and market conditions. First-time buyers may qualify for competitive FHA and VA rates.

Q: Are Utah mortgage rates expected to drop in 2025? A: Based on current forecasts, experts anticipate a stable or slightly declining trend in interest rates through mid-2025.

Want to understand current mortgage rates in Utah today? This guide helps you compare, calculate, and lock in the best deal using real numbers and tools updated for 2025. Looking to buy or refinance in Utah? Explore the current mortgage rates today, compare top lenders, use our Utah mortgage calculator, and larn how to lock in the best rates for 2025. Many homebuyers are surprised by how much they can save by checking the current Utah home loan ratestoday rather than relying on national averages.

Current Mortgage interest rates in Utah Today: How to Compare, Calculate, and Lock in the Best Deal

Current rates for Utah mortgages Today: What to Expect

If you’re refinancing or buying your first home, understanding the Home financing options in Utah can help you lock in a better deal for your long-term goals. Mortgage pricing today can vary depending on your loan type, credit score, and lender. As of this week, 30-year fixed mortgage Utah rates average around 6.5%, while 15- year mortgage rates Utah sit closer to 5.9%. These rates can fluctuate daily, which is why many homebuyers are choosing to lock Home loan rates in Utah while they’re favorable. If you’re refinancing, refinance rates in Utah today follow a similar pattern, offering lower rates for shorter terms. Tools like a Utah refinance calc

Using a Utah Mortgage Calculator for Smarter Planning

Before applying, use a Utah mortgage calculator to estimate monthly payments. These tools allow you to plug in your loan amount, interest rate, and term length to forecast affordability. Many include options to estimate Utah home equity loan rates, taxes, and insurance—giving you a more realistic picture. Refinancing? Be sure to use a Utah cash-out refinance calculator if you’re looking toleverage your home equity for major purchases.

Compare Mortgage Rates From Utah Banks and Lenders

Choosing the best mortgage companies in Utah can make a huge difference in your loan experience. Some of the top-rated Utah mortgage lenders include City Creek Mortgage, Academy Mortgage, and Intercap Lending. Always compare mortgage rates from Utah banks, credit unions, and online brokers. Look for no closing cost mortgage Utah options, lowest down payment Utah mortgage offers, and pre-approval terms from Utah mortgage pre approval providers.

Exploring Loan Options – FHA, VA, Jumbo & More

Different loans mean different rates. Here’s a quick breakdown: Utah FHA loan rate today is often lower than conventional rates and great for first-time buyers with minimal down payments. VA loan rates Utah are exclusive to veterans and active-duty military, often with 0% down. Utah jumbo mortgage rates are needed for homes priced above county loan limits—expect slightly higher rates. Utah HELOC rates and Utah home equity loan rates let you tap into your home equity for renovations, debt payoff, or investments.

The Forecast – Utah Mortgage Rate Trends 2025

Wondering what’s next? According to experts, Utah mortgage rate predictions 2025 show potential stabilization, with Utah mortgage rate trends 2025 indicating a slow drop as inflation cools and demand evens out. Stay informed with a Utah mortgage rate chart from reliable financial sources to track monthly rate changes.

Final Tips – Locking the Best Mortgage Rate in Utah

Here’s how to snag the best current Loan interest rates in Utah: Apply for Utah mortgage pre approval to show you’re a serious buyer; monitor Utah mortgage rate forecast updates weekly; consider shorter loan terms for better rates (i.e., 15-year); ask about no closing cost mortgage Utah options to save upfront; and review and lock mortgage rate Utah when it dips.

Conclusion: Take Action With the Right Tools & Info

From using a Utah mortgage calculator to comparing Utah mortgage lenders, the tools are in your hands. Whether you’re buying your first home or refinancing with Utah cash out refinance rates, now is the time to make smart moves. Keep an eye on the Utah mortgage rate chart and remember to lock in rates when they align with your financial goals.

Frequently Asked Questions About Utah Mortgage interest rates

Should I lock in my mortgage rate now?

With rates still fluctuating, many Utah buyers are choosing to lock in their mortgage rate if they find one that fits their budget. Locking prevents you from being affected by rising rates between approval and closing.

What’s the difference between fixed and adjustable rates?

A fixed-rate mortgage means your interest rate stays the same throughout your loan term. An adjustable-rate mortgage (ARM) starts lower but may change after a few years based on market conditions.

Can I refinance if I just bought a home last year?

Yes! If rates have dropped or your credit has improved, refinancing—even within a year—can help you lower monthly payments or pull out equity through a cash-out refinance.

How to Use Our Utah Mortgage Calculator

Just plug in your loan amount, interest rate, and term length. You can also estimate property taxes, insurance, and even HOA fees for a more accurate view. Want to test a cash-out refi scenario? Adjust the loan amount to include equity withdrawal. The calculator updates instantly!

Still comparing options? Be sure to bookmark this page and check back weekly—we update our Utah mortgage rate trends every Friday to help you stay ahead in 2025.

If you’re exploring homeownership in the Beehive State, a Utah housing loan might be your best path forward. Whether you’re a first time home buyer in Utah, a low-income family, a self-employed professional, or even a single parent, Utah offers a wide range of mortgage programs tailored to your needs. These programs—often backed by the Utah Housing Corporation—can help make buying a home more affordable with flexible credit requirements, down payment assistance, and low-interest financing options.

FHA Home Loan in Utah: A Flexible Option for New Buyers

The FHA home loan in Utah is one of the most popular loan options for new buyers, particularly those with moderate or low credit scores. FHA loans are backed by the federal government and offer a down payment as low as 3.5%. These loans also pair well with Utah housing loan programs, which may include grants or second mortgages to assist with upfront costs.

If you’re not sure whether an FHA loan is your best fit, consider using a home loan comparison in Utah to explore other choices. For many, the FHA option stands out thanks to its low barrier to entry and compatibility with Utah mortgage assistance offerings.

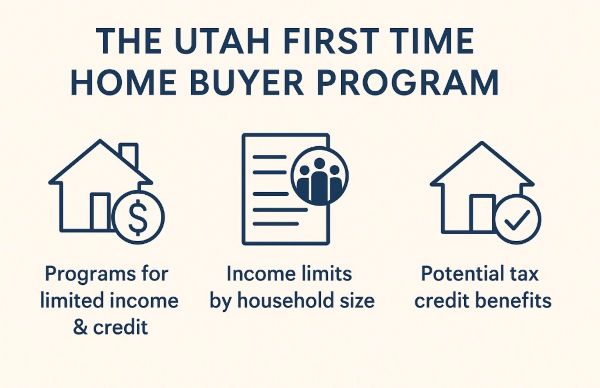

The Utah First Time Home Buyer Program: What You Should Know

The Utah first time home buyer program offers significant support for those purchasing their first home. Through the Utah Housing Corporation, eligible buyers can access programs like FirstHome, HomeAgain, Score, and NoMI—all designed to support individuals with limited income or credit history.

These programs often come with Utah housing first time buyer income limits, which are set based on household size and location. If you qualify, you may also be eligible for the first time home buyer tax credit in Utah, giving you additional savings after your purchase.

Don’t forget to check whether your home qualifies for a USDA home loan in Utah—an option for buyers in rural areas—or if you’re a veteran, a VA home loan in Utah might offer zero down and no mortgage insurance. Check out Tools to Beat Today’s Mortgage Rates

Utah Mortgage Preapproval Checklist: Preparing for Success

Before you apply for a mortgage, use a Utah mortgage preapproval checklist to get organized. Preapproval increases your credibility with sellers and gives you a clearer idea of your budget.

Here’s what you’ll likely need:

Two years of tax returns and W-2s

Recent pay stubs or income proof

Asset documentation and bank statements

Photo ID and Social Security number

For buyers in unique situations, such as applying for a mortgage for self employed in Utah, you’ll need to provide business income verification, including profit-and-loss statements and 1099 forms. Similarly, a mortgage for single parents in Utah may involve proof of child support or government assistance.

Collecting the documents needed for a mortgage application in Utah can feel overwhelming, but preparation makes the process smoother. Beyond financial records, lenders may also ask for rental history, gift letters (if applicable), and proof of homeowner’s insurance. These documents are crucial, especially when you’re applying for low income mortgage programs in Utah or using down payment assistance Utah funding.

Low Down Payment Mortgage Options in Utah

If saving for a down payment is holding you back, you’re not alone. Thankfully, low down payment mortgage Utah options can get you into a home with minimal upfront cost. These programs—often available through the Utah housing loan system—include grants or secondary loans that cover both the down payment and part of the closing costs.

Working with one of the best lenders for first time buyers in Utah ensures you receive guidance on these options and helps you navigate the eligibility criteria effectively.

How to Apply for a Home Loan in Utah

Understanding how to apply for a home loan in Utah is simpler when broken down step-by-step:

Gather financial documents and get preapproved

Choose a lender or mortgage broker in Salt Lake City

Explore Utah housing loan programs

Compare offers using a home loan comparison Utah tool

Submit your full application and schedule a home inspection

The best mortgage companies in Utah will walk you through each of these steps and ensure you receive all applicable Utah mortgage assistance.

Refinance and Beyond: Getting the Best Rates in Utah

Already a homeowner? You may still benefit from the best refinance rates Utah. Refinancing your existing mortgage—especially if you originally used a Utah housing loan—can lower your monthly payments or reduce your interest rate. Be sure to ask your lender if you qualify for a streamlined refinance under FHA or VA guidelines.

Choosing the Right Lender or Mortgage Broker in Salt Lake City

Partnering with a mortgage broker in Salt Lake City can help you compare multiple loan options at once, especially if you’re not sure whether to go with a conventional, FHA, VA, or USDA home loan in Utah. Brokers often have access to exclusive rates and can assist with unique needs like self-employment income or single-parent households.

Buying a home in Utah? Understanding current mortgage rates in Utah—which are currently higher than the national average—and navigating the real estate market can save you thousands. With home prices rising and interest rates fluctuating, it’s crucial to be well-prepared. This guide will walk you through expert home buying tips, from getting pre-approved to securing the best financing options, so you can purchase your dream home confidently.

Why Utah is a Great Place to Buy a Home

Utah has become one of the most attractive states for homebuyers primarily because of its booming economy and job growth. With a growing tech sector, known as the “Silicon Slopes,” and a strong business environment, Utah offers excellent employment opportunities, making it an ideal place to settle down. In addition to economic stability, Utah is famous for its stunning landscapes and outdoor recreation. From world-class skiing in Park City to world renown hiking trails and national parks, Utah has it all. These lifestyle perks make homeownership even more desirable. Another major advantage is affordability in Utah and Utah remains more cost-effective than neighboring states like California and Colorado, allowing buyers to get more value for their money while still enjoying a high quality of life.

7 Home Buying Tips to Get the Best Deal

Buying a home is one of the biggest financial decisions you’ll make, and getting the best deal requires careful planning. From understanding current mortgage rates in Utah to navigating a competitive housing market, being prepared can save you thousands of dollars. The key to a successful home purchase is securing favorable financing, knowing what loan options are available, and strategically negotiating your offer. Whether you’re a first-time buyer or a seasoned investor, these seven expert home-buying tips will help you find the right home at the best possible price. By following these steps, you’ll be able to make informed decisions, avoid common pitfalls, and ensure a smooth home-buying process. Let’s dive in!

1. Check Current Mortgage Rates in Utah

Before starting your home search, it’s crucial to research current mortgage rates in Utah. Mortgage rates directly impact your monthly payment and the overall cost of your home, so staying informed can save you thousands over the life of your loan. Compare fixed vs. adjustable-rate mortgages to see which best suits your financial goals. Keep an eye on historical trends to understand whether rates are rising or falling, and consider locking in a rate when market conditions are favorable. Working with a lender early in the process can help you secure a competitive mortgage rate that aligns with your budget.

2. Get Pre-Approved Before You Shop

A mortgage pre-approval is one of the most important steps in the home-buying process. It signals to sellers that you are a serious buyer and can afford the home you are bidding on. During pre-approval, lenders evaluate your credit score, income, and debt-to-income ratio to determine your borrowing capacity. The stronger your credit profile, the better mortgage rates you can qualify for, potentially saving you thousands over the life of your loan. Getting pre-approved before house hunting also helps you set a realistic budget and avoid falling in love with homes outside your price range. you set a realistic budget and avoid falling in love with homes outside your price range.

3. Understand Your Loan Options

Choosing the right mortgage loan type can significantly impact your affordability and long-term financial stability. Conventional loans are best for buyers with strong credit and stable income, often requiring a 20% down payment. FHA loans are great for first-time buyers, offering lower down payment options and more flexible credit requirements. VA loans (for military service members and veterans) and USDA loans (for rural homebuyers) provide additional financing benefits with low or no down payment requirements. Understanding the pros and cons of each mortgage type will help you select the best financing option for your home purchase.

4. Know Utah’s First-Time Home Buyer Programs

If you’re a first-time homebuyer, Utah’s first-time home buyer programs can help make home ownership more affordable. The Utah Housing Corporation provides loans with low-interest rates and down payment assistance, making it easier to qualify for a mortgage. Additionally, various federal and state grants are available to help cover closing costs and down payments, reducing the upfront financial burden. Researching these programs and working with a knowledgeable lender can help you maximize your home-buying benefits and secure the best possible deal.

5. Choose the Right Location

Location is one of the most critical factors in determining the value of your home. The best place to buy in Utah depends on your lifestyle, budget, and long-term goals. Salt Lake City is a great choice for those seeking urban amenities, job opportunities, and a vibrant city life. Provo is ideal for families and students, with a strong rental market and great schools. If you prefer a warmer climate and scenic beauty, St. George offers a relaxed, nature-filled lifestyle with easy access to national parks. To help narrow your search, check out our in-depth breakdown of the best Utah cities for homebuyers.

6. Be Prepared for a Competitive Market

Utah’s real estate market is highly competitive, with many homes selling quickly and above asking price. To increase your chances of securing a home, be prepared to act fast when you find a property you love. In competitive areas, buyers may need to offer above the asking price to stand out. Additionally, waiving certain contingencies, such as appraisal or home inspection contingencies, can make your offer more attractive to sellers—but be sure to discuss risks with your real estate agent before making these decisions. If you’re entering a bidding war, our guide on winning a bidding war on a home in Utah has expert strategies to help you succeed.

7. Factor in Closing Costs & Extra Fees

Many buyers focus on the down payment but overlook additional expenses such as closing costs, taxes, and fees. Closing costs typically range between 2-5% of the home’s purchase price, covering lender fees, title insurance, and escrow expenses. Additional costs like home inspections, property taxes, and homeowners insurance can add to your budget. Understanding these expenses ahead of time will help you plan financially and avoid last-minute surprises. Before closing on your home, review our complete guide to closing costs in Utah so you know what to expect.

Final Thoughts: Secure the Best Mortgage Rate in Utah

Yes! We understand that buying a home is a very exciting journey, but it can also feel very stressful, especially with fluctuating mortgage rates and the competitive Utah Market. The key to a successful home purchase is staying informed about current mortgage rates in Utah and prepping in advance. Monitoring rates, getting pre-approved, and partnering with a trusted local real estate agent can help position you for success.

Even just a slight reduction in your mortgage rate will lead to significant savings over the life of your loan. Making smart financial decisions early on in the process is vital to securing the right home at the best price and one that aligns with your budget, lifestyle, preferences.

Explore Other Resources: For additional help and guidance on navigating Utah’s real estate market and securing the best mortgage rates, visit our [Home Buying Resources Page]. You can also check trusted sites like [Bankrate] and [Zillow] for the latest Utah mortgage rates and property listings.

Mortgage Myths Debunked:What Every Utah Homebuyer Should Know

Buying a home can feel like a daunting task, especially with some common misconceptions that can make it feel like homeownership is out of reach for so many. Homebuyer education, mortgage calculators and tools, loan, and down payment assistance programs can make homeownership more accessible and affordable than you might think. We will debunk common myths regarding mortgage rates and homeownership in Utah and show how you might access a mortgage that previously seemed out of reach.

Myth: You Need a 20% Down Payment and Perfect Credit to Buy a House in Utah

The belief that you need a perfect credit score and a 20% down payment to buy a home discourages many potential homebuyers. While these can ease the process of buying a home, certain incentives and benefits make it easier to get approval for a loan than you might think.

Utah Down payment Assistance

One myth that keeps many from pursuing homeownership is the idea that you need a 20% down payment to purchase a home. While it’s true that a larger down payment can help you secure a better mortgage rate, it’s far from a requirement. In fact, there are several Utah mortgage assistance programsthat can help you cover your down payment. For first-time homebuyers in Utah, down payment assistance programs and low down payment mortgage options like FHA loans or USDA loans can make buying a home much more affordable. The Utah Housing Corporation down payment assistance program offers down payment assistance specifically for eligible Utah homebuyers. Some Utah communities offer additional down payment assistanceshould you choose to purchase a home there. Using a Utah mortgage calculator, you can quickly see how much you can save on your down payment by exploring different loan options, including low down payment mortgages or even no down payment loans for eligible buyers in rural areas with USDA loan eligibility.

Homebuyer Assistance in Utah with Low Credit

A common myth that discourages many potential buyers is the belief that you need a perfect credit score to secure Utah home loans. While having a strong credit history certainly helps when applying for a mortgage, it’s not a dealbreaker if your score isn’t flawless. Many Utah mortgage brokers and local mortgage companies in Utah offer specialized loan options for those with less-than-perfect credit. FHA loans, for instance, are designed to help buyers with lower credit scores (often as low as 580) secure financing with lower down payments. If you’re worried about your credit score, talk to the best mortgage lenders in Utah about homebuyer resources and options like FHA loans, VA loans or USDA loans. These can be forgiving of lower scores, especially if other financial factors, such as your debt-to-income ratio, are strong.

Myth: Renting is Always Cheaper Than Buying in Terms of Home Affordability

There is a common myth that states that renting is always cheaper than buying. We will discuss and debunk this myth. It is not necessarily true that renting is always cheaper. While renting has lower upfront costs, buying a house can be more cost-effective in the long run. There are many different factors at play to determine which is better for you. Current Utah mortgage rates, tax benefits, access to FHA loans in Utah, and property appreciation can all impact your financial decisions. Depending on the rates when you buy, a mortgage payment could be cheaper than a rent payment.

Utah Homebuyer Grants vs. Costs of Renting

While buying means more upfront costs, there are resources which can combat this. First-time homebuyers can qualify for homebuyer grants which provide sums of money for free to use towards a down payment or closing costs. This can be huge in the long run, because the larger down payment you put down, the lower your monthly mortgage payment is. On the flip side, with renting there can be many extra costs that can increase your monthly rent payment. For example, parking fees, pet ownership fees, and amenities fees; as well as one-time large payments for a security deposit. Additionally, when you pay a monthly mortgage, you are building equity by owning a property and can get money back if you sell the house later on. When you rent, you do not build any equity or get any money back that you have paid. This is because owning a house is an investment. Fixed-rate mortgages mean that payments do not inflate over time, but rent payments generally increase steadily every year. While mortgage rates are currently higher in Utah than they were several years ago, analysts predict them to be lower in the future. This gives you the chance to lock in a house at the current price and refinance at a lower rate down the road. With the right loans, homeowner assistance programs, and a look to the future, now could be a great time to make the switch from being a renter to being a homeowner.

Navigating Utah’sMortgage Myths and Homebuying Realities

Buying a home in Utah can seem overwhelming with all the myths surrounding mortgage rates, down payments, and credit requirements. However, as we’ve explored, you don’t need a perfect credit score or a 20% down payment to become a homeowner. With various federal / Utah down payment assistance programs and flexible loan options, purchasing a home is more accessible than many realize. While renting might seem like the cheaper option upfront, buying a home can often be more cost-effective in the long run, thanks to homebuyer grants, equity building, and stable mortgage payments. To further assist you in navigating Utah’s mortgage landscape, check out the resource Mortgage Rates Made Easy for helpful tools, updated rates, and personalized guidance. Understanding your options, using tools like a Utah mortgage calculator and working with reputable lenders can help you make the best decision for your financial future. Whether you’re looking to buy your first home or exploring ways to invest, debunking these common myths is the first step toward turning homeownership into a reality in Utah.