Entering Utah’s housing market requires more than just finding the right property. it requires understanding how to finance it strategically. Whether you’re preparing to buy a home in Utah or planning long-term equity growth, knowing how FHA loans, refinancing options, and equity tools work together will put you in a stronger financial position.

This guide walks through the major financing options available to Utah buyers and explains how each decision impacts your long-term financial plan.

FHA Loans in Utah: Qualification, Credit Scores, and Loan Limits

For many buyers, FHA loans provide one of the most accessible paths to homeownership. These government-backed mortgages are especially helpful for borrowers with moderate income, limited savings, or credit challenges.

Those researching FHA loans for bad credit often find that FHA guidelines are more flexible than conventional programs. The typical FHA loan minimum credit score is lower than most traditional financing options, making it attractive for first-time buyers.

Understanding how to qualify for FHA loan programs requires reviewing income stability, debt-to-income ratio, and employment history. Before choosing FHA financing, buyers should evaluate the fha loan pros and cons, particularly mortgage insurance requirements. It’s also wise to compare FHA vs. conventional loan structures to determine which aligns best with your long-term financial goals. Additionally, county-specific FHA loan limits in Utah can influence how much you’re able to borrow, depending on where you plan to purchase.

Down Payment Assistance and First-Time Buyer Programs in Utah

One of the biggest obstacles for new homeowners is saving for a down payment. Fortunately, several first-time home buyer down payment assistance programs exist to reduce upfront costs.

Programs offering Utah first-time home buyer assistance and broader Utah down payment assistance programs help qualified buyers bridge the financial gap. Reviewing first-time home buyer requirements early ensures you’re fully prepared before entering the market.

If you’re still learning how to buy your first home, working with a local mortgage professional can clarify eligibility guidelines, documentation needs, and financing timelines.

In certain rural areas, a USDA loan Utah may also provide zero-down financing opportunities for eligible properties.

Monitoring Mortgage Rates and Evaluating Refinance Opportunities

Interest rates significantly affect monthly payments and long-term affordability. Keeping an eye on the mortgage rate forecast and reviewing a mortgage rate history chart can help you understand current market trends.

Choosing between a fixed vs adjustable mortgage is another critical decision. Fixed-rate loans offer payment stability, while adjustable-rate mortgages may offer lower introductory rates depending on market conditions.

After purchasing, many homeowners begin asking when they should refinance. To answer that, you must consider refinance closing costs, evaluate whether a no closing cost refinance makes sense, and compare current cash out refinance rates.

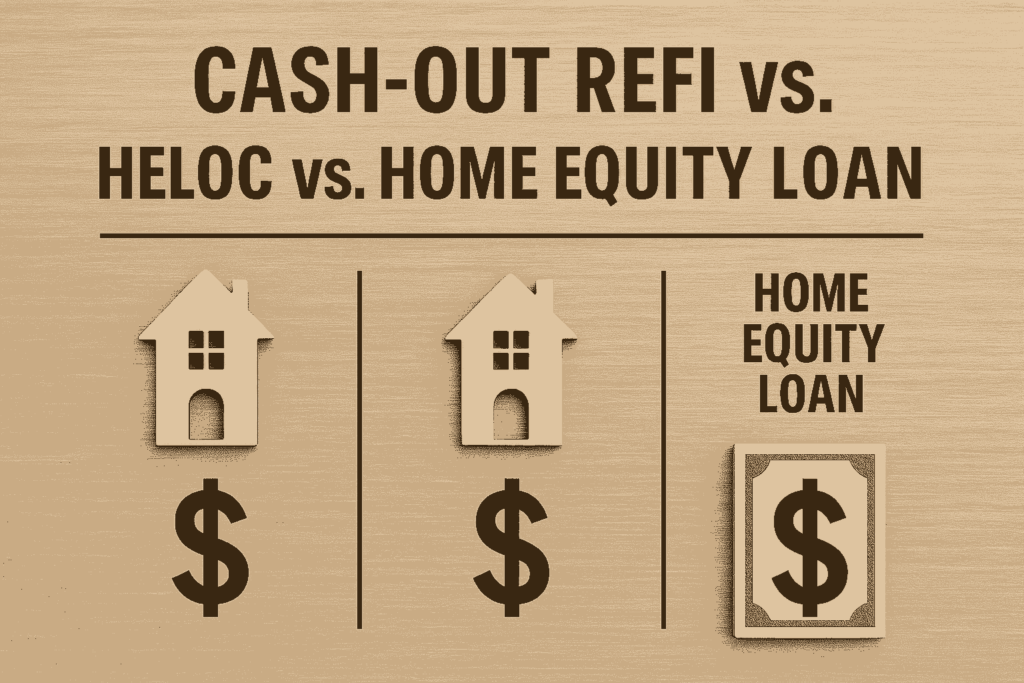

Some borrowers also compare refinancing vs. home equity loan options to determine which offers greater flexibility or lower overall borrowing costs.

Home Equity Loan vs HELOC: Accessing Built-Up Equity

As property values increase, homeowners build equity that can later be accessed strategically. Before applying, it’s important to understand how much equity is needed to qualify for secondary financing.

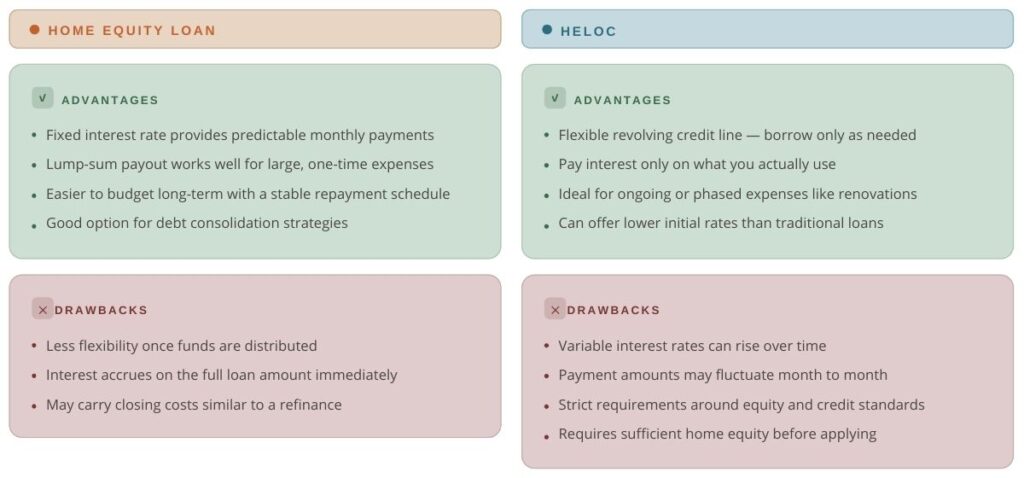

When comparing home equity loans vs. HELOC products, the primary difference is structure. A traditional home equity loan provides a lump-sum payment with fixed repayment terms, while a revolving line of credit offers more flexibility. Evaluating HELOC vs. home equity loan options allows homeowners to match borrowing structure with financial goals.

Understanding typical HELOC requirements, including minimum credit thresholds, equity levels, and income documentation, improves your chances of approval.

Many borrowers choose a home equity loan for debt consolidation to reduce high-interest balances and simplify monthly payments.

Building a Sustainable Strategy

Successfully planning to buy a home in Utah involves more than securing loan approval. It requires understanding how FHA loans, Utah assistance programs, refinancing strategies, and equity tools fit into a long-term financial plan.

By monitoring rate trends, comparing loan structures (e.g., fixed vs. adjustable mortgages), evaluating refinance timing, and preparing for future equity access, you position yourself for financial stability and growth.

Working with experienced Utah mortgage professionals ensures you remain informed as market conditions evolve and your goals change.