Current Home Loan Refinance Rates in Utah: What Homeowners Need to Know This Month

If you’re a Utah homeowner wondering whether now is the right time to refinance your mortgage, you’re not alone. Interest in current home loan refinance rates in Utah has surged in recent months as borrowers look to reduce their monthly payments or access home equity. With thousands of people searching for terms like “refinance mortgage rates” and “current refinance mortgage rates,” staying informed about local trends has never been more important.

In this guide, we’ll break down what’s happening with mortgage and refinance rates in Utah, how you can compare options, and what factors affect your ability to lock in a low rate.

Why Are Refinance Rates in Utah Attracting So Much Attention?

According to recent search data, keywords like “current home loan refinance rates” and “refinance mortgage rates today” have seen a 900% year-over-year increase. That means homeowners are actively looking for updated, localized refinance information—especially those in fast-growing housing markets like Salt Lake City, Ogden, and Provo.

There are a few reasons for this surge:

- Falling interest rates in certain loan categories

- Increased home equity from rising property values

- Desire to switch from adjustable to fixed-rate mortgages

- Access to cash through cash-out refinancing

Even a 0.5% change in refinance mortgage rates can lead to thousands of dollars in savings over the life of a loan, making rate shopping a high-stakes activity for families.

Current Refinance Mortgage Rates in Utah

While rates can vary based on your credit profile, lender, and loan type, here’s a general breakdown of refinance interest rates in Utah as of this month:

| Loan Type | Average Refinance Rate |

| 30-Year Fixed | 6.45% |

| 15-Year Fixed | 5.85% |

| 5/1 ARM (Adjustable Rate) | 6.10% |

| FHA Refinance | 6.25% |

| VA Refinance | 6.00% |

Tip: Use an online refinance calculator to estimate your savings based on these average rates and your current mortgage terms.

These averages reflect national and Utah-specific data, but current refinance mortgage rates can vary day to day. That’s why it’s essential to get personalized quotes.

What Impacts Your Refinance Rate?

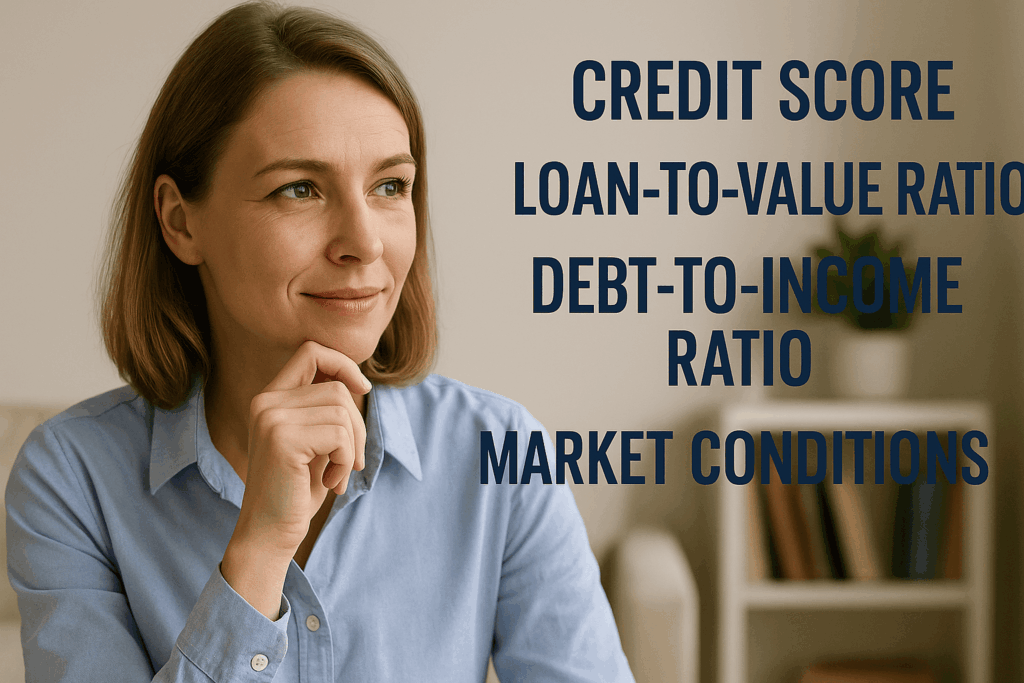

Before locking in a new loan, it’s important to understand what influences your rate. Here are the main factors lenders consider:

- Credit Score: Higher scores (740+) usually unlock the lowest rates.

- Loan-to-Value Ratio (LTV): A lower LTV, meaning more equity in your home, often leads to better rates.

- Debt-to-Income Ratio (DTI): A DTI under 36% is ideal.

- Type of Refinance: Rates for cash-out refinances are typically higher than for rate-and-term refinances.

- Market Conditions: Federal Reserve policy, inflation, and investor demand for mortgage-backed securities all affect national trends.

If you’re trying to decide whether now is a good time to refinance, keep in mind that today’s refinance rates may shift significantly based on upcoming economic news.

When Is the Best Time to Refinance in Utah?

The answer depends on your goals. Here are some common scenarios where refinancing makes sense:

- You want to lower your monthly payment by locking in a lower rate.

- You plan to stay in your home for several years and want to switch from an ARM to a fixed mortgage.

- You need cash for home improvements, college tuition, or debt consolidation.

- You bought your home when rates were over 7% and want to drop to current mortgage refinance rates near 6%.

If any of these apply, it may be worth checking current refinance rates in Utah and getting prequalified.

How to Shop for the Best Refinance Mortgage Rates in Utah

Don’t just go with the first lender you find online. Here’s how to find the most competitive offer:

- Compare at least three quotes from national banks, credit unions, and local Utah lenders.

- Look at both the interest rate and the APR, which includes fees.

- Use a refinance calculator to model your break-even point.

- Ask about discount points and how much it would cost to buy down your rate.

- Make sure the lender knows your FICO score, home value, and loan goals.

Final Thoughts: Stay Current, Save Thousands

With so many homeowners exploring current home loan refinance rates, staying updated can help you make smart financial decisions. Even a small drop in your rate can translate to major savings, especially if you’re still paying off a 30-year loan.