Mortgage loan pre approval: what it is and why it matters

Mortgage pre approval is the stage where a lender verifies your income, credit, assets, and debts and then issues a letter showing what you can afford. A mortgage loan pre approval gives you a clear price range before you tour homes and signals to sellers that you are a serious buyer. If you are comparing options, keep in mind that a house loan pre approval is simply another way people describe the same step: confirming you qualify before you commit to a purchase.

Mortgage loan pre approval estimate and mortgage pre approval estimate

A mortgage loan pre approval estimate is the lender’s best calculation of what you can borrow based on the documents you provide. You may also hear this called a mortgage pre approval estimate. Either way, it helps you avoid guessing and reduces the risk of shopping above your budget. If you want to tighten the estimate, update your application with the most current paystubs and bank statements and confirm how your lender is counting income (especially bonuses, commissions, or self-employment).

Home loan pre approval calculator: quick planning before you apply

Before you submit paperwork, a home loan pre approval calculator can help you understand what monthly payments might look like at different price points. Many buyers also use a mortgage pre approval calculator to sanity-check their numbers before speaking with a loan officer. These tools are helpful for planning, but the lender’s underwriter will still confirm everything during the mortgage pre approval process.

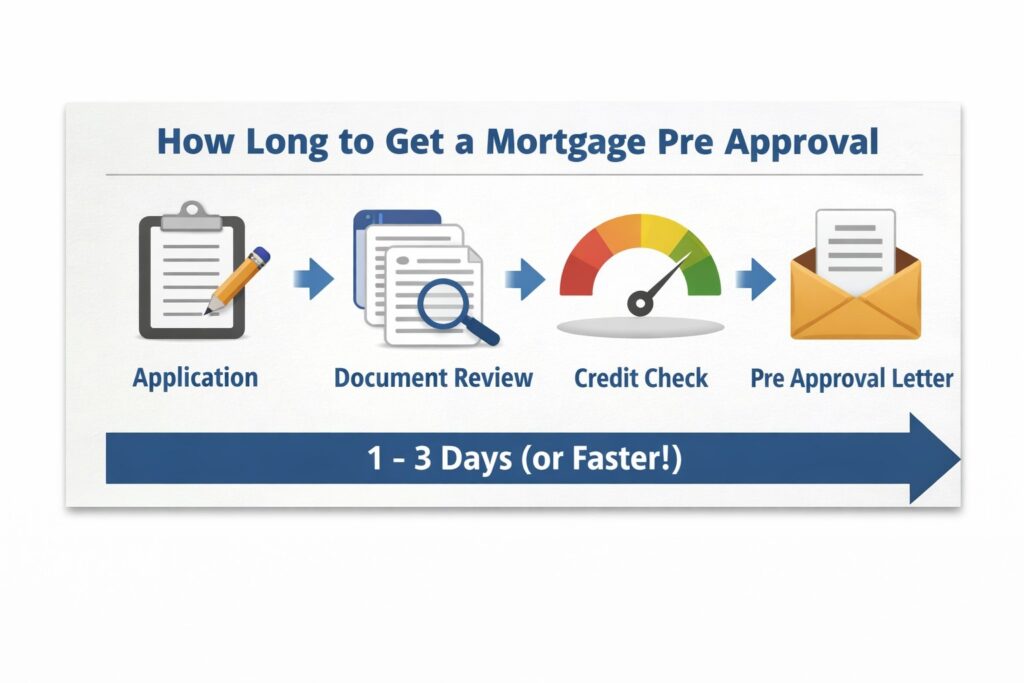

Mortgage pre approval process: from application to letter

The mortgage pre approval process usually follows four steps: (1) application, (2) document review, (3) credit pull, and (4) pre approval letter. The home loan pre approval process is similar across most lenders, but timelines vary based on how quickly you can upload documents and whether your income is straightforward. The goal is to move smoothly from pre approval to approval for mortgage after you have a signed purchase contract and the home is appraised.

How long to get a mortgage pre approval and ways to speed it up

How long to get a mortgage pre approval depends on your documentation and the lender’s workflow. If you have your files ready, some lenders can offer fast mortgage pre approval, and in certain cases you may even see same day mortgage pre approval. If you choose online mortgage pre approval, you can often upload items immediately and reduce back-and-forth delays.

Program-specific approvals: USDA, FHA, and VA

Different loan programs have different requirements. USDA pre approval may include income limits and property eligibility rules. FHA mortgage pre approval is often more flexible on credit history, but you will still need stable income and documentation. VA mortgage pre approval requires proof of military eligibility (a COE) plus standard underwriting items. If you are leaning into FHA specifically, FHA home loan pre approval can be a good path for first-time buyers, while VA options may offer competitive terms for qualifying service members.

Choosing a lender: why brand searches are different intent

Some searchers look for a specific institution, such as freedom mortgage pre approval, huntington bank pre approval, ally pre approval, nfcu mortgage pre approval, chase bank mortgage pre approval, bank of america pre approval mortgage, or chase bank home loan pre approval. Those terms signal brand-specific intent. If you are not tied to one lender yet, focus on comparing overall requirements, responsiveness, and pricing so you can choose the best fit for your situation.

Next steps

Once you have your pre approval letter, keep your financial picture stable: avoid opening new credit, avoid large unverified deposits, and respond quickly to documentation requests. When you are ready, you can get pre approved for a mortgage and move into home shopping with confidence.

{kind=link}