Locking in the best mortgage rate isn’t just about numbers—it’s about maximizing your long-term savings and securing the home you want on your terms. Whether you’re a first-time buyer, planning a refinance, or tapping into your home’s equity, understanding how to lock in the best mortgage rate today can save you thousands of dollars over the life of your loan.

In this guide, we’ll break down what impacts mortgage rates, how to prepare your finances, and the exact steps you need to take to secure the lowest rate possible.

What Does It Mean to Lock In a Mortgage Rate?

A mortgage rate lock guarantees the interest rate on your loan for a specific period—usually 30 to 60 days—while you finalize your mortgage. This protects you from rising rates during the application and approval process. Locking in at the right time can literally make the difference of tens of thousands of dollars over the life of your loan.

Learn more about rate locks at Investopedia

Step 1: Compare Lenders and Get Quotes

Mortgage rates vary significantly from one lender to another. Use a trusted platform like LendingTree to compare current mortgage offers across top lenders. Don’t just settle for advertised rates—get personalized quotes that match your credit profile, income, and loan goals.

Look for lenders with good reviews, competitive fees, and flexible rate-lock options.

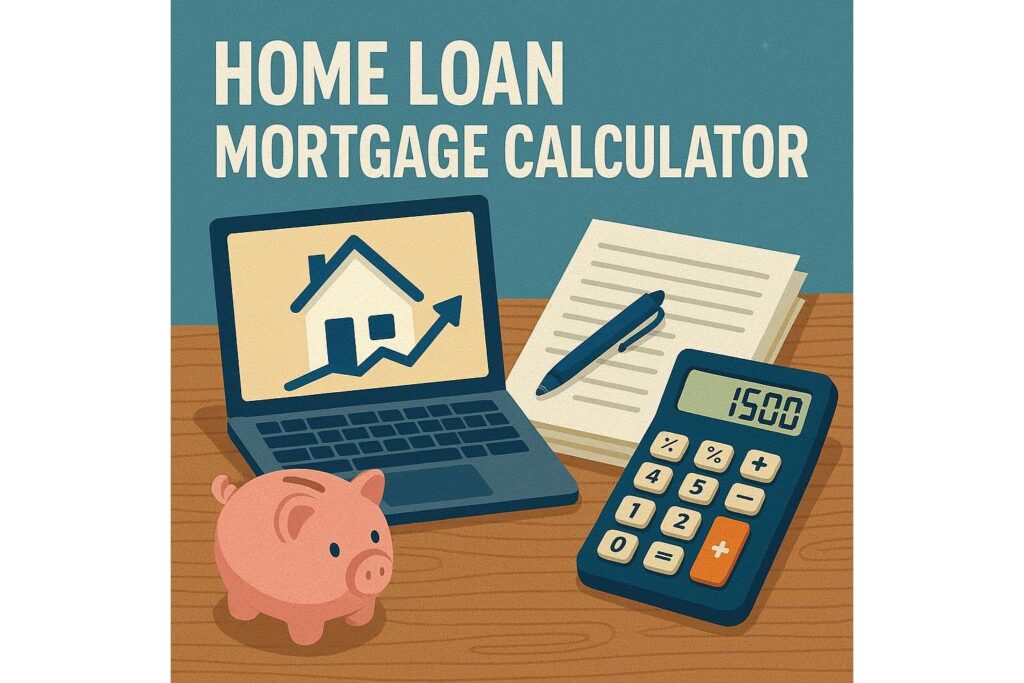

Step 2: Use a Mortgage Calculator

Before choosing a loan, use a reliable calculator like NerdWallet’s Mortgage Calculator to estimate your monthly payments. Enter your expected rate, loan amount, and loan term to preview your budget. If you qualify for a VA loan, try the VA loan calculator from Veterans United.

Understanding your affordability upfront puts you in a stronger negotiating position.

Step 3: Get Pre-Approved

A pre-approval letter from your lender shows sellers you’re serious and lets you lock in today’s best mortgage rate. Most lenders offer fast online pre-approvals that give you a solid idea of your borrowing power.

Start the process early so you can move quickly once you find the right home.

Step 4: Time Your Rate Lock

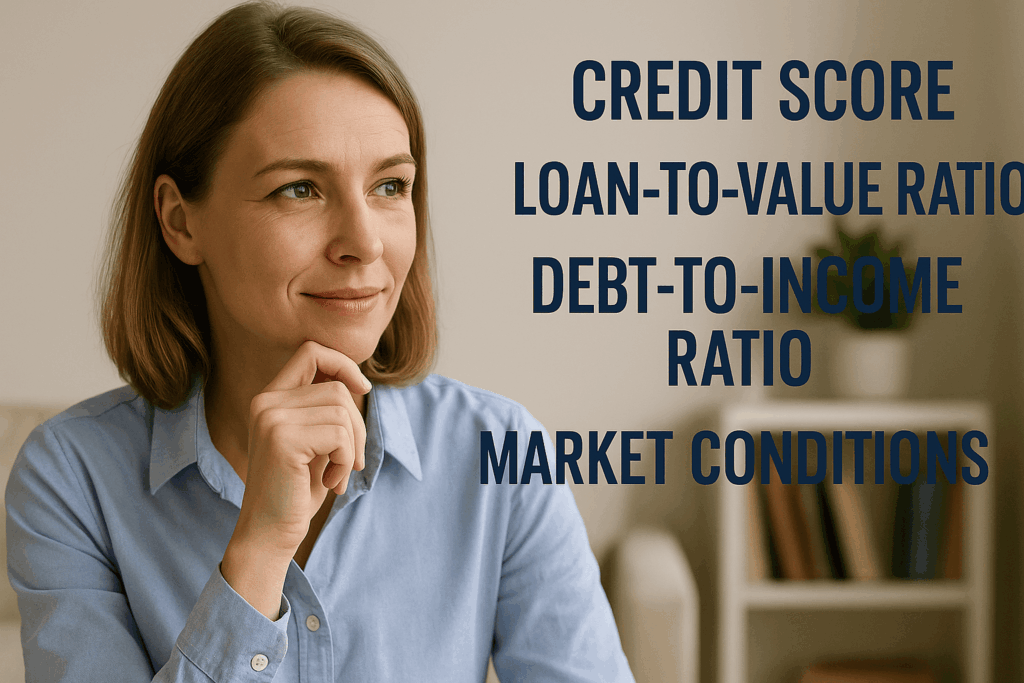

Mortgage rates fluctuate based on economic trends, inflation, and Federal Reserve decisions. Monitor real-time data from sources like Bankrate’s Mortgage Rates Tracker and consider locking your rate when market conditions are favorable.

Tip: If rates are trending up, locking sooner is usually better. If they’re dropping, you may benefit from waiting—but talk to your lender about their float-down options.

Step 5: Choose the Right Loan Product

Conventional, FHA, and VA loans all offer different rate structures. Depending on your situation, one loan type may offer a better rate or lower fees. Talk with your loan officer about which option aligns best with your goals.

If you already own a home, refinancing can also help you secure a lower rate and save over time. Visit Rocket Mortgage’s Refinance Center to explore options.

Smart Next Steps for Savvy Homebuyers

💡 Explore Refinancing: Learn about options at Rocket Mortgage: https://www.rocketmortgage.com/refinance

📊 Try a Mortgage Calculator: Estimate monthly payments with NerdWallet’s calculator: https://www.nerdwallet.com/mortgages/mortgage-calculator

🔍 Compare Lenders: Shop rates and offers using LendingTree: https://www.lendingtree.com/mortgage/rates/

Final Thoughts

Securing your ideal mortgage rate isn’t about luck—it’s about strategy. By comparing lenders, using calculators, watching market trends, and acting decisively, you can lock in the best mortgage rate today and save thousands.

Whether you’re buying your first home or refinancing, take control of your financing journey. Start with the tools and tips in this guide to make confident, informed decisions.