How Much Mortgage Can I Afford?

Buying a home starts with one essential question: how much mortgage can I afford? While many buyers begin with a mortgage calculator with taxes and PMI or a mortgage calculator with down payment, lenders evaluate so much more than a simple monthly payment estimate. Income, debt obligations, credit score, and loan structure all determine your final approval amount.

Understanding the difference between how much mortgage can I get approved for and how much mortgage can I qualify for is critical. Approval depends on verified income, employment stability, credit history, and your debt-to-income ratio for mortgage approval.

Income-Based Mortgage Affordability

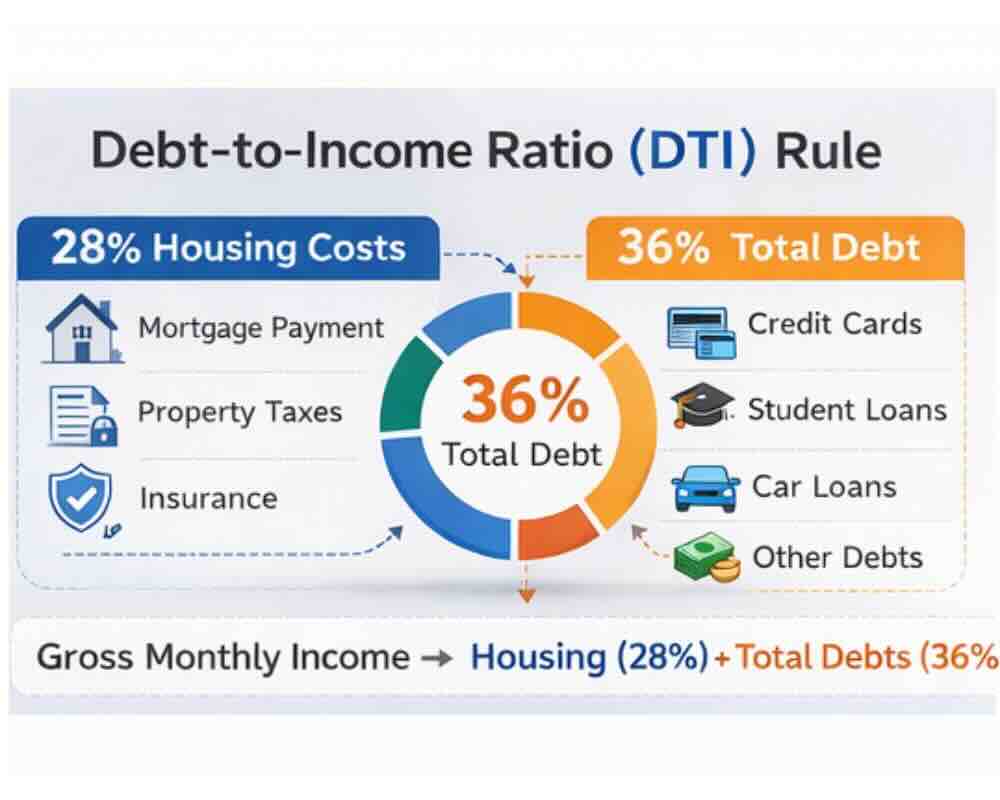

If you earn $65,000 annually, you may ask how much mortgage can I afford with 65k salary. Lenders often use the 28/36 rule, meaning no more than 28% of gross income should go toward housing and no more than 36% toward total debts.

For borrowers researching how much house can I afford 50k income, the same percentage guidelines apply, but the resulting maximum mortgage amount based on income will be lower.

Student loan debt also impacts affordability. Many buyers wonder how much house can I afford with student loans, since lenders calculate overall obligations using a mortgage affordability calculator debt to income ratio model. Some borrowers also prefer calculating conservatively and ask how much mortgage can I afford after taxes to ensure their budget remains comfortable.

Approval vs. Qualification Requirements

Lenders may require a certain minimum income for mortgage approval, but consistency of earnings often matters more than the raw number. If you are self-employed, a mortgage calculator for self-employed borrowers can help estimate potential affordability.

Those with commissions or fluctuating pay must understand how to calculate variable income for mortgage qualification. Most lenders review two years of income history to determine a stable average.

Credit Score and First-Time Buyer Considerations

Your credit profile significantly influences affordability. Securing a mortgage with 700 credit score generally provides access to competitive interest rates and better loan terms.

However, first-time buyers exploring a mortgage calculator first time buyer bad credit may see higher estimated payments due to increased risk. Lower-income households may also use a low-income mortgage calculator to determine realistic price ranges before beginning the application process.

Understanding the Full Monthly Payment

Many buyers only focus on principal and interest, but a realistic estimate requires more detail. Tools such as a mortgage calculator with insurance, mortgage calculator with HOA fees, and mortgage calculator including closing costs provide a clearer picture of total expenses.

A mortgage payment breakdown calculator separates principal, interest, taxes, insurance, and PMI. If purchasing with a partner, a dual income home loan calculator can demonstrate how combined earnings increase borrowing power.

Comparing options with a 30-year fixed mortgage calculator helps buyers understand long-term payment stability and total interest costs.

Ultimately, understanding what affects mortgage affordability ensures that you choose a loan that fits your financial goals rather than stretching to the maximum lender approval.