Shopping for current mortgage rates can feel like trying to hit a moving target, especially when national headlines, local Utah market conditions, and lender pricing all shift week to week. The truth is that “the rate” you see online is rarely the rate you actually qualify for. Your credit score, down payment, loan type, and even the property itself can change pricing. That’s why the smartest way to shop is to compare apples-to-apples loan scenarios and collect multiple mortgage interest rate quotes before making a decision.

Borrowers often start with aggregator sites like bankrate mortgage rates to see national averages, but Utah buyers and homeowners get the best results when they combine that research with personalized quotes from local lenders. Whether you’re buying your first home, looking at a VA loan, or considering a refinance, this guide explains how to interpret home loan rates of different banks, what’s driving federal reserve mortgage rates influences, and how to choose a strategy that fits your goals.

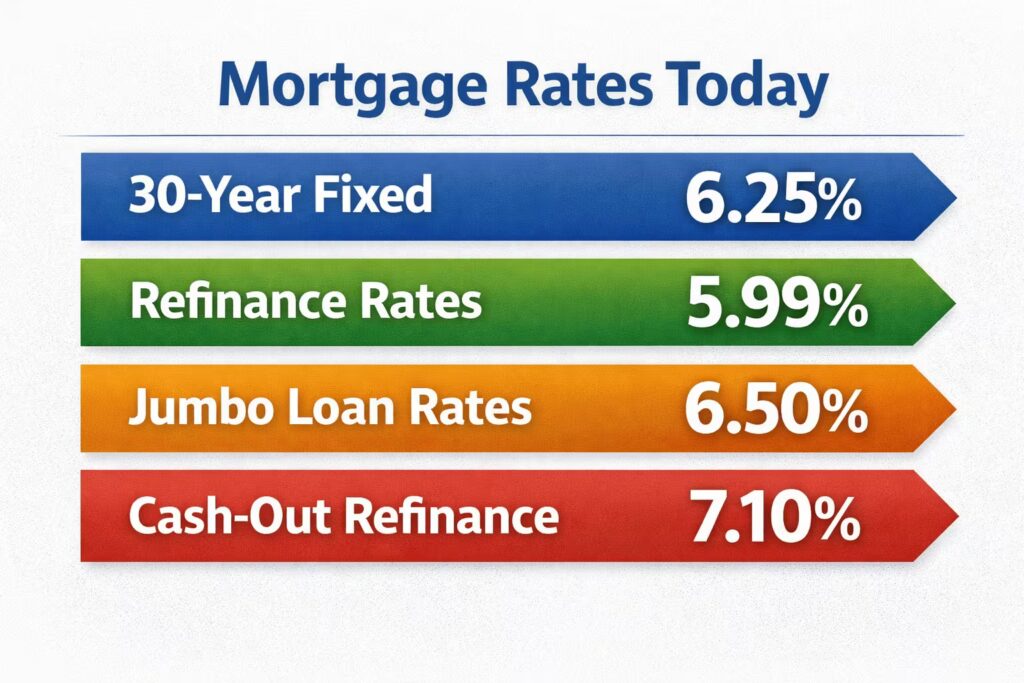

Mortgage Rates Today: 30-Year Fixed and 30 Year Mortgage Rates

For many Utah households, mortgage rates today: 30-year fixed are the default starting point because the payment stays predictable for decades. 30 year mortgage rates are typically higher than 15-year rates, but the monthly payment is lower, which can be helpful if you’re prioritizing cash flow or qualifying for a specific home price.

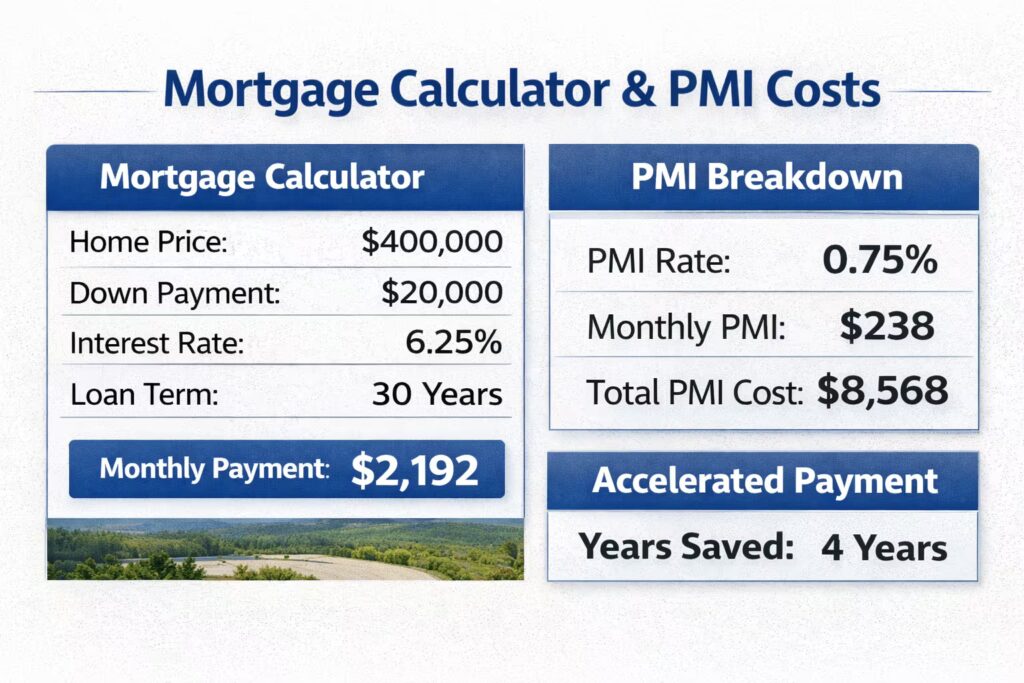

When comparing 30-year offers, don’t just look at the interest rate. Ask lenders for the full loan estimate, including points, lender fees, and required escrows. A “low” rate with expensive points can cost more than a slightly higher rate with lower fees. This is where using a mortgage interest calculator can save you from guessing: plug in the interest rate, fees, and loan amount to estimate both monthly payment and total interest paid.

Tip for Utah buyers: if you’re competing in a hot market, ask about locking options early. A lock won’t guarantee the best long-term deal, but it can protect you from short-term volatility while you’re under contract.

Refinance Mortgage Rates Today and Cash Out Refinance Rates

Homeowners watching refinance mortgage rates today usually fall into two groups: (1) those trying to lower their payment or rate, and (2) those trying to access equity. If you’re tapping equity, you’ll be comparing cash out refinance rates with second-lien products like home equity loans.

A rate-and-term refinance replaces your current mortgage with a new one designed to reduce the interest rate, shorten the term, or switch loan types. A cash-out refinance does the same, but you borrow more than you owe and receive the difference as cash, often used for renovations, debt consolidation, or major expenses.

Since cash-out loans have different risk pricing, cash out refinance rates can be higher than standard refinance pricing. Your best move is to request multiple mortgage interest rate quotes for both structures and compare them side-by-side using a mortgage interest calculator. You’re not just shopping for the lowest rate, you’re shopping for the best overall outcome.

Rocket Mortgage VA Loan Rates, Jumbo Loan Rates, and Investment Property Mortgage Rates

Not all loans are priced the same. Borrowers eligible for VA financing often look up rocket mortgage va loan rates as a reference point, but you should still compare local lenders, credit unions, and brokers for the best terms. VA loans can be extremely competitive because they typically don’t require mortgage insurance and can offer attractive pricing depending on lender overlays.

For higher-balance properties, jumbo loan rates can differ from conforming loans. Jumbo underwriting often requires stronger credit, higher reserves, and stricter debt-to-income guidelines. In exchange, some borrowers may find jumbo pricing surprisingly competitive, especially with strong borrower profiles.

If you’re buying a rental, investment property mortgage rates are usually higher than owner-occupied rates because lenders treat them as higher risk. If you’re comparing options for a rental, don’t forget to model realistic cash flow. A slightly higher rate might still be worth it if the property’s rental income and appreciation potential are strong.

Mortgage Companies With Lowest Interest Rates and Mortgage Lenders With Lowest Rates

Many people search for mortgage companies with lowest interest rates, mortgage lenders with lowest rates, or mortgage companies with best interest rates, but those phrases can be misleading without context. The “lowest rate” is often tied to a perfect borrower profile (high credit score, large down payment, low DTI, primary residence, and sometimes paying points). That doesn’t mean those rates aren’t real; it means you need to compare rates based on your actual scenario.

A practical way to compare lenders is to gather quotes from:

- A local Utah lender or broker (often competitive on service and speed)

- A bank or credit union (sometimes strong on fees)

- A large online lender (often strong on convenience)

Then compare the effective cost, not just the headline rate. If you’re trying to find mortgage companies with lowest interest rates, ask each lender to quote the same loan amount, down payment, occupancy type, and lock length. That’s the fastest way to figure out who actually offers mortgage companies with best interest rates for you.

Private Mortgage Insurance Rates, Mortgage Insurance Rate Finder, and Mortgage Pre Approval Interest Rate

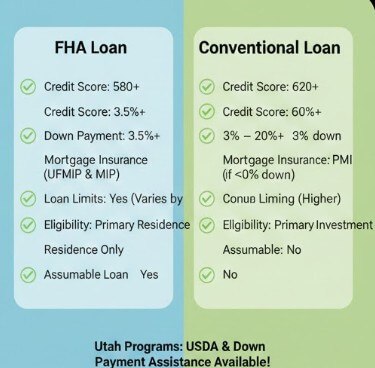

If you put down less than 20% on a conventional loan, you’ll likely pay private mortgage insurance rates (PMI). PMI is not one-size-fits-all. It’s driven by your credit score and loan-to-value ratio, and it can move your effective monthly cost more than a small rate difference.

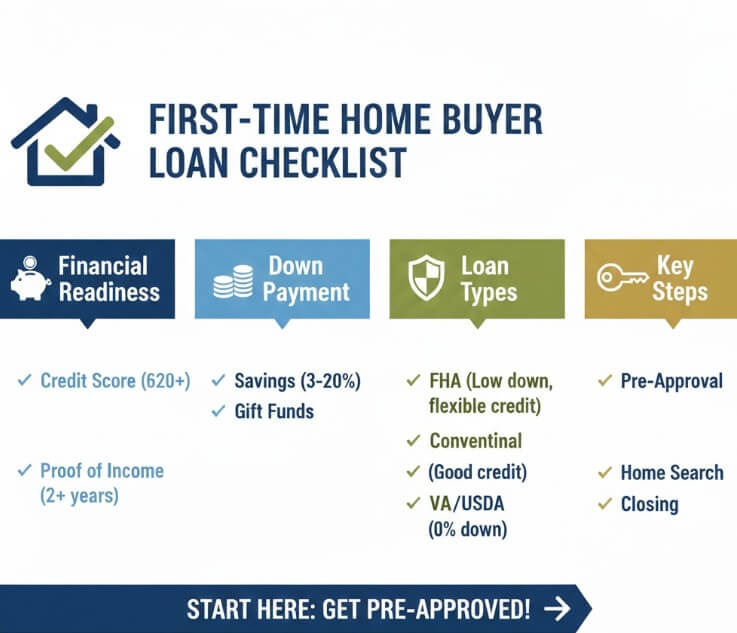

Before you lock anything in, request your mortgage pre approval interest rate so you know what you can realistically afford and what pricing tier you’re in. Many buyers skip this step and fall in love with a payment they can’t replicate once the real numbers come in.

To estimate PMI, you can use a mortgage insurance rate finder (or ask lenders to show you the PMI line item in the quote). In many cases, improving your credit score or increasing your down payment slightly can reduce PMI enough to materially change your monthly payment.

Best Interest Only Mortgages, Accelerated Mortgage Payment, and Home Equity Loan Rates

Some borrowers explore best interest only mortgages to keep payments lower during an initial period. These can be useful in specific situations, like uneven income, short-term liquidity needs, or strategic investing, but they require discipline. Once the interest-only period ends, payments can rise significantly because you start paying principal too.

On the flip side, if your goal is to pay off debt faster, an accelerated mortgage payment strategy can reduce interest and shorten your timeline. Biweekly payments or adding extra principal each month can make a noticeable difference over time, especially if you start early.

If you’re not trying to replace your first mortgage, compare home equity loan rates to refinancing. A home equity loan may let you keep your original rate while borrowing against equity separately. The best choice depends on your current rate, how much you need to borrow, and how long you plan to keep the home.

Federal Reserve Mortgage Rates and Mortgage Rates Will Go Down

A common question is whether mortgage rates will go down. While it’s impossible to predict perfectly, mortgage pricing often reacts to inflation expectations, bond markets, and signals from the Federal Reserve. People sometimes refer to federal reserve mortgage rates, but the Fed doesn’t set mortgage rates directly. Instead, its policy moves influence borrowing costs across the economy, which can flow through to mortgage pricing.

The smartest approach is to avoid trying to “time the bottom.” If the monthly payment works for your budget and the loan supports your financial goals, it can still be a good move, even if rates shift later. If rates drop meaningfully, you can evaluate refinancing at that point.

Current Mortgage Rates and 40-Year Mortgage Refinance Options

If you’re returning to the market again, remember that current mortgage rates change not only by day, but by borrower profile and loan type. And for homeowners who need payment relief, some lenders offer long-term options such as a 40-year mortgage refinance. This can reduce monthly payments by extending the loan length, though you’ll typically pay more interest over the life of the loan.

Before you choose a 40-year option, compare it against alternatives like a standard refinance, a home equity loan, or changing your payment strategy. The “best” loan isn’t always the one with the smallest monthly payment, it’s the one that matches your timeline and keeps your long-term costs reasonable.