Navigating the real estate market in the Beehive State can be daunting, but understanding how to get a mortgage is the first real step toward homeownership. Many prospective home buyers start their journey by exploring the financial landscape of home loans —the real competitive edge comes from securing a mortgage pre-approval. This document proves to sellers that a mortgage lender has already vetted your finances and is ready to back your offer.

To start the process, you should research the best mortgage companies and best mortgage lenders available in the state of Utah. Experts encourage you to get a mortgage quote from several different sources to ensure you get the best deal. While some buyers prefer large national banks, others have found that working with a local mortgage broker offers help with the local markets and a more personalized experience.

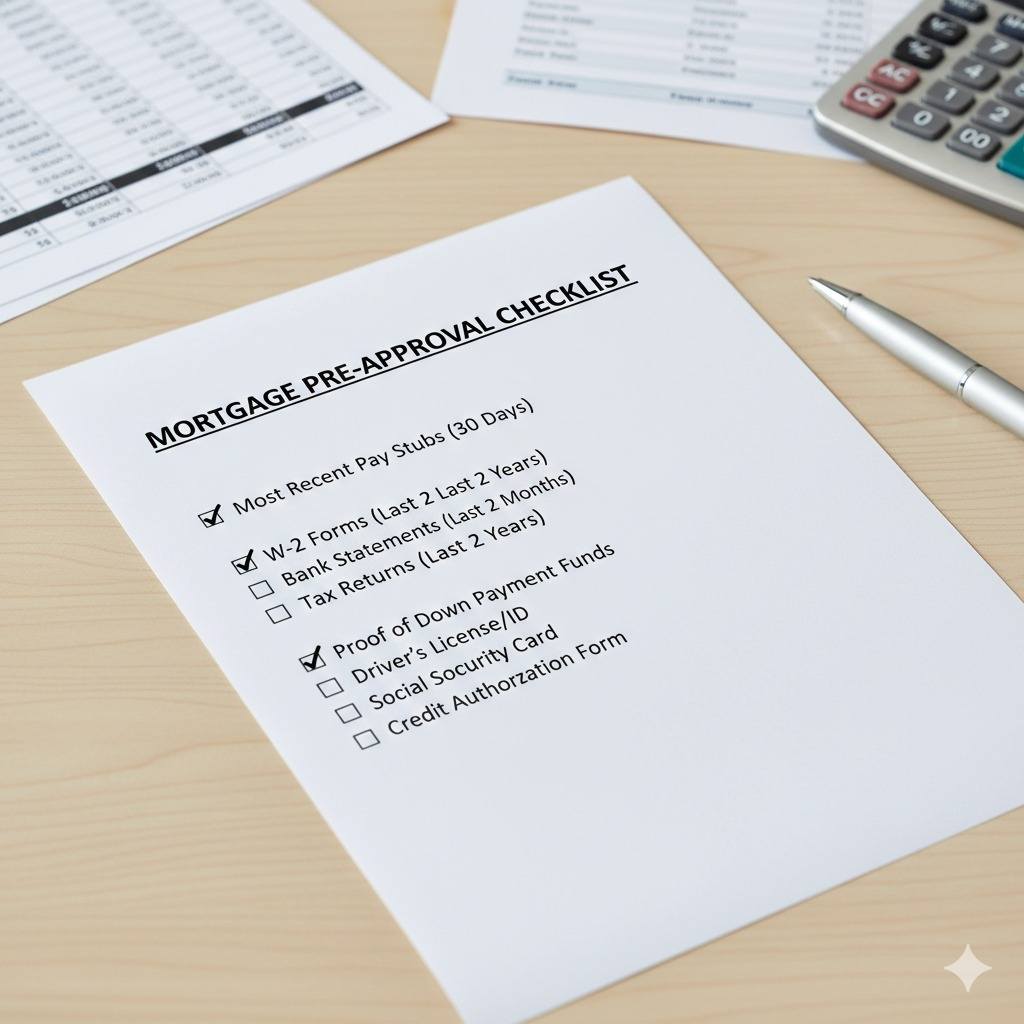

What You Need to Get Pre-Approved

When you sit down with a professional to discuss your mortgage application, you might ask, “What will I need to get a mortgage?” Generally, you will need to provide proof of income (such as W-2s and tax returns) and evidence of assets for a down payment. Knowing specifically what you need for pre-approval saves time and stops the underwriting process from stalling.

Once you have gathered your documents, the next question is timing. When should I apply for the mortgage loan paperwork? Ideally, this should happen before you even set foot in an open house. When should a lender pre-approve my mortgage loan? Most experts recommend getting your letter 3 to 6 months before you intend to buy. This gives you time to fix any credit issues that might arise during the steps to buying a house. When should you get a mortgage pre-approval? As soon as you are serious about entering the market.

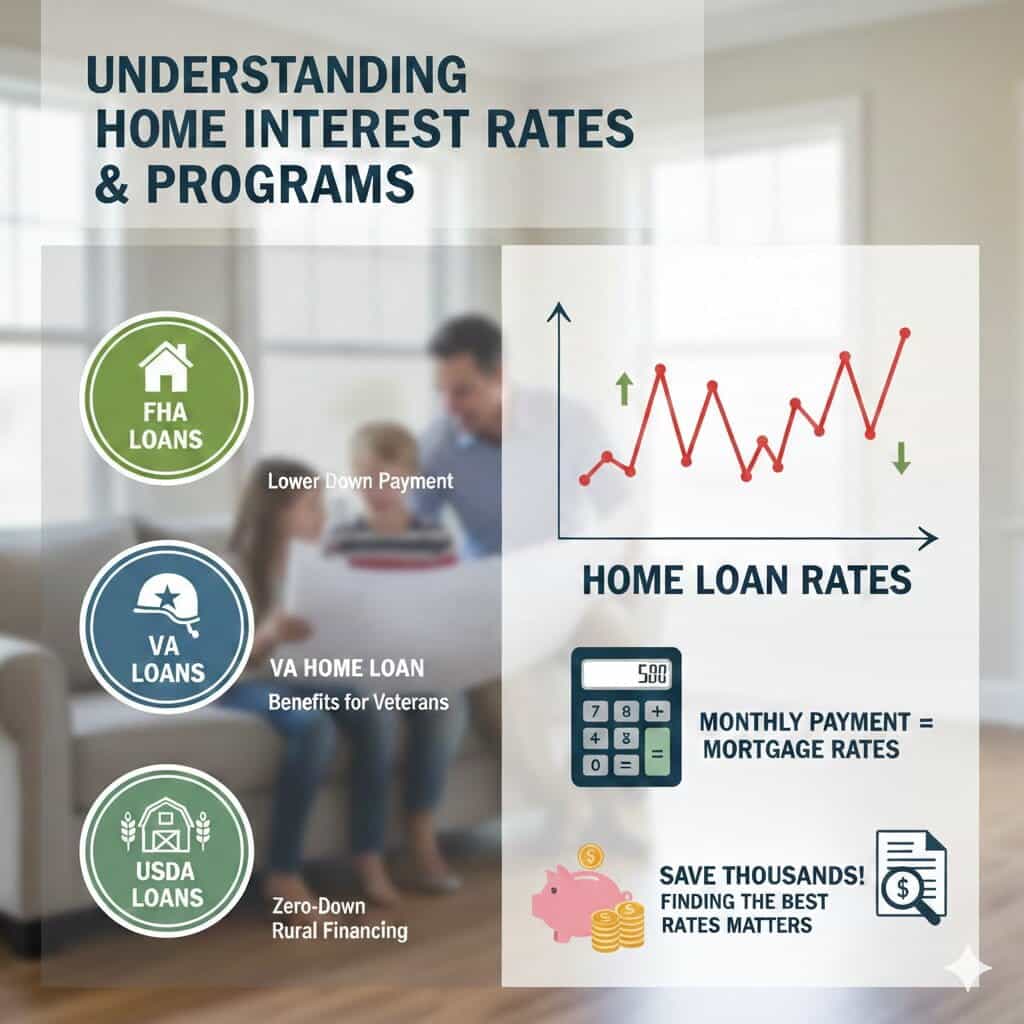

Understanding Home Loan Interest Rates and Programs

Your choice depends on your financial situation and specific program requirements. For many, FHA loans are an excellent entry point because they offer lower down payment options. Veterans should always look into a VA home loan, which provides significant benefits for those who have served. In more rural Utah communities, USDA loans are another powerful tool for zero-down financing.

Regardless of the program, current mortgage rates and home loan interest rates dictate your monthly payment. It pays to be diligent; finding the best mortgage or home loan rates can save you thousands of dollars over the lifetime of your loan. Keep a close eye on home loan rates, as they fluctuate with market conditions.

Finalizing Your Mortgage Pre-Approval in Utah

It is important to understand the difference between securing a home loan approval and obtaining a prequalification for a home. A pre-qualification is a surface-level look at your debt, while a pre-approval is a deep dive into your credit score. Most sellers in Utah will not even look at an offer without a formal pre-approval letter. As you finalize your plans, continue to monitor current mortgage rates and stay in close contact with your lender. Following these steps will position you to secure your dream home. Whether comparing lenders or quotes, preparation is the key to success.

Explore first-time home buyer mortgage Utah options, including mortgage rates Utah, FHA loan requirements Utah, Utah down payment assistance programs, and how to get pre-approved today.

First Time Home Buyer Mortgage Utah Guide (2026)

Buying your first home can feel overwhelming, but understanding the first-time home buyer mortgage process in Utah makes it far more manageable. From comparing mortgage rates in Utah to reviewing FHA loan requirements in Utah and local assistance programs, today’s buyers have more tools than ever to make smart financial decisions.

Many buyers begin by checking mortgage rates today and researching mortgage rate forecast trends. While timing matters, preparation matters more. Understanding affordability, loan programs, and credit requirements will position you for success whether rates rise or fall. Using a mortgage calculator in Utah can help estimate payments early and determine a comfortable budget.

first-time-home-buyer-utah.jpg

Mortgage Rates Utah and 30 Year Mortgage Rates Utah Today

Tracking mortgage rates in Utah is one of the most important steps for any buyer. Many borrowers monitor mortgage rates today, especially 30 year mortgage rates Utah, since the 30-year loan remains the most common option.

When reviewing mortgage rates forecast projections, remember that markets change quickly. Many buyers ask, are mortgage rates expected to drop in Utah or should they move forward now? Rather than waiting indefinitely, evaluate affordability and payment stability.

Using a mortgage calculator with extra payments can show how making additional principal payments reduces total interest. Buyers also frequently compare mortgage rate lock vs float strategies. If rates appear volatile, locking may protect your budget. If trends suggest improvement, floating may offer savings.

First Time Home Buyer Programs Utah and Utah Down Payment Assistance Programs

Saving for a down payment is often the biggest obstacle. Fortunately, several first-time home buyer programs in Utah and Utah down payment assistance programs exist to support new buyers.

These programs may include:

Down payment grants

Closing cost assistance

Reduced mortgage insurance

Education incentives

Many first-time home buyers search for Utah mortgage rates for first-time home buyers to find programs with competitive interest rates. Pairing assistance with favorable rates can dramatically improve affordability.

If savings or credit are limited, FHA loan requirements Utah often provide flexible qualification options. FHA programs allow lower down payments and can be paired with Utah down payment assistance programs for additional support.

home-buyer-programs-utah.jpg

FHA Loan Requirements Utah and Minimum Credit Score for Mortgage Utah

Understanding of loan requirements Utah is essential for buyers with moderate credit or limited savings. FHA financing is popular because it allows more flexible guidelines than many conventional loans.

Buyers frequently ask about the minimum credit score for the mortgage Utah standards. While requirements vary by lender, improving your credit score, reducing debt, and maintaining stable employment strengthen approval chances.

Veterans should also review VA loan eligibility Utah. VA loans often provide competitive interest rates and reduced down payment requirements for qualified borrowers.

If credit challenges exist, consider searching for mortgage lenders for bad credit or a mortgage broker near me for bad credit to identify specialized lending options. Many mortgage lenders with the best rates also offer consultation on improving approval strength before applying.

How Much House Can I Afford in Utah?

Before shopping for homes, calculate affordability. Many buyers search for ” how much house can I afford Utah to determine realistic price ranges.

Helpful tools include:

mortgage calculator Utah

mortgage calculator with extra payments

debt-to-income analysis

tax and insurance estimates

Using these tools helps align expectations with financial comfort. Just because you qualify for a certain amount does not mean you should spend the maximum. Responsible borrowing ensures long-term stability.

Mortgage Pre Approval Utah First Time Buyer

Getting mortgage pre approval the first time buyer, documentation completed early provides a strong advantage. Sellers take pre-approved buyers more seriously, and you will understand your exact price range.

The pre-approval process typically includes:

Credit evaluation

Income verification

Asset review

Employment confirmation

Many buyers search for ” mortgage broker near me reviews or mortgage broker near me first time home buyer to find trusted local professionals. Comparing mortgage lenders near me ensures competitive pricing and service. Some buyers also compare mortgage lenders for bad credit if credit improvement is needed before closing.

Choosing Between Mortgage Lenders Near Brokers and Me

Working with experienced professionals can simplify the process. Searching for mortgage lenders near me or mortgage lenders with the best rates allows you to compare options and find competitive financing.

Mortgage brokers often provide access to multiple lenders, which may help buyers with unique credit or income situations. Whether working with a broker or a direct lender, transparency and communication are key.

When Should I Lock My Mortgage Rate?

Many buyers wonder:

When should I lock my mortgage rate

Are mortgage rates expected to drop utah

mortgage rate lock vs float

Locking a rate protects against increases, while floating may benefit buyers if rates decline. Your decision should depend on market trends, risk tolerance, and closing timeline rather than speculation alone.

Final Thoughts on First-Time Home Buyer Mortgage Utah

Navigating the first-time home buyer mortgage process in Utah requires preparation and knowledge. By understanding mortgage rates Utah, 30 year mortgage rates Utah today, and available first-time home buyer programs Utah, buyers can move forward with confidence.

Review FHA loan requirements Utah, explore Utah down payment assistance programs, and calculate affordability using a mortgage calculator Utah. Then begin the mortgage pre approval Utah first time buyer process with trusted mortgage lenders near me.

With the right preparation and strategy, purchasing your first home in Utah can be both achievable and financially smart.

Entering Utah’s housing market requires more than just finding the right property. it requires understanding how to finance it strategically. Whether you’re preparing to buy a home in Utah or planning long-term equity growth, knowing how FHA loans, refinancing options, and equity tools work together will put you in a stronger financial position.

This guide walks through the major financing options available to Utah buyers and explains how each decision impacts your long-term financial plan.

FHA Loans in Utah: Qualification, Credit Scores, and Loan Limits

For many buyers, FHA loans provide one of the most accessible paths to homeownership. These government-backed mortgages are especially helpful for borrowers with moderate income, limited savings, or credit challenges.

Those researching FHA loans for bad credit often find that FHA guidelines are more flexible than conventional programs. The typical FHA loan minimum credit score is lower than most traditional financing options, making it attractive for first-time buyers.

Understanding how to qualify for FHA loan programs requires reviewing income stability, debt-to-income ratio, and employment history. Before choosing FHA financing, buyers should evaluate the fha loan pros and cons, particularly mortgage insurance requirements. It’s also wise to compare FHA vs. conventional loan structures to determine which aligns best with your long-term financial goals. Additionally, county-specific FHA loan limits in Utah can influence how much you’re able to borrow, depending on where you plan to purchase.

Down Payment Assistance and First-Time Buyer Programs in Utah

One of the biggest obstacles for new homeowners is saving for a down payment. Fortunately, several first-time home buyer down payment assistance programs exist to reduce upfront costs.

Programs offering Utah first-time home buyer assistance and broader Utah down payment assistance programs help qualified buyers bridge the financial gap. Reviewing first-time home buyer requirementsearly ensures you’re fully prepared before entering the market.

If you’re still learning how to buy your first home, working with a local mortgage professional can clarify eligibility guidelines, documentation needs, and financing timelines.

In certain rural areas, a USDA loan Utah may also provide zero-down financing opportunities for eligible properties.

Monitoring Mortgage Rates and Evaluating Refinance Opportunities

Interest rates significantly affect monthly payments and long-term affordability. Keeping an eye on the mortgage rate forecast and reviewing a mortgage rate history chart can help you understand current market trends.

Choosing between a fixed vs adjustable mortgage is another critical decision. Fixed-rate loans offer payment stability, while adjustable-rate mortgages may offer lower introductory rates depending on market conditions.

After purchasing, many homeowners begin asking when they should refinance. To answer that, you must consider refinance closing costs, evaluate whether a no closing cost refinance makes sense, and compare current cash out refinance rates.

Some borrowers also compare refinancing vs. home equity loan options to determine which offers greater flexibility or lower overall borrowing costs.

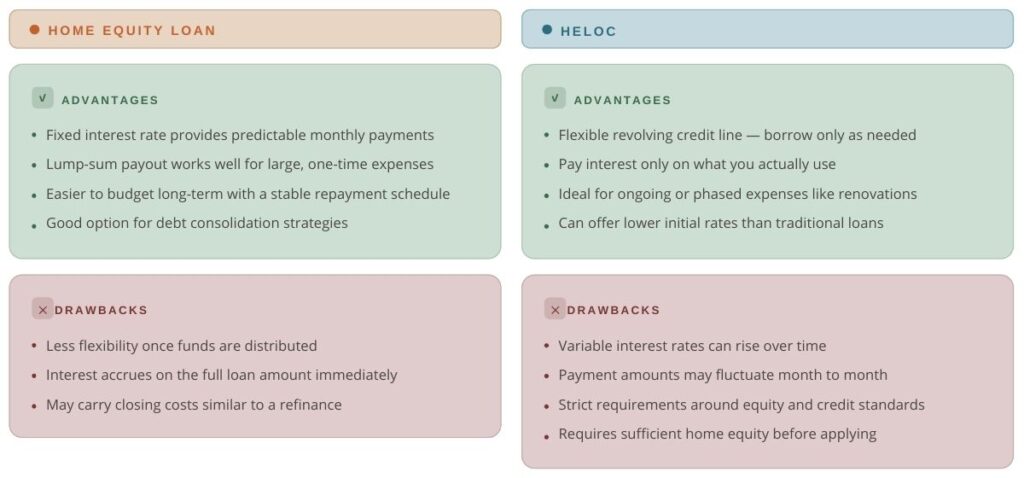

Home Equity Loan vs HELOC: Accessing Built-Up Equity

As property values increase, homeowners build equity that can later be accessed strategically. Before applying, it’s important to understand how much equity is needed to qualify for secondary financing.

When comparing home equity loans vs. HELOC products, the primary difference is structure. A traditional home equity loan provides a lump-sum payment with fixed repayment terms, while a revolving line of credit offers more flexibility. Evaluating HELOC vs. home equity loan options allows homeowners to match borrowing structure with financial goals.

Understanding typical HELOC requirements, including minimum credit thresholds, equity levels, and income documentation, improves your chances of approval.

Many borrowers choose a home equity loan for debt consolidation to reduce high-interest balances and simplify monthly payments.

Building a Sustainable Strategy

Successfully planning to buy a home in Utah involves more than securing loan approval. It requires understanding how FHA loans, Utah assistance programs, refinancing strategies, and equity tools fit into a long-term financial plan.

By monitoring rate trends, comparing loan structures (e.g., fixed vs. adjustable mortgages), evaluating refinance timing, and preparing for future equity access, you position yourself for financial stability and growth.

Working with experienced Utah mortgage professionals ensures you remain informed as market conditions evolve and your goals change.

Thinking about buying a home in Utah in 2025? Learn about first-time buyer programs, local mortgage rates, refinancing options, and expert tips to make your journey smoother.

Is 2025 Your Year to Buy a Home in Utah?

If you’re thinking about buying a home in Utah in 2025, chances are you’ve got a lot on your mind. Maybe it’s your first time, and you’re just trying to understand where to begin. Or maybe you already own a home and are wondering whether this is the right year to refinance or invest in a second property.

Wherever you are in the process, you’re not alone—and you don’t have to figure it all out at once.

We’ve pulled together this guide to help you feel more informed and confident—whether you’re comparing Utah mortgage rates today, researching first time home buyer Utah programs 2025, or trying to connect with the best mortgage companies in Salt Lake City.

First Time Buyer? Let’s Talk Programs and Loan Options

Being a first-time buyer can feel overwhelming, but Utah offers a surprising amount of support. Through first time home buyer programs 2025, you may qualify for lower rates, better terms, and even down payment assistance to make buying your first home more affordable.

You’ll want to explore first time home buyer loan options, which might include FHA, VA, or conventional loans tailored for first-time buyers. Each has pros and cons, but a good lender will help you find the best mortgage for first time home buyer situations based on your income, credit, and goals.

What’s the Market Like Right Now?

The housing market is shifting, but it’s not as scary as headlines make it sound. Utah mortgage rates today are still in a relatively stable place, and that means there are real

opportunities if you’re ready.

Loan thresholds have also changed. The FHA loan limits Utah 2025 increase allows you to borrow more while still qualifying for a government-backed mortgage. For veterans, VA loan lenders in Utah remain a strong option with zero down and competitive rates.

Working With Local Experts Makes a Difference

While big banks have their place, local expertise matters—especially in today’s market. A mortgage broker Ogden Utah or a mortgage lender Sandy Utah can offer advice that’s grounded in local market knowledge.

Don’t forget about credit unions. Many buyers find better terms through the best Utah credit unions for mortgages, especially when it comes to customer service and flexible underwriting.

Already Own a Home? It Might Be Time to Refinance

If you’ve been thinking about refinancing, 2025 could be your moment. Whether you want to lower your payment or tap into equity, the best place to refinance a mortgage in Utah might be right around the corner—or even your local credit union.

You might also consider a HELOC. Researching the best banks for HELOC in Utah can help you fund renovations, cover college tuition, or consolidate debt—all with more flexibility than a traditional loan.

What If You’re Not Ready to Buy?

Not everyone is ready to commit to a mortgage just yet. For those looking for a more gradual path to ownership, rent to own homes Utah offer a hybrid option—letting you live in the home while working toward ownership.

Others may be exploring investment property mortgage rates, especially with rental demand rising across the state. Or, if you’re dreaming of a mountain getaway, just make sure you’re up to speed on second home mortgage rules, which have stricter requirements than primary residences.

Planning to Buy a House in Utah in 2025?

Whether you’re gearing up for your first purchase or adding to your real estate portfolio, buying a house in Utah 2025 doesn’t have to be overwhelming. With the right programs, a trustworthy lender, and a little guidance, you can make smart choices that work for your budget—and your future.

From first time home buyer down payment assistance to investment property mortgage

rates, the tools are out there. All you need is the right roadmap.