Mortgage Pre Approval Checklist: The Smart Way to Get Approved

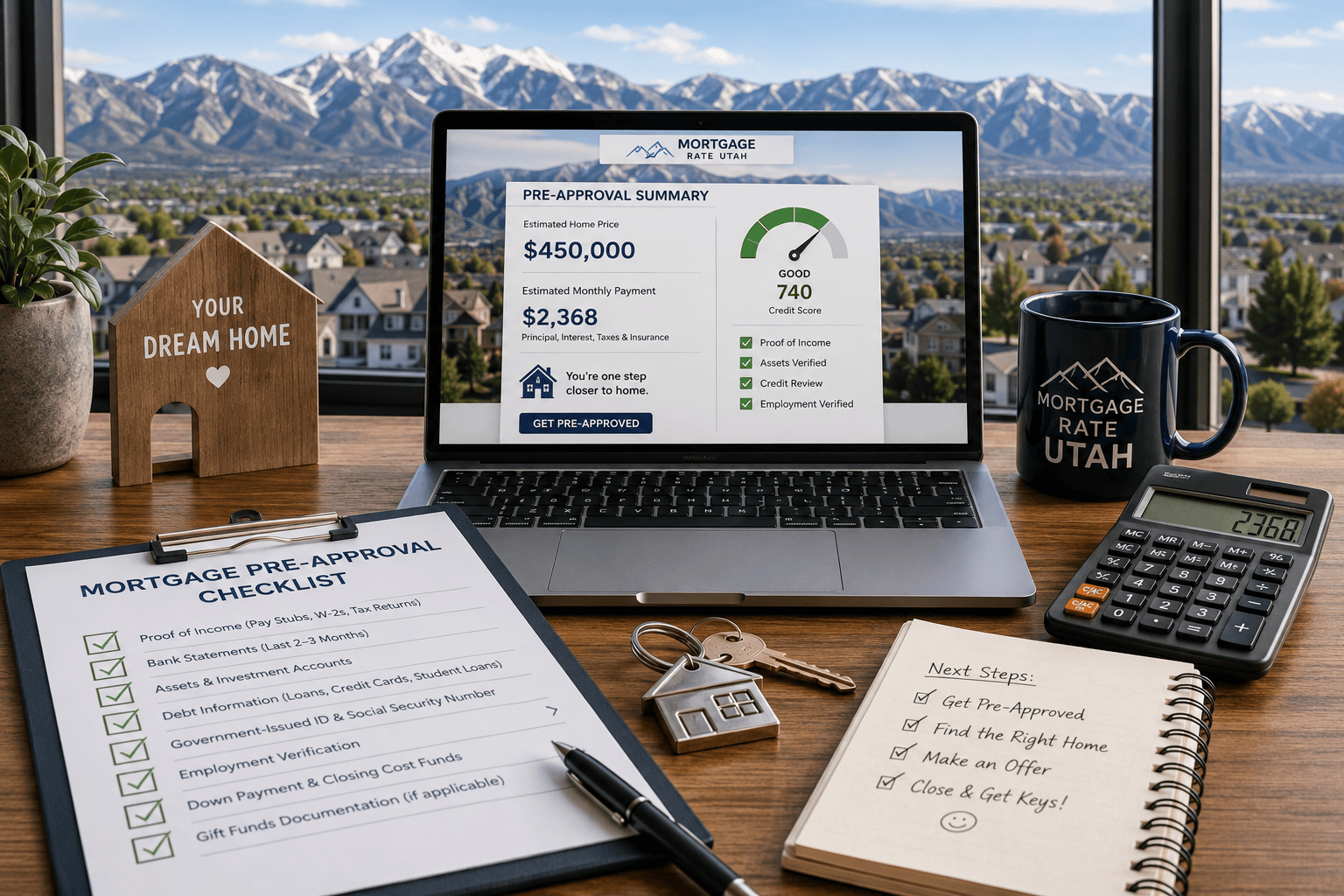

Mortgage Pre Approval Checklist: Everything You Need Before Applying Getting ready to buy a home is exciting, but it can also feel overwhelming if you …

Mortgage Pre Approval Checklist: Everything You Need Before Applying Getting ready to buy a home is exciting, but it can also feel overwhelming if you …

Navigating the 2026 real estate market requires more than just a passing interest in home listings; it requires a fortified financial strategy. As home prices …

Mortgage Myths Debunked: What Every Utah Homebuyer Should Know Buying a home can feel like a daunting task, especially with some common misconceptions that can …

Looking to expand your knowledge of banking? Here’s what you need to know when getting started.