Navigating the real estate market in the Beehive State can be daunting, but understanding how to get a mortgage is the first real step toward homeownership. Many prospective home buyers start their journey by exploring the financial landscape of home loans —the real competitive edge comes from securing a mortgage pre-approval. This document proves to sellers that a mortgage lender has already vetted your finances and is ready to back your offer.

To start the process, you should research the best mortgage companies and best mortgage lenders available in the state of Utah. Experts encourage you to get a mortgage quote from several different sources to ensure you get the best deal. While some buyers prefer large national banks, others have found that working with a local mortgage broker offers help with the local markets and a more personalized experience.

What You Need to Get Pre-Approved

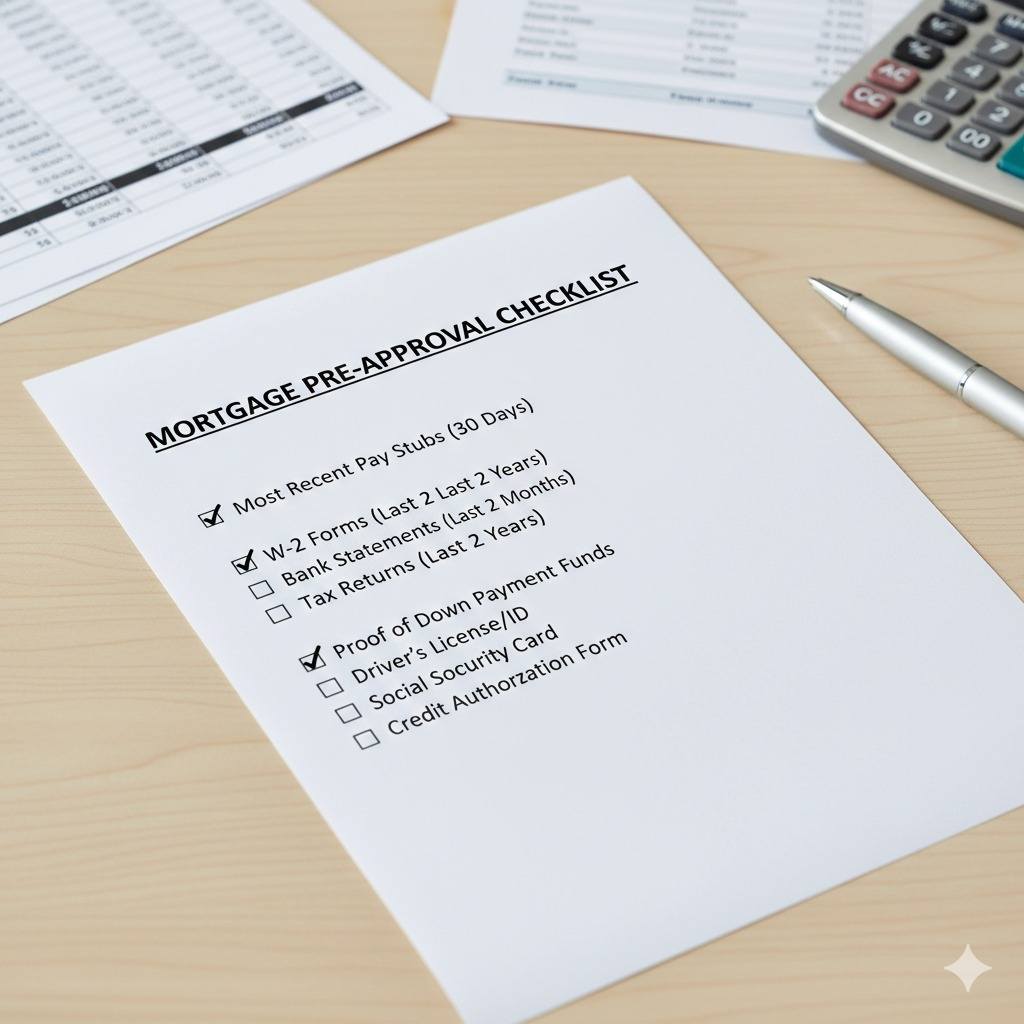

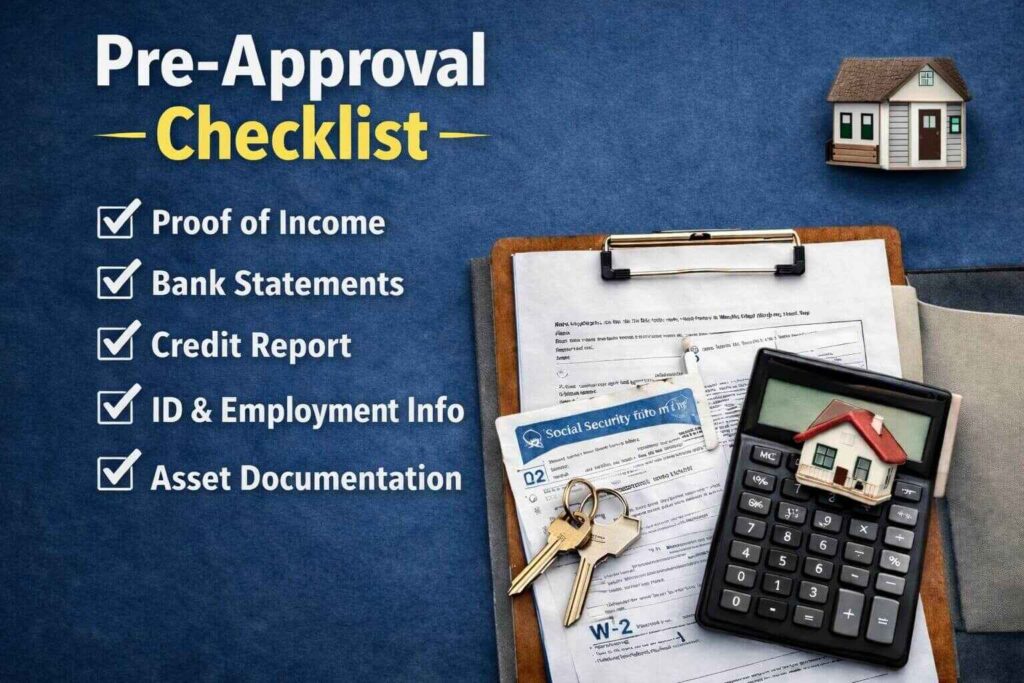

When you sit down with a professional to discuss your mortgage application, you might ask, “What will I need to get a mortgage?” Generally, you will need to provide proof of income (such as W-2s and tax returns) and evidence of assets for a down payment. Knowing specifically what you need for pre-approval saves time and stops the underwriting process from stalling.

Once you have gathered your documents, the next question is timing. When should I apply for the mortgage loan paperwork? Ideally, this should happen before you even set foot in an open house. When should a lender pre-approve my mortgage loan? Most experts recommend getting your letter 3 to 6 months before you intend to buy. This gives you time to fix any credit issues that might arise during the steps to buying a house. When should you get a mortgage pre-approval? As soon as you are serious about entering the market.

Understanding Home Loan Interest Rates and Programs

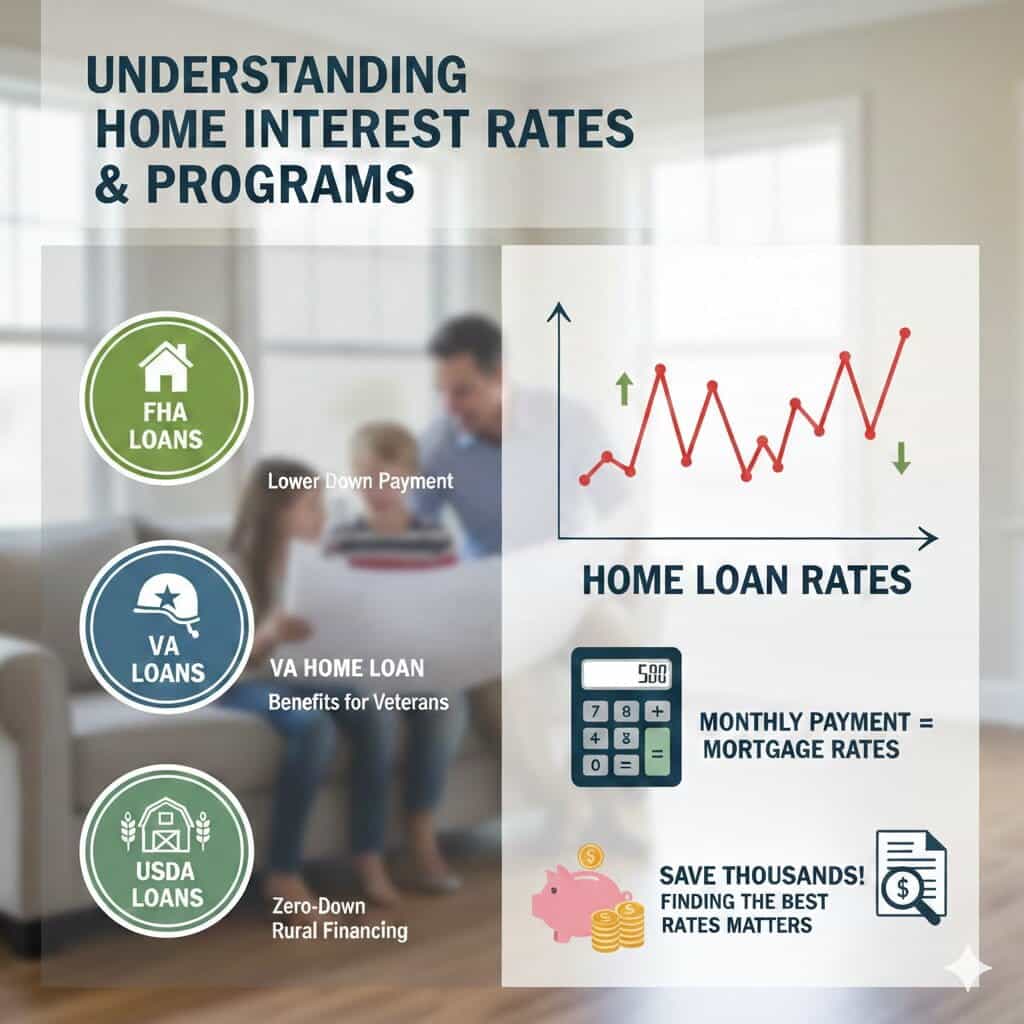

Your choice depends on your financial situation and specific program requirements. For many, FHA loans are an excellent entry point because they offer lower down payment options. Veterans should always look into a VA home loan, which provides significant benefits for those who have served. In more rural Utah communities, USDA loans are another powerful tool for zero-down financing.

Regardless of the program, current mortgage rates and home loan interest rates dictate your monthly payment. It pays to be diligent; finding the best mortgage or home loan rates can save you thousands of dollars over the lifetime of your loan. Keep a close eye on home loan rates, as they fluctuate with market conditions.

Finalizing Your Mortgage Pre-Approval in Utah

It is important to understand the difference between securing a home loan approval and obtaining a prequalification for a home. A pre-qualification is a surface-level look at your debt, while a pre-approval is a deep dive into your credit score. Most sellers in Utah will not even look at an offer without a formal pre-approval letter. As you finalize your plans, continue to monitor current mortgage rates and stay in close contact with your lender. Following these steps will position you to secure your dream home. Whether comparing lenders or quotes, preparation is the key to success.

Navigating the 2026 real estate market requires more than just a passing interest in home listings; it requires a fortified financial strategy. As home prices remain steady and inventory remains a challenge, the first step for any serious buyer is understanding the difference between mortgage prequalification vs preapproval. While a prequalification gives you a ballpark estimate of your buying power based on self-reported data, a preapproval is a rigorous, verified commitment from a lender that carries significant weight when you finally make an offer.

How Much House Can I Afford ?

Determining your budget is the cornerstone of a successful home search. To truly answer the question, “how much house can I afford,” you must look beyond the sticker price and evaluate your monthly cash flow. In 2026, lenders are scrutinizing mortgage income requirements more closely than ever, typically looking for a debt-to-income (DTI) ratio that ensures your total monthly obligations, including your future mortgage, stay within a manageable range.

When running these numbers, many buyers forget to include the mortgage insurance cost, which is a mandatory fee for those putting down less than 20% on a conventional loan or using an FHA product. Furthermore, you must determine exactly how much do I need for a down payment to reach your desired price point. While traditional advice suggests 20%, modern FHA down payment requirements allow buyers to enter the market with as little as 3.5% down, making homeownership accessible even as savings are stretched.

First Time Home Buyer Programs

The path to your first front door is often paved with financial assistance. There are numerous first time home buyer programs available in 2026 designed to lower the barrier to entry for new market participants. These programs often provide a combination of low-interest loans and first time home buyer grants that do not require repayment, provided the buyer remains in the home for a specified period.

Because real estate trends are highly localized, you should also investigate home buyer grants [state-specific] that may offer additional tax credits or cash assistance for down payments. Many buyers find that they can “stack” these benefits with down payment assistance programs and closing cost assistance to significantly reduce the out-of-pocket expenses required at the signing table. Taking the time to research these options before you start touring homes can add tens of thousands of dollars to your effective budget.

How to Improve Credit to Buy a House

Your credit score is the single most important factor in determining your interest rate and loan eligibility. If you find your score is below the minimum credit score for mortgage approval, typically 620 for conventional loans or 580 for FHA, you must prioritize how to improve credit to buy a house. This process includes paying down high-interest credit card debt, ensuring all utility bills are paid on time, and avoiding any new large purchases or credit inquiries in the months leading up to your application.

Once your credit is in a healthy range, you can explore more specialized financing options. For example, if you are looking at properties in less populated areas, a USDA rural development loan offers a 0% down payment option for eligible borrowers. For those with an Individual Taxpayer Identification Number, an ITIN home loan provides a vital alternative to traditional Social Security-based financing. If your dream home is a fixer-upper, the fha 203k loan allows you to bundle renovation costs directly into your mortgage, though you should be prepared for the fact that this specific, “how long does mortgage approval take” question often results in a 45-to-60-day timeline due to the extra inspections required.

Navigating Specific Loan Requirements

Different properties come with vastly different financial hurdles. If you are eyeing a luxury property, you must meet the stringent jumbo loan requirements, which often include higher cash reserves and credit scores. Conversely, those interested in a more affordable entry point might investigate a manufactured home loan, though these require the home to be permanently affixed to a foundation to qualify for traditional real estate rates.

Condo living offers its own set of challenges, as condo financing requirements demand that the homeowner association (HOA) maintains adequate insurance and financial reserves. Regardless of the property type, your lender will conduct a thorough audit of your finances to ensure you meet all mortgage income requirements. Understanding these nuances early in the process, before the clock starts ticking on a purchase agreement, is the difference between a smooth closing and a failed deal.

If you’re shopping for a home in Utah, the best way to reduce stress (and write a stronger offer) is to get your financing ready before you fall in love with a listing. A real pre-approval helps you understand your budget, speeds up the offer process, and shows sellers you’re serious. This guide walks you through the process, the documents you’ll need, and how options like FHA, VA, and online applications fit in—so you can move quickly and confidently.

Mortgage Pre Approval Utah: What It Is and Why It Matters

Mortgage pre approval Utah means a lender has reviewed your financial information—typically income, assets, debts, and credit—and is willing to pre-approve you up to a certain loan amount (assuming nothing major changes before closing). This is different from a rough estimate because it’s based on documentation, not just a conversation. In many Utah markets, sellers and agents expect buyers to have a pre-approval letter ready, and it can make your offer feel safer and more credible.

If your main goal is to get pre approved Utah, start early. Even if you’re “just looking,” pre-approval gives you a realistic price range and helps you avoid wasting time on homes that don’t match your true buying power. It also gives you a chance to fix issues (like paperwork gaps or a debt-to-income problem) before you’re under pressure.

Home Loan Pre Approval vs. Pre-Qualification: Which One Do You Need?

Some buyers begin by trying to <strong>prequalify for home loan</strong> because it’s fast and low-commitment. Pre-qualification is usually an informal estimate based on what you report (income, debts, and general credit range). It can be helpful early on, and it’s why so many people search how to get prequalified for a home loan when they’re still exploring options.

But if you want to write offers, a home loan pre-approval is the stronger step because it involves verification. When you get pre-approved for a mortgage, the lender checks documents and runs credit, so the letter actually means something to sellers. If you’re serious about buying soon, you’ll typically want to move beyond pre-qualification and get pre-approved for a home loan before you start making big decisions.

Some buyers begin by trying to prequalify for home loan because it’s fast and low-commitment. Pre-qualification is usually an informal estimate based on what you report (income, debts, and general credit range). It can be helpful early on, and it’s why so many people search how to get prequalified for a home loan when they’re still exploring options.

But if you want to write offers, a home loan pre-approval is the stronger step because it involves verification. When you get pre-approved for a mortgage, the lender checks documents and runs credit, so the letter actually means something to sellers. If you’re serious about buying soon, you’ll typically want to move beyond pre-qualification and get pre-approved for a home loan before you start making big decisions.

How to Get Pre-Approved for a Home Loan in 5 Practical Steps

If you’ve been wondering how to get pre-approved for a home loan, this is the most straightforward path that works for most borrowers:

Pick a lender and complete the application

Upload your financial documents (income, assets, debts)

Authorize a credit check

Review loan options and confirm your comfortable payment range

Receive your letter and keep your finances stable while you shop

That process is also what people mean when they ask how to get preapproval for a home loan—the goal is a written letter you can use when making offers. You’ll often see similar phrases like mortgage loan pre approval and house loan pre approval; they’re different wording for the same milestone: you’ve been reviewed and are ready to buy within a certain range.

If you’re asking how I can get pre-approved for a home loan as quickly as possible, the #1 tip is to respond fast when the lender requests clarification (like a missing page of a bank statement, proof of employment, or explanation for a deposit). Delays usually happen when documents are incomplete or unclear.

What Is Needed to Get Pre Approved for a Mortgage: Your Document Checklist

People commonly ask what is needed to get pre-approved for a mortgage because they don’t want surprises. While lenders vary, you can usually prepare for these categories:

Identity verification (ID)

Proof of income (pay stubs, W-2s, or tax returns if self-employed)

Proof of assets (bank statements, retirement accounts, gift funds documentation if used)

Employment history details

A list of monthly debts (auto loans, student loans, credit cards)

Credit authorization (so the lender can review score and history)

This checklist is also what helps when you’re asking how to get pre-approved for a home mortgage—you’re proving you can repay the loan, and you have funds to complete the purchase.

If your question is more specific—like how to get pre-approved for a house or how to get pre-approved for a house loan—the same checklist applies. The “house” part just means you’re using the approval to shop for a property; the lender still evaluates the borrower the same way.

FHA and VA Options: FHA Loan Pre Approval and VA Home Loan Pre Approval

Your loan program can affect details (like down payment rules and documentation), but the structure of approval stays similar.

For FHA borrowers, FHA loan pre-approval is typically focused on verifying income, assets, and credit—then pairing you with FHA guidelines. You’ll also see the shorter phrase fha pre approval used interchangeably. FHA can be a fit for some buyers because it’s designed to widen access to homeownership, but it still requires careful documentation and underwriting.

For eligible military buyers, va home loan pre-approval can be a major advantage. You may also see va mortgage pre-approval used for the same concept. VA loans often require that you confirm your eligibility (commonly through a Certificate of Eligibility) and meet lender standards for credit, income, and occupancy.

Online Speed: Online Mortgage Pre Approval and How It Works

If convenience matters, <strong>online mortgage pre approval</strong> can reduce friction because you can upload documents through a secure portal, sign disclosures digitally, and track your progress without playing phone tag. Online doesn’t mean “less real”—your lender still verifies your financial profile. The benefit is speed and organization, especially if you’re juggling work, school, or moving timelines.

Many buyers start with an estimate and prequalify for a mortgage loan online first, then transition into full approval once they’re ready. If your goal is to move from “planning” to “offer-ready,” ask the lender what they need to convert a pre-qual into a full approval letter.

FAQ: The Most Common “How-To” Questions (Answered Clearly)

Q: How to get pre-approved for a mortgage loan? A: Apply, submit documents, authorize credit, and respond quickly to lender follow-ups. This is the cleanest path to a usable pre-approval letter.</p>

Q: Get pre-approved for a home mortgage (what should I do right now?) A: Gather your pay stubs/tax returns, bank statements, and debt info first—then apply. Being organized speeds everything up.</p>

Q: How to get preapproval for a mortgage if my credit needs work? A: A lender can often tell you what’s holding you back (high balances, recent late payments, or too much debt) and what to change before you reapply.

Q: Get pre approved for a mortgage and keep it valid A: Avoid opening new credit lines, making large unexplained deposits, or changing jobs during the process. Those things can trigger re-verification.