Welcome to your all-in-one guide for navigating home financing in 2025. Whether you’re buying your first home in Salt Lake City, refinancing, or exploring a 2025 FHA loan in Utah, this article walks you through the loan programs, rate trends, and equity opportunities Utah residents need to know right now.

Which Loan Type Is Right for You?

Let’s start with the basics. A 2025 FHA loan in Salt Lake City or St. George is designed for buyers with moderate credit and lower down payments. These loans are backed by the Federal Housing Administration, making them ideal for first-time homebuyers who want easier qualification.

If you’re a military veteran or active-duty service member, a 2025 VA loan in Utah offers zero down payment and no private mortgage insurance—major benefits that can save you thousands over the life of your loan. Be sure to check your eligibility through the VA Home Loan Requirements, and compare local options like a 2025 VA loan in Salt Lake City or St. George to find the best fit.

Buyers with strong credit scores and stable income might benefit most from a 2025 conventional mortgage in Utah. These loans typically offer lower long-term costs if you can make a 20% down payment. Local lenders in both Salt Lake City and St. George provide competitive rates and options.

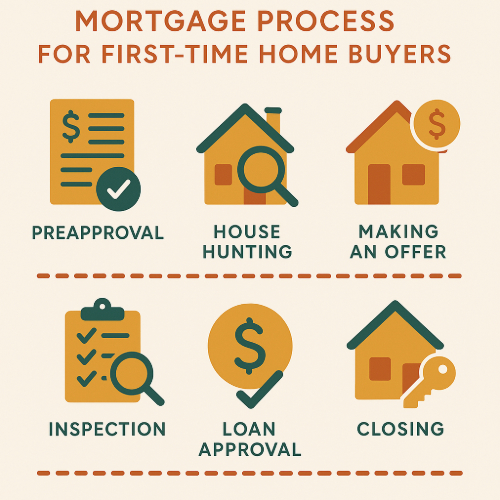

First-Time Buyers: Local Resources & Support

If this is your first home purchase, there’s good news—Utah is packed with programs designed to help. A 2025 first time home buyer in Utah may qualify for down payment assistance, homebuyer education, or reduced-rate programs. Cities like Salt Lake and St. George offer their own support too, such as the 2025 first time home buyer in Salt Lake City

grants or programs from local housing authorities in St. George.

Use these benefits to lower your entry costs and navigate the process with confidence.

Already Own a Home? Consider a Home Equity Loan

If you’re sitting on equity, 2025 might be the perfect time to tap into it. A 2025 home equity loan in Utah can help you fund renovations, invest in your business, or consolidate high-interest debt. Just be sure to compare offers from local banks—especially the best home equity rates Utah banks have available.

Rates and terms vary between lenders, so shop around. Consider options in your local market—whether it’s a 2025 home equity loan in Salt Lake City or a 2025 home equity loan in St. George.

Rates and Refinancing in 2025

Let’s talk about mortgage rates 2025. Right now, average rates in Utah are hovering around 6.5% to 7%. That’s higher than a few years ago but still very manageable, especially if you’re working with one of the top mortgage lenders 2024 or largest mortgage servicers 2024.

If you’re starting with an FHA loan, it may be smart to refinance later to a conventional loan to remove mortgage insurance. The strategy of refinancing an FHA loan to a conventional mortgage once you hit 20% equity is popular with savvy Utah homeowners.

Helpful Tools and Resources

Don’t leave things to guesswork—run the numbers. A US mortgage calculator with extra payments can help you estimate your monthly payments and see how even small extra payments can shave years off your loan. Want the full picture? View a full amortization schedule to track your payments over time.

It’s also a good idea to compare bank vs credit union mortgage rates. Credit unions may offer slightly lower rates or more personal service, while banks often provide faster preapprovals and digital tools.

Finally, keep an eye on lending trends. While conventional loans remain steady, government-backed loans are seeing a rise in delinquencies. Understanding these trends can help you make better long-term financial decisions.

Final Thoughts

There’s no one-size-fits-all approach to buying a home, but there are tools and strategies to make the process smoother. Whether you’re applying for a 2025 FHA loan in Utah, considering a 2025 VA loan, or comparing your options for a 2025 conventional mortgage in Salt Lake City, the key is to prepare early, ask questions, and compare multiple offers.

2025 could be your year to buy smart and build something lasting—right here in Utah.