Securing a home loan can feel overwhelming when your credit isn’t perfect, especially if you’re dealing with low scores, limited credit history, or past financial setbacks. The good news? Many borrowers successfully obtain financing even with credit hurdles. This guide brings together the most common scenarios homebuyers face so you can better understand your options—whether you’re seeking a mortgage with 580 credit score, a mortgage with 600 credit score, a mortgage with 620 credit score, or even a mortgage with bad credit.

In fact, lenders today offer a number of alternative programs designed to help borrowers re-enter the housing market, rebuild after financial hardship, or buy their first home despite a minimal credit footprint. With the right approach, education, and strategy, you can position yourself for mortgage approval sooner than you think.

Understanding Credit Thresholds and Low-Score Mortgage Options

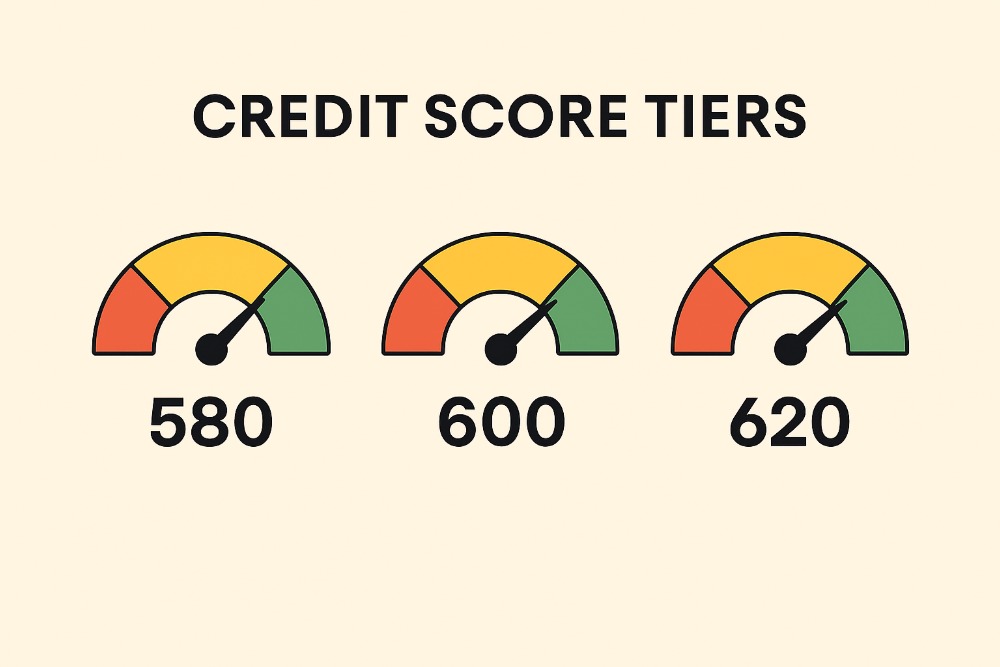

One of the most common concerns among buyers is qualifying for a mortgage with 580 credit score. FHA financing is the most widely accessible option for this scenario, as FHA guidelines typically allow borrowers to purchase a home with a 3.5% down payment when they have at least a 580 FICO. Similarly, a mortgage with 600 credit score often opens the door to even more lender flexibility, and a mortgage with 620 credit score is often considered the threshold where conventional financing becomes attainable.

These milestones matter because lenders classify credit tiers differently. While a mortgage with bad credit may sound discouraging, the truth is that many programs were created specifically to help borrowers with credit scores under 620. Additionally, if your credit is considered “fair,” working toward a mortgage with fair credit can still provide competitive opportunities. Each increase in score—even by 20 points—can significantly improve loan terms, which is why steady improvements often result in better approval odds and lower interest rates.

Getting a Mortgage With Limited, No, or Alternative Credit History

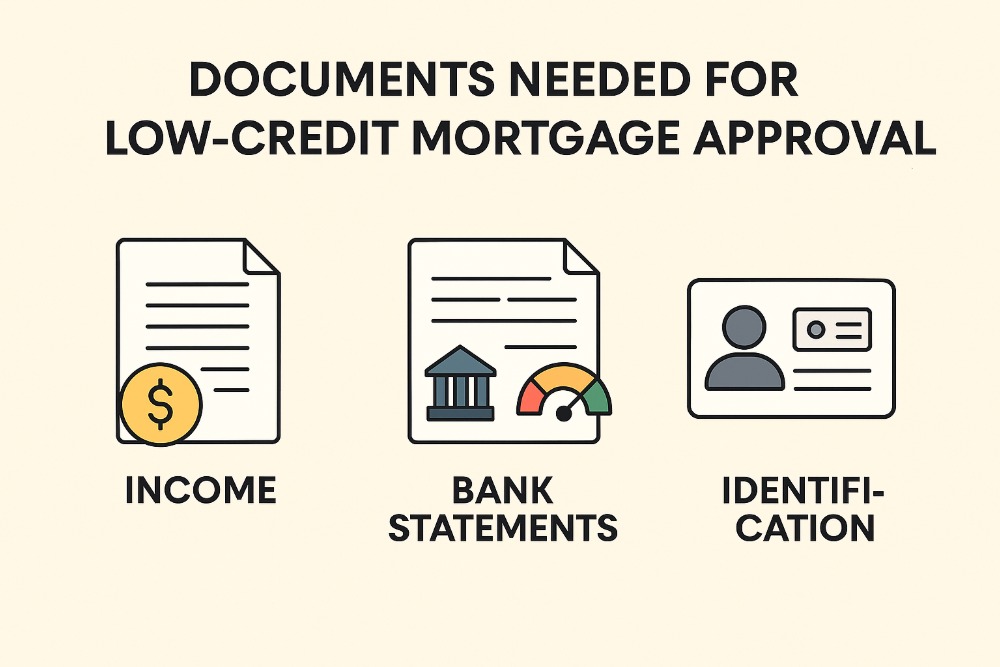

Not everyone has an established credit profile, and that’s okay. Programs exist for those needing a mortgage without credit history, a mortgage with limited credit history, or even a mortgage with no fico score. In these cases, lenders may rely on alternative credit sources such as rental payments, utility accounts, or insurance premiums to evaluate payment reliability.

You may also see terms like mortgage without established credit or first time buyer mortgage no credit, both describing scenarios where a traditional credit report doesn’t reflect the borrower’s financial responsibility. Lenders familiar with manual underwriting often serve these buyers by reviewing consistent payment histories outside of standard credit reporting.

If you’re a first-time homebuyer who hasn’t used credit much—either by choice or circumstance—don’t assume that purchasing a home is out of reach. These programs were built with you in mind.

Navigating Mortgages After Bankruptcy, Foreclosure, or Credit Setbacks

Life happens, and financial challenges such as bankruptcy or foreclosure can temporarily disrupt your ability to qualify for a mortgage. Fortunately, many borrowers successfully obtain financing again once they meet the required waiting periods and demonstrate financial recovery.

A mortgage after bankruptcy is possible through several paths. Borrowers can pursue a mortgage after chapter 7 or a mortgage after chapter 13, depending on their filing type. The waiting periods differ, but many loan programs—including FHA, VA, and sometimes USDA—allow buyers to qualify sooner than conventional loans.

Similarly, if you’ve experienced a foreclosure, you may seek a mortgage after foreclosure. While foreclosure often carries a longer waiting period than bankruptcy, it does not permanently prevent homeownership. Lenders evaluate how you rebuilt your financial profile since that event and whether your current situation supports stable repayment.

Borrowers sometimes face other challenges like late payments or default history. If this sounds familiar, you may need guidance on obtaining a mortgage after missed payments or a mortgage after late mortgage payments. Many buyers also seek approval for a mortgage with recent credit issues, which could include anything from charge‑offs to collection accounts.

Mortgages When You Have Collections, High Debt, or Disputes

Some scenarios involve more complex credit reports. For example, securing a mortgage approval with collections varies by loan type. FHA may permit approval with certain types of collections, while conventional financing may require the accounts to be resolved or addressed through payment plans. Every lender views collections differently, which is why shopping around can make a major difference.

If your debt load is high, a mortgage with high debt to income ratio may still be possible. FHA and VA loans tend to accommodate higher DTI ratios than conventional loans, making them more accessible for borrowers with strong income but higher monthly obligations.

Another roadblock buyers encounter is dealing with active disputes on their credit reports. A mortgage with credit disputes or a mortgage with disputed accounts can delay underwriting since many lenders require disputes to be removed or resolved before final approval. Addressing these issues early in the application process ensures a smoother path to closing.

Finding the Right Lenders for Challenging Credit Situations

A significant part of achieving mortgage approval lies in choosing the right lender—one familiar with working with imperfect or unusual credit histories. Searching for low credit score mortgage lenders or mortgage lenders for bad credit can help you find professionals comfortable evaluating non‑traditional financial profiles.

Some lenders specialize in FHA loans, others in VA or non‑QM (non‑qualified mortgage) programs, and others work specifically with first‑time or credit‑challenged borrowers. The key is identifying lenders who evaluate your full financial picture rather than denying applications based solely on score thresholds.

Conclusion

No matter your credit situation—whether you’re seeking a mortgage with 580 credit score, working on rebuilding after bankruptcy, needing a mortgage with no fico score, or searching for help after recent credit issues—you have more options than you may realize. Countless borrowers obtain mortgages every year with less‑than‑perfect credit, and with the right preparation, lender selection, and strategy, you can too.