For many Utahns, the dream of homeownership is alive and well — but if you’re self-employed, that dream might feel just out of reach. The good news? It’s absolutely possible to qualify for a home loan when you’re your own boss. This guide breaks down what you need to know about getting a mortgage when self employed, with a special focus on loan options like bank statement mortgages loans and no doc mortgages products.

How to Get a Mortgage Being Self-employed in Utah

If you’re a freelancer, entrepreneur, or small business owner, lenders evaluate your income differently. You’ll typically need:

Two years of tax returns

Profit & loss statements and business licenses

Personal/business bank statements

Strong credit score

Low debt-to-income ratio (DTI)

Additionally, some lenders may also request a mortgage pre-approval for self-employed borrowers. Use a self-employed mortgage calculator to run the numbers in advance.

Self-employed Mortgage Options: Bank Statement Loans vs No Doc Mortgage

Bank Statement Loans

Perfect for freelancers and gig workers. These loans use 12–24 months of bank statements instead of tax returns. This is a great option when your adjusted gross income doesn’t reflect your actual cash flow.

No Doc Mortgage

These require minimal paperwork and are ideal for those with excellent credit and strong assets. They’re offered by the best no doc mortgage lenders like Truss Financial and select niche lenders.

Need help deciding? Search for a mortgage broker that specializes in self-employed mortgages to guide you.

Best Lenders for Self-employed Mortgages

Whether you’re searching for bank statement home loans or Utah’s best mortgage broker for self-employed clients, prioritize lenders who:

Understand SMB (small and medium business) income

Have flexible underwriting

Are based in or familiar with Utah’s current mortgage climate

Pro tip: Some lenders offer a no doc HELOC for property owners who want more liquidity.

Utah Mortgage Rates Right Now (and How to Lock In Yours)

Compare current mortgage rates and Salt Lake City mortgage rates daily. Timing matters! Ask your lender how to lock in mortgage rate Utah to avoid rate fluctuations during underwriting. Platforms like MortgageRateUtah.com let you view Utah mortgage rates right now with real-time data.

Working with a Local Broker

Searching for a mortgage broker near you? A seasoned local broker can help you:

Get mortgage pre approval

Compare best home loan lenders for self employed

Navigate the unique Utah market

If needed, ask for referrals or search online directories. A good broker makes all the difference for the self employed mortgage process.

Final Takeaway

All things considered: can you get a mortgage? Yes — especially with the right resources. Gather your financials, explore your options, and use tools like MortgageRateUtah.com to compare Utah lenders and secure the best deal.

HELOC vs Home Equity Loan in Utah? That’s the big question…

Utah homeowners looking to unlock the value of their properties in 2025 are faced with an important decision: should you choose a Home Equity Line of Credit (HELOC) or a home equity loan? Both options allow you to access funds using your home’s equity, but they differ in structure, flexibility, and long-term costs. In this guide, we’ll compare the two options using ALL of the key mortgage-related keywords to help you decide which is the better fit for your financial goals.

Mortgage Rates and Home Equity Options in Utah

Understanding mortgage rates is essential when choosing between a HELOC and a home equity loan. In 2025, Utah homeowners can expect home equity loan rates between 6.5% and 8.5%, while HELOCs range from 7.1% to 9.5%. Unlike mortgage rates today for new purchases, equity loans are based on your available equity and credit profile.

Using our mortgage calculator, homeowners can estimate their home loan calculator inputs to decide between fixed vs. variable interest products.

Home Equity Loan vs HELOC: A Mortgage Calculator Breakdown

A home equity loan gives borrowers a lump sum with fixed interest rates, while a HELOC offers revolving credit with variable interest. Use a mortgage calculator to analyze:

Monthly mortgage payments

Long-term interest cost projections

Amortization over 10–30 years

Compare Utah’s average home equity loan rates using trusted local lenders like Zions Bank, America First Credit Union, and SecurityNational Mortgage.

Mortgage Refinancing vs Home Equity Loans

Many homeowners debate between mortgage refinancing, a cash-out refinance, or a home equity product. If your current mortgage rate is low, refinancing may not be cost-effective. Instead, using a home equity line of credit or loan preserves your original rate while unlocking funds for:

Renovations

Debt consolidation

Tuition or medical bills

Use a mortgage quote tool to check Utah’s current refinance home loan rates.

Using a VA Loan Calculator and Other Niche Tools

Veterans may qualify for special home equity products tied to a VA home loan. While VA loan calculators are often used for home purchase estimates, they also help calculate refinance or equity loan costs. If you already used a VA home loan for your mortgage, ask lenders about cash-out refinance VA programs in Utah.

Find the Best Mortgage Lenders and Brokers Near You

When applying for a home equity product, you’ll need a mortgage lender or mortgage broker near me. Top Utah-based options for 2025 include:

Read online reviews to find the best mortgage companies and the best mortgage companies for first time buyers.

Reverse Mortgage Calculator and Retirement Planning

If you’re 62 or older, a reverse mortgage calculator can help estimate loan amounts based on your home value. This is different from a traditional HELOC, but still uses home equity. Compare it to a home equity loan to see which better meets retirement income needs.

Apply for a Mortgage or Equity Product

Ready to move forward? Many Utah lenders let you apply for a mortgage or equity loan online. Make sure you’re mortgage pre-approved by submitting your application early. For a smoother experience:

Gather proof of income and home value

Review credit reports

Compare lender fees using a mortgage calculator

Conclusion: Which Option is Right for You?

Choosing between a HELOC and home equity loan in Utah depends on your unique needs:

Prefer fixed rates and lump sums? Choose a home equity loan.

Need flexibility and phased access to funds? Go with a HELOC.

Use the mortgage calculator to run your numbers. Then get a personalized mortgage quote, review your options, and speak to a mortgage lender.

Utah mortgage rates 2025 are shifting due to inflation, interest rate policies, and evolving economic trends in the state. Whether you’re a first-time homebuyer or refinancing an existing loan, understanding the current mortgage landscape in Utah is essential. In this guide, we’ll explore the latest rate updates, compare top lenders, and share expert tips to help you secure the best deal possible.

Utah mortgage rates 2025

Understanding Mortgage Rates Utah in 2025

Utah mortgage rates 2025 are shifting as the housing market responds to inflation, policy changes, and local economic trends. Whether you’re a first-time buyer or looking to refinance, understanding how rates are trending in Utah can help you make smarter financial decisions. In this guide, we’ll break down the latest rate updates, tools to compare lenders, and tips to secure the best home loan for your needs.

borrowers are seeing depend on factors like loan type, credit score, down payment, and even location.Navigating the landscape of mortgage rates Utah can feel overwhelming, especially as we head into 2025. Whether you’re buying your first home, refinancing, or comparing lender offers, having accurate information is essential. Current mortgage rates Utah

Daily Tracking: Why Mortgage Rates Today Matter

Mortgage interest rates change quickly. Federal Reserve updates, market conditions, and inflation reports all influence rate fluctuations. By monitoring Utah mortgage rates 2025, homebuyers and investors can time their decisions more effectively and potentially save thousands in interest over the life of the loan.

Find the Has to OfferBest Mortgage Rates Utah

To lock in the lenders provide, you need to:best mortgage rates Utah

– Compare multiple lenders – Use a reliable mortgage estimator Utah – Review loan options like FHA, VA, and conventional loans

Salt Lake City home loan rates may vary based on lender policies or local promotions.If you’re located in Salt Lake, consider checking mortgage rates Salt Lake City for region-specific offers.

Factors Impacting Utah Mortgage Rates 2025

Several variables affect the mortgage rates you’re offered in Utah:

Loan type (FHA, VA, conventional)

Credit score

Down payment amount

Property location

Because of these factors, Utah mortgage rates 2025 vary across borrowers and lenders. It’s important to evaluate offers tailored to your financial profile.

Using the Right Tools: Estimators & Calculators

mortgage calculator mortgage rates or a Smart homebuyers use a mortgage estimator with taxes to calculate their full monthly cost, including property tax and insurance. Tools like a home loan mortgage rates calculator offer deeper insights. The best platforms also provide a Utah mortgage calculator with real-time rate comparisons.

Compare Utah Mortgage Lenders

compare Utah mortgage rates side-by-side using objective tools before locking in a rate.There are several Utah mortgage lenders offering competitive packages. When shopping, don’t just look at advertised rates—check APRs, fees, and closing costs. It’s also smart to

Loan Types: FHA, VA & More

Different loans come with different rates. For example:

Utah home loan rates will depend on your financial profile and loan structure.- Utah FHA loan rates are popular for first-time buyers due to their low down payment options. – Utah VA loan rates offer incredible value to veterans and active military members, often with no down payment. – Standard

Comparing Utah Mortgage Rates 2025 Offers

Don’t rely on a single lender’s offer. To find the best Utah mortgage rates 2025, compare:

Interest rate vs APR

Loan term (15 vs 30 years)

Lender fees and closing costs

Use a mortgage rate comparison tool or a Utah-specific loan estimator to make informed comparisons.

First Time Home Buyer Utah: Tailored Programs

If you’re a first time home buyer Utah offers several grant and assistance programs that help reduce upfront costs and secure better terms. Many lenders also offer special Utah housing loan rates for qualifying buyers.

How to Secure the Lowest Mortgage Rates in Utah

Securing the lowest mortgage rates in Utah comes down to preparation:

– Improve your credit score – Choose a shorter loan term – Provide a larger down payment – Shop during low-rate cycles

Using these tactics can help you lower your Utah interest rates home loan and save thousands over the life of your mortgage.

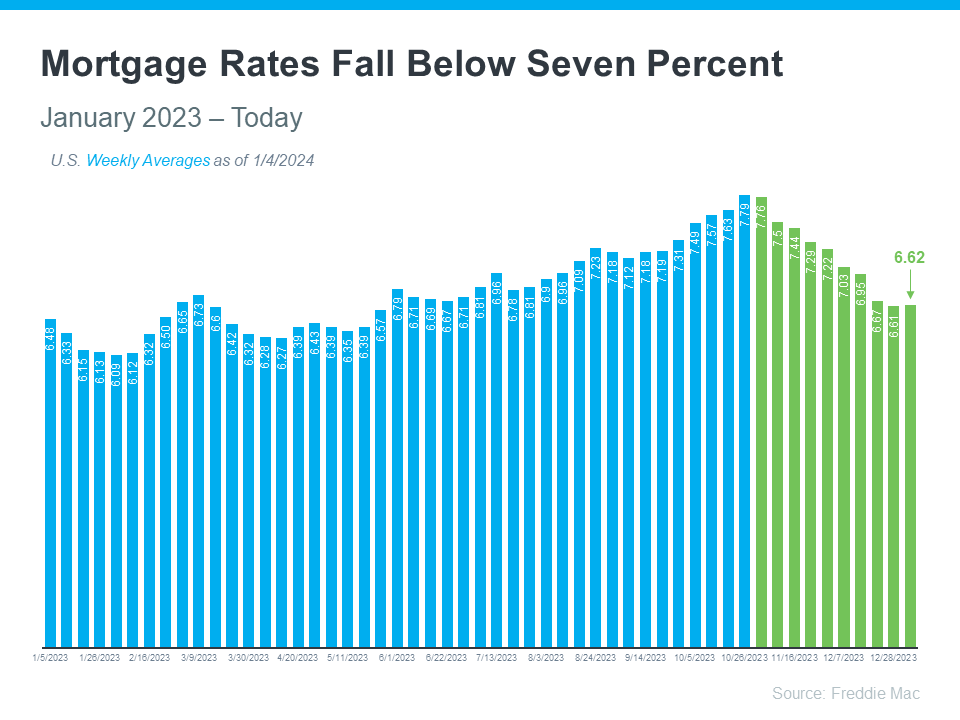

If you’re looking to buy a home or refinance, understanding Utah mortgage rates today is essential. Rates fluctuate daily based on national trends, inflation, and your personal financial profile. As of mid-2025, 30-year mortgage rates in Utah are around 6.75%, while 15-year mortgage rates average 6.1%.

Use a mortgage rate calculator to estimate your specific rate, or get a custom mortgage quote from local mortgage lenders in Utah.

Image Placement Note

“Utah homes with mortgage rate chart overlay”

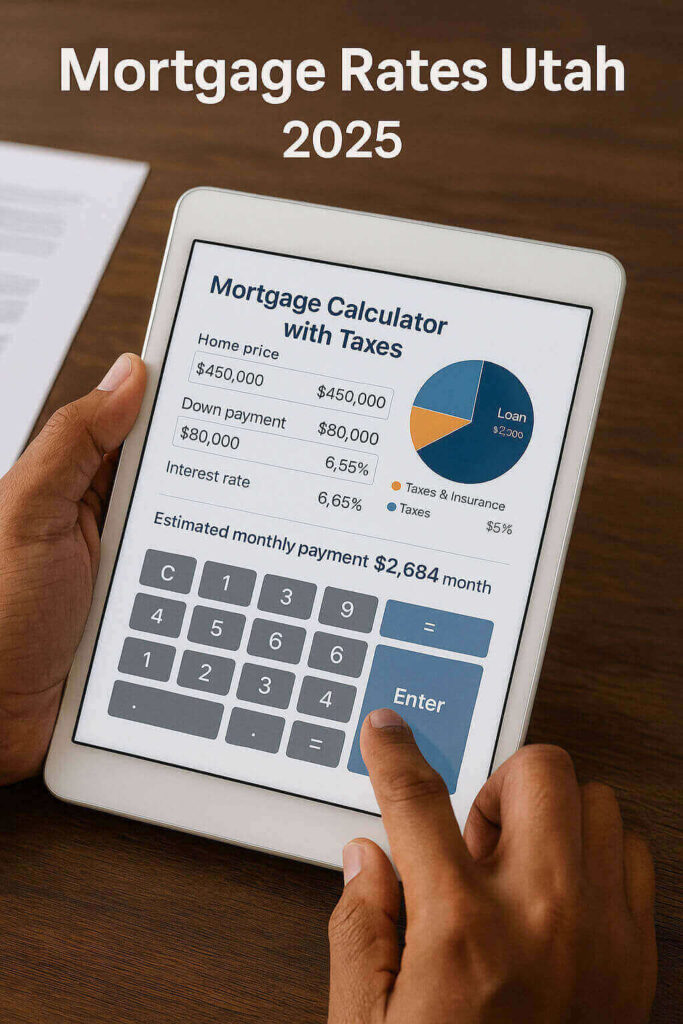

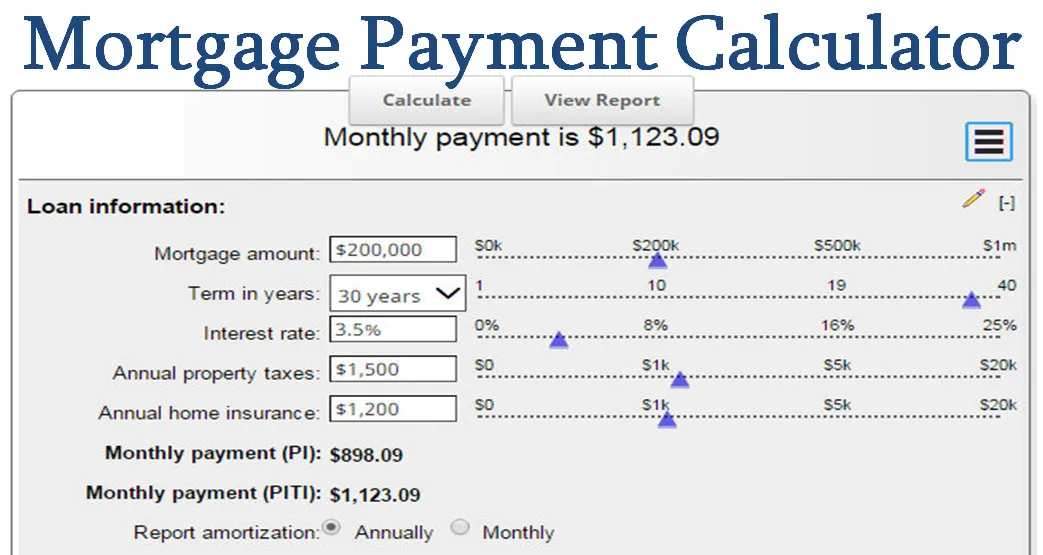

Use a Mortgage Calculator to Plan Your Budget

Before you apply, try our mortgage calculator to calculate monthly payments. This tool factors in loan amount, term, rate, property taxes, and insurance. You can also explore a:

Mortgage payment calculator

Mortgage affordability calculator

Refinance calculator

Mortgage pre approval calculator

VA loan calculator

Each of these tools can help you decide how much house you can afford.

Image Placement Note

“Visual of mortgage calculator inputs and monthly breakdown”

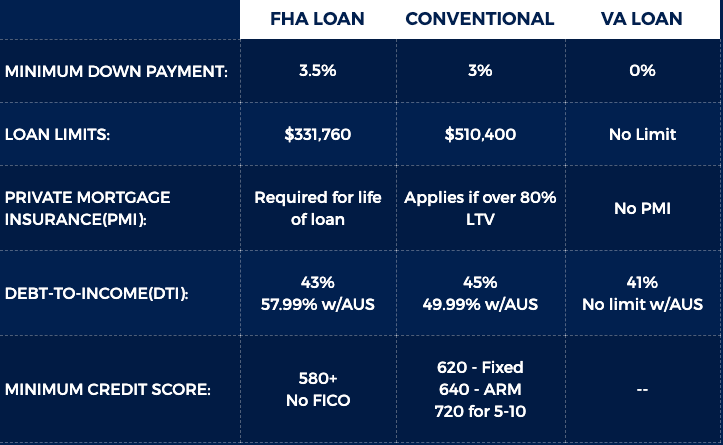

Types of Home Loans in Utah

Choosing the right loan helps you save money over time. Here’s a breakdown:

Conventional Loans: Ideal for borrowers with strong credit.

FHA Loans: Designed for first-time buyers with low down payments.

VA Home Loans: Available to veterans and active-duty military. Try a VA loan calculator to estimate savings.

USDA Loans: Zero-down options for rural and suburban homebuyers.

Jumbo Loans: Used for high-value homes exceeding $726,200.

Be sure to compare home loan interest rates to find the best fit.

Image Placement Note

“Chart showing FHA vs VA vs conventional loan features”

Refinance Options to Lower Your Payments

Already a homeowner? Explore refinance home loan options:

Lower your rate

Shorten loan term

Switch to a fixed rate

Take cash out (see cash out refinance calculator)

Popular choices include:

FHA Streamline refinance

VA refinance (IRRRL)

Cash out refinance

Traditional refinance mortgage rates

Compare refinance rates from multiple mortgage lenders Utah to find the best offer.

Tap Your Equity With a Home Equity Loan

Looking for funds to renovate or pay off high-interest debt? Consider a home equity loan or home equity line of credit (HELOC). Tools like a home equity loan calculator and heloc rates checker can help you evaluate payment plans.

Compare home equity loan rates and read the terms carefully.

Get Pre-Approved & Shop With Confidence

A mortgage pre approval gives you a competitive edge when placing an offer on a home. Most lenders allow you to get pre approved for a mortgage online in minutes.

Also explore:

Prequalify for home loan

Get prequalified for a mortgage

First time home buyer programs

Find the Best Mortgage Lenders in Utah

Whether you’re looking for the best mortgage companies or a mortgage broker near me, make sure they offer:

Transparent interest rates today

Fast pre-approvals

Clear closing cost estimates

Search reviews, ask questions, and compare at least three offers to secure your best deal.

At first, applying for a home loan may seem overwhelming. However, understanding what to expect can help reduce uncertainty and you can apply for a mortgage loan now! Once you apply, the lender immediately begins reviewing your finances, verifying your details, and ordering a home appraisal. Typically, the home loan processing time lasts between 30 and 45 days. Nevertheless, this can vary depending on your financial profile, loan type, and how quickly you submit required documents.

Now that you know the typical timeline, let’s look at what actually happens during that time. The mortgage application process begins with preapproval—this gives you a clear sense of your budget. After that, you’ll submit a formal application. From there, the lender evaluates your credit, income, and assets during underwriting. Once approved, you’ll schedule a closing and sign your final loan documents.

Mortgage Documents Needed to Get Started and Apply

To keep things moving smoothly, you’ll want to have your documents ready early. Most lenders require:

Recent pay stubs or income statements

W-2s or tax returns from the past two years

Bank statements

A valid photo ID

Proof of employment

By gathering these mortgage documents ahead of time, you’ll speed up the approval process and reduce the chance of delays.

Mortgage Loan Terms You Should Know

As you fill out your application and review loan options, you’ll likely encounter unfamiliar terminology. Key mortgage terms include:

Fixed-rate vs. adjustable-rate (ARM): Fixed rates remain constant, while ARMs may increase or decrease over time.

Loan term: Most commonly 15 or 30 years, this defines how long you’ll repay your loan.

Principal and interest: The principal is the loan amount; interest is the cost of borrowing.

Escrow: A third-party account that holds funds for taxes and insurance.

Understanding these terms will help you compare loan offers with confidence.

Choosing the Right Mortgage Loan for You

With a basic understanding of terms, the next step is choosing the right loan. If you’re looking for lower payments upfront, an interest only mortgage might work for you—this lets you pay just the interest for a set period before principal payments begin.

Alternatively, if you’re buying in a rural or suburban area, a USDA mortgage could offer zero down payment and competitive rates—perfect for buyers who meet income and location requirements

Down Payment Assistance for Homebuyers

Many buyers struggle with saving enough for a down payment—but down payment assistance programs can help. These programs may offer grants, low-interest loans, or forgivable loans to cover part of your upfront costs. They are often available for first-time buyers, low-income households, or those purchasing in certain areas.

Mortgage Insurance: What you need to know

If your down payment is less than 20%, your lender will likely require mortgage insurance. This protects the lender—not you—in case of default. Conventional loans use PMI (Private Mortgage Insurance), while FHA and USDA loans include their own insurance structures. Make sure to factor this into your monthly costs.

Yes, you can still refinance with less-than-perfect credit. Government-backed programs—such as the FHA Streamline or VA IRRRL—allow qualified borrowers to lower their monthly payments or move into a fixed-rate mortgage. While your interest rate may be higher, refinancing can still offer long-term savings and stability

You can Apply Today!

Buying a home is one of the most meaningful financial decisions you’ll ever make—and you don’t have to do it alone. By understanding the loan process, preparing your documents, and exploring the right mortgage options, you’re already one step closer to achieving your goal. Whether you’re a first-time buyer, exploring refinancing, or looking for down payment support, the tools and resources are within reach. So take that next step with confidence and apply for a mortgage loan now—your new home is closer than you think.

Are you dreaming of owning a home in the Beehive State? Utah’s thriving economy and stunning landscapes make it a desirable place to live. However, understanding the mortgage landscape can be daunting for first-time buyers and seasoned homeowners alike. This comprehensive guide will navigate you through the essential aspects of home loans in Utah, ensuring you’re well-equipped to make informed decisions.

Understanding Mortgage Rates in Utah

One of the first things potential homebuyers research is mortgage rates Utah. In Utah, these rates can fluctuate based on national trends, economic factors specific to the state, and even local market conditions. It’s crucial to stay informed about current mortgage rates to understand your potential monthly payments. Keep an eye on resources that provide mortgage rates daily and specifically track mortgage rates Salt Lake City for the most relevant local information. For up-to-the-minute information, consider searching “mortgage rates in Utah today.”

Exploring Home Loan Options

Securing a home loan is a significant step. Utah offers various options, from conventional loans to government-backed programs. For veterans, VA home loans provide attractive benefits, often with no down payment. First-time buyers should explore first-time home buyer programs, which can offer down payment assistance Salt Lake City and other forms of financial aid. Some home loans for teachers are also available through targeted programs. Understanding these options is key to finding the best fit for your individual circumstances.

Leveraging HELOCs and Home Equity

For homeowners looking to leverage their existing equity, a HELOC (home equity line of credit) can be a flexible solution. A HELOC allows you to borrow against the equity in your home, often at competitive HELOC rates Utah. Check current HELOC rates from various lenders. Alternatively, a home equity loan provides a lump sum of cash, typically at a fixed interest rate. Utah homeowners can use these options for home improvements, debt consolidation, or other financial needs. It’s also worth comparing a HELOC with other options like a cash-out refinance.

Dealing with Credit Challenges

Many potential homebuyers worry about bad credit loans. While having a strong credit score is ideal, it’s not always a deal-breaker. There are lenders who specialize in refinance with bad credit options, although interest rates may be higher. Explore options for credit repair and consider strategies to improve your credit before applying for a home loan interest rates Utah.

The Importance of a Mortgage Calculator

A mortgage calculator is an invaluable tool for homebuyers. It helps you estimate your monthly payments, factoring in the loan amount, interest rate, and loan term. Online resources offer various calculators, including jumbo loan calculator, VA loan calculator, and refinance calculator. Use these tools to understand your budget and assess your affordability. You can also explore tools like the home loan calculator to see various scenarios. Even consider a specialized calculator like a HELOC calculator if you are contemplating that option.

Working with Mortgage Professionals

Navigating the mortgage process is often easier with the help of a professional. A mortgage lender can guide you through the application process and help you compare different loan options. A mortgage broker near me may provide access to a wider range of lenders, potentially securing you a better rate. If you’re building a home, search for a professional specializing in home loan interest rates Ogden to ensure you get the best local advice.

Don’t just search for best mortgage companies online—seek personalized advice to make the right choice for your financial future.

When it comes to buying a home or refinancing in Utah, understanding your mortgage costs upfront is critical. A mortgage calculator can help you estimate monthly payments, compare loan terms, and see how interest rates will affect your total investment. In this guide, we’ll walk through everything you need to know about mortgage tools, rates, and approval estimators to help you make informed decisions.

Use our Utah mortgage calculator to estimate monthly payments and compare loan options tailored to your budget.

This guide walks you through how to use a mortgage calculator, estimate your approval odds, and find today’s most competitive mortgage loan rates.

Mortgage Rates Today: What to Expect in Utah

Staying on top of mortgage rates today is key to getting the best deal. Rates fluctuate daily based on economic conditions, inflation, and your creditworthiness. Right now, Utah’s current mortgage rates for a 30-year fixed loan hover between 6.5% and 7.1%, while 15-year terms may offer lower rates. Link to national rate tracker: https://www.bankrate.com/mortgages/mortgage-rates/

To understand your personal rate, use a mortgage approval estimator. It calculates your likely interest rate based on your financial profile, giving you an edge when applying for pre-approval.

Current Mortgage Interest Rates and How They Work

Your current mortgage interest rate will have the biggest impact on your monthly payments and the total cost of your loan. In Utah, the average home loan interest rate typically trends slightly below national averages, particularly for borrowers with excellent credit or those using VA and FHA loans.

Institutions like USAA home loan rates tend to offer competitive options for military families. If you already own a home, it’s worth looking into current home refinance rates to determine if you can save long-term. https://www.mortgagerateutah.com/understanding-home-loans-in-utah

Best Mortgage Loans and How to Compare Them

The best mortgage loans are the ones that align with your financial goals and homeownership plans. You’ll want to compare offers from various mortgage loan companies, whether you’re pursuing a fixed-rate loan, FHA assistance, or a VA-backed mortgage.

Use online tools or search for mortgage lenders near me to start collecting personalized quotes. The best mortgage companies typically offer a combination of competitive rates, flexible terms, and responsive customer service.

Mortgage Loan Rates Today: Why They Matter

Comparing mortgage loan rates today helps you find the most cost-effective loan. Tools like the mortgage calculator can instantly show you how small rate differences affect your monthly payment. Some calculators include fields for PMI, taxes, and homeowners insurance for a complete estimate.

Use a veteran home loan calculator if you qualify for VA benefits to see how your rate compares.

Current Fixed Mortgage Rates: Locking In Stability

A big decision when taking out a loan is choosing between a fixed or adjustable rate. Current fixed mortgage rates offer stability, and many Utah homeowners prefer to lock in rates with 30-year or 15-year terms. A fixed mortgage rates today tool can help compare offers side-by-side.

Thinking about refinancing? Try a home refinance calculator to see if you can reduce your rate or loan term.

Apply for a Mortgage with Confidence

When you’re ready to move forward, you can apply for a mortgage online. Look for a streamlined home loan application process that allows you to upload documents and track your application digitally.

Compare the best home loan interest rates from both national and local mortgage loan lenders for the most favorable terms.

Home Interest Rates Today and What Affects Them

Several factors impact home interest rates today, including your credit score, loan term, and down payment. Use a mortgage approval estimator or calculator to plan accordingly.

For live rate tracking, bookmark: https://www.mortgagenewsdaily.com/mortgage-rates

Always check interest rates now before locking your offer.

If you’re looking for current mortgage rates in Utah, you’re navigating one of the most challenging interest rate environments in over a decade. With mortgage interest rates today hovering around 6.75% to 7%, understanding today’s market can help you make informed decisions about buying or refinancing your home.

Current Mortgage Interest Rates Today

As of late June 2025, current mortgage interest rates are showing some volatility but remain elevated. Today’s average 30-year fixed-mortgage rate is 6.75%, a decrease of 7 basis points over the last seven days.

Key Rate Highlights:

30-year fixed mortgage rates: 6.75% – 6.82%

15-year fixed mortgage rates: 5.78% – 5.92%

Current home mortgage rates in Utah: 6.25% – 6.915%

Current mortgage refinance rates: 6.75% – 6.82%

The latest mortgage rates reflect ongoing economic uncertainty. By January 2025, the average rate on a 30-year fixed-rate mortgage surpassed 7% for the first time since last May.

30-Year Mortgage Rates in Utah

30-year mortgage rates remain the most popular choice for Utah homebuyers, offering predictable monthly payments. As of June 27, 2025:

30-year fixed rate mortgage: 6.25%

15-year fixed-rate loan: 5.375%

Utah’s 2025 mortgage rates typically align with national averages, but local lenders may offer competitive options for strong credit profiles.

Best Mortgage Lenders in Utah

Finding the best mortgage lenders in Utah requires comparing rates, fees, and loan programs. Options include national lenders, regional banks, and local credit unions.

Utah FHA loan requirements – Lower down payments for qualified buyers

Utah VA loan eligibility – Benefits for military veterans

Utah housing down payment assistance – Up to $30,000 in support

Utah Mortgage Calculator and Refinancing

Using a Utah mortgage calculator helps estimate monthly payments based on current fixed mortgage rates. With rates around 6.75%, sample monthly payments are:

Sample Monthly Payments (Principal + Interest):

$300,000 loan @ 6.75%: $1,946/month

$400,000 loan @ 6.75%: $2,594/month

$500,000 loan @ 6.75%: $3,243/month

You’ll pay approximately $648.60 per $100,000 borrowed at 6.75%.

Refinance Rates in Utah

Utah homeowners should closely monitor refinance rates, especially if your mortgage rate is over 7%.

Refinancing makes sense when:

Your current rate is higher than today’s

You plan to stay long-term

You have sufficient equity

You can recoup closing costs quickly

First-Time Home Buyer Programs in Utah

First-time home buyer Utah programs help buyers overcome high rates and home prices.

Available Assistance Includes:

Utah housing down payment assistance – Income-based

Utah FHA loan requirements – 3.5% down payment

Low-income home loans Utah – Specialized programs

Mortgage loans for teachers in Utah – Career-specific benefits

Home loans for nurses Utah – Healthcare worker programs

Utah Housing Market Trends

Utah’s housing market shows unique trends. Notably, 71% of mortgages have rates below 4%, leading to a strong lock-in effect.

Current Market Conditions (as of Jan 2025):

Median home price: $508,749

Average days on market: 64

Homes selling above list price: 21.6%

A rise in rates from 3% to 6% increases monthly payments by 34% – from $1,657 to $2,227.

Getting Approved: Key Questions Answered

To get approved for a mortgage in Utah:

Best credit score: 620+ for conventional loans

Average mortgage rate in Utah: 6.25% – 6.915%

Should I lock my rate today? – Yes, if rates are trending upward

Compare lenders to secure the best offer

Mortgage approval requires:

Stable income and job history

Debt-to-income (DTI) ratio below 43%

Sufficient down payment

Solid credit score

Market Timing and Strategy

The best time to buy a home in Utah is typically spring to early fall. But current conditions may shift timing.

Strategy Tips:

Focus on the right property, not perfect rate timing

Use pre-approval to strengthen offers

Consider mortgage options for self-employed

Compare 30-year rates with other term options

Conclusion

Current mortgage rates in Utah remain high historically, but prepared buyers still have options. Whether you’re a first-time buyer or refinancing, knowing your options helps.

Rates around 6.75% are reasonable by historical standards. Don’t wait for the perfect rate — focus on the right home and loan. Use a Utah mortgage calculator, compare lenders, and explore programs to make a smart purchase in today’s market.

If you’re a homeowner looking to borrow in 2025, it’s important to compare the best HELOC lenders and home equity loan options. Popular choices like Bank of America HELOC, AmeriSave HELOC, and BECU HELOC offer competitive rates and flexible terms. You can also explore fixed-rate loans such as 15 year loan rates, 30 year loan rates, or shorter options like 2 year fixed home loan rates and 5 year fixed home loan rates. Tools like a 30 year HELOC payment calculator or Bankrate HELOC comparisons can help you decide. If you prefer a one-time payout, lenders like AmeriSave and Bank of America offer home equity loans with fixed payments. Be sure to research ARM loan rates and check Bank of America home loan rates or AimLoan rates to see what fits your budget. Finally, use trusted resources to find the best HELOC rates and the best home equity lenders for your needs.

If you’re buying your first home, refinancing a current mortgage, or exploring a home equity option, understanding mortgage rates in Utah is more important than ever in 2025. Utah’s real estate market has been one of the fastest-growing in the U.S. for years, fueled by a young population, strong job growth, and an influx of remote workers. But with rising interest rates and tightening lending conditions, getting the best deal on your mortgage—or even understanding what your options are—can be challenging.

With home prices soaring, mobile homes offer an affordable alternative to apartment living. Learn how to get pre-approved for a mobile home loan in Utah today!

Introduction Navigating the real estate market in the Beehive State can be daunting, but understanding how to get a mortgage is the first real step toward homeownership. Many prospective home buyers start their journey by exploring the financial landscape of home loans —the real competitive edge comes from securing a mortgage pre-approval. This document proves…

If you are searching for an FHA loan for bad credit in 2026, you are likely also checking mortgage rates today, reviewing the mortgage rate forecast, and calculating what your real monthly payment might look like. The good news is that an FHA loan continues to be one of the most accessible mortgage options for…

Mortgage rates play a major role in determining how affordable a home is, how much buyers can borrow, and whether refinancing makes financial sense. In Utah, where population growth and housing demand remain strong, understanding current mortgage rates—and where they may be headed—is especially important for both first-time buyers and existing homeowners. This guide breaks…

This guide breaks down everything you need to know, from how to check the latest mortgage rates this week, to using a mortgage calculator Utah lenders trust, to finding the best home equity loan rates Utah residents can access.

What Are the Current Mortgage Rates in Utah?

As of early 2025, mortgage rates in Utah for a 30-year fixed loan hover between 6.5% and 7.2%, depending on your credit score, down payment, and lender. These rates may seem high compared to the ultra-low rates of 2020–2021, but they’re fairly consistent with national averages today. Meanwhile, 15-year fixed rates are slightly lower, ranging from 5.8% to 6.4%.

It’s important to note that these rates change weekly. That’s why checking mortgage rates this week is a crucial step before applying for a loan. Rates can rise or fall with inflation reports, Federal Reserve meetings, or changes in lender policies.

Exploring VA Mortgage Rates in Utah

f you’re an active-duty service member, veteran, or surviving spouse, you may qualify for a VA loan and that comes with serious advantages. VA mortgage rates in Utah are typically lower than conventional loans, and they often don’t require a down payment or private mortgage insurance (PMI). Many Utah-based lenders offer VA loans, and competition helps keep rates favorable.

For example, institutions like Mountain America Credit Union and America First Credit Union routinely advertise competitive VA mortgage rates with added benefits like low closing costs and flexible underwriting for military families.

Using Mortgage Calculators for Utah Buyers

Before you even talk to a lender, it’s smart to estimate your budget using a reliable mortgage calculator Utah residents can count on. These tools let you plug in your expected interest rate, loan term, down payment, and estimated taxes and insurance to get a preview of your monthly payments.

Some mortgage calculators go a step further by estimating your front-end and back-end debt-to-income ratios, helping you understand what banks will actually approve. Look for calculators on lender websites or platforms like Bankrate and NerdWallet.

Home Equity Options: Agreement vs. Loan

Utah homeowners sitting on built-up equity have two primary ways to access it: a home equity loan or a home equity agreement. Both have pros and cons.

A home equity loan is a traditional second mortgage with a fixed rate. Current home equity loan rates in Utah are usually between 7.0% and 8.5%, depending on the lender.

A home equity agreement, on the other hand, is a newer model. Instead of a loan, you receive cash in exchange for a percentage of your home’s future value, usually repayable in 10–30 years. Companies like Unison and Point offer this option in Utah.

Using a home equity calculator can help you understand which option may be more cost-effective based on your plans to sell or refinance in the future.

Should You Refinance Your Mortgage in 2025?

If you locked in a high rate in 2023 or 2024, you may be looking to refinance now that the market is starting to stabilize. Refinance rates in Utah have slightly improved, especially for borrowers with strong credit and home equity.

Still, it’s important to compare refinance mortgage rates and factor in closing costs. Many Utah homeowners overlook hidden fees that can eat away at their savings. Tools like a refinance calculator can help you determine your break-even point and whether refinancing makes financial sense.

Don’t Forget About Other Rate Terms

In addition to conventional loans, many lenders offer specialized rate structures:

House rates Utah – This term is often used to describe rates across different housing products, including manufactured or modular homes.

Mortgage rates this week – Always compare this week’s published rates to previous trends.

VA mortgage rates Utah – Ensure your lender is VA-approved if you qualify.

Refinance rates Utah – Rates may be lower than purchase loans depending on equity and credit

By understanding how these terms differ, you’ll be better equipped to ask the right questions when meeting with a mortgage advisor.

What Is a Mortgage, Really?

It sounds basic, but many first-time buyers still ask: what is a mortgage? A mortgage is simply a legal agreement where a lender gives you money to buy a home, and you agree to pay it back—plus interest—over time. The lender uses your home as collateral. If you fail to make payments, they can foreclose and take ownership of the property.

There are many types of mortgages: fixed-rate, adjustable-rate, government-backed (like FHA or VA), and jumbo loans. Each comes with its own eligibility requirements, rate structures, and long-term financial implications.

Final Thoughts: Be a Smart Borrower in Utah

In a competitive market like Utah, knowledge is your most powerful tool. Whether you’re using a mortgage calculator, shopping for VA mortgage rates in Utah, or comparing a home equity loan vs. a home equity agreement, being informed helps you avoid overpaying.

Start by reviewing mortgage rates in Utah this week, then explore your options using reputable lenders, online tools, and financial advisors. And don’t be afraid to ask questions—mortgages may be complex, but they don’t have to be confusing.

Next Steps:

Check weekly rates from trusted sources like Bankrate

Use a calculator from NerdWallet

Compare loan offers from local and national lenders