Mortgage Pre Approval Checklist: The Smart Way to Get Approved

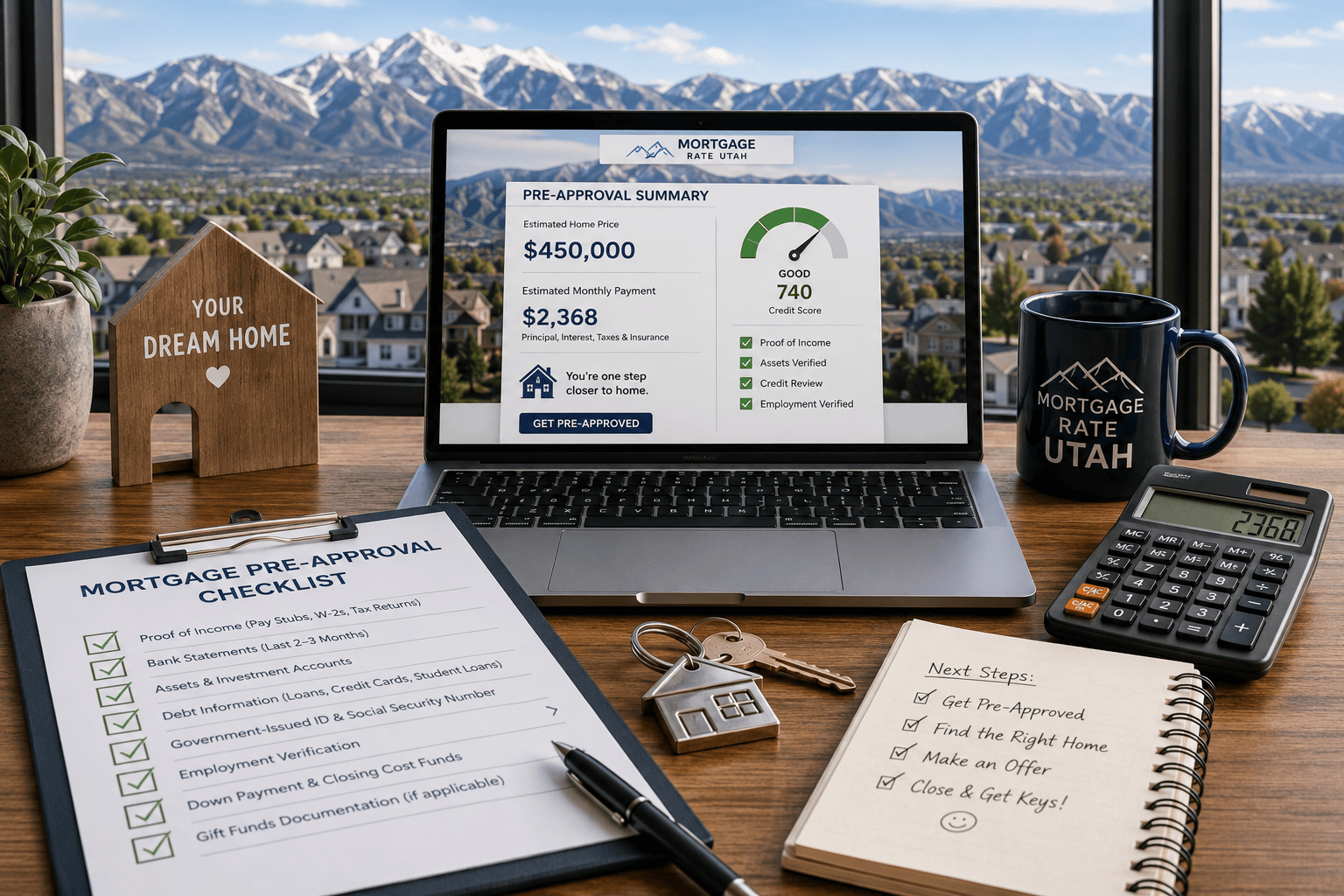

Mortgage Pre Approval Checklist: Everything You Need Before Applying Getting ready to buy a home is exciting, but it can also feel overwhelming if you …

Mortgage Pre Approval Checklist: Everything You Need Before Applying Getting ready to buy a home is exciting, but it can also feel overwhelming if you …

Estimate Monthly Payments the Smart Way with a Utah Mortgage Calculator A Utah mortgage calculator is one of the most important tools in your homebuying …

Mortgage Myths Debunked: What Every Utah Homebuyer Should Know Buying a home can feel like a daunting task, especially with some common misconceptions that can …

Utah Mortgage Guide Buying Your First Home in Utah Buying a home for the first time is an exciting yet complex journey, especially when it …