If you’re monitoring mortgage rates today in Utah, you’re likely trying to understand how current mortgage rates impact what you can afford. In Utah’s fast-moving housing market, even small shifts in home loan interest rates today can significantly change your monthly payment and long-term buying power.

Whether you’re purchasing a home in Salt Lake City or refinancing elsewhere in Utah, understanding how rates work — and how they affect your budget — is essential.

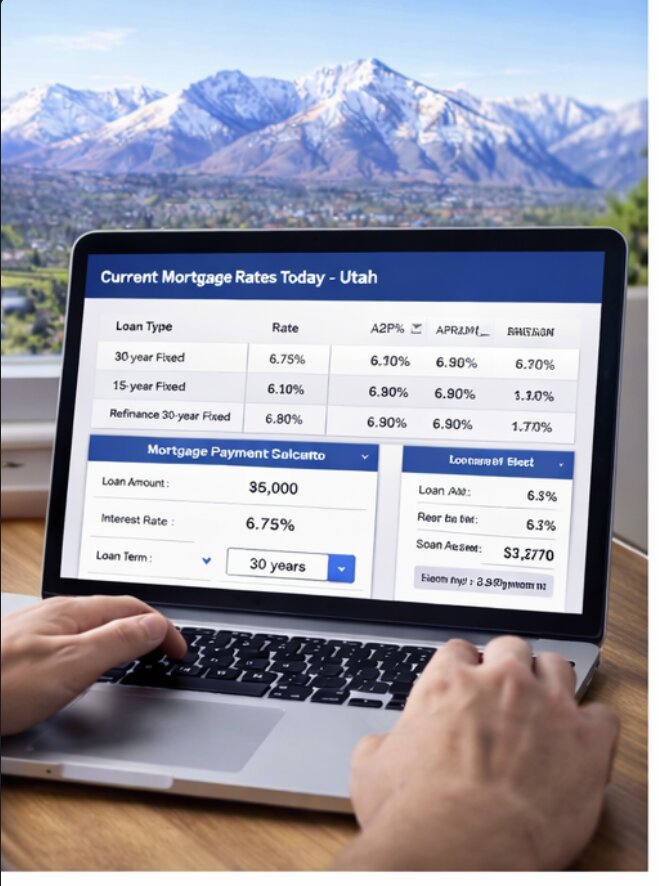

Mortgage Rates Today Utah: What Borrowers Need to Know

When searching for mortgage rates today or current mortgage rates in Utah, Salt Lake City, borrowers are typically looking for current pricing on 30-year and 15-year fixed loans. National averages influence current average mortgage rates, but local lender competition, credit score requirements, and down payment amounts affect what you personally qualify for.

Reviewing mortgage rates today refinance 30 year fixed options helps determine if refinancing makes financial sense. If you’re searching for: mortgage rates today near me, best mortgage rates today, best mortgage interest rates today, home loan mortgage rates today, home loan interest rates today. Remember that rates vary daily and are customized to each borrower.

How Mortgage Rates Affect Monthly Payments

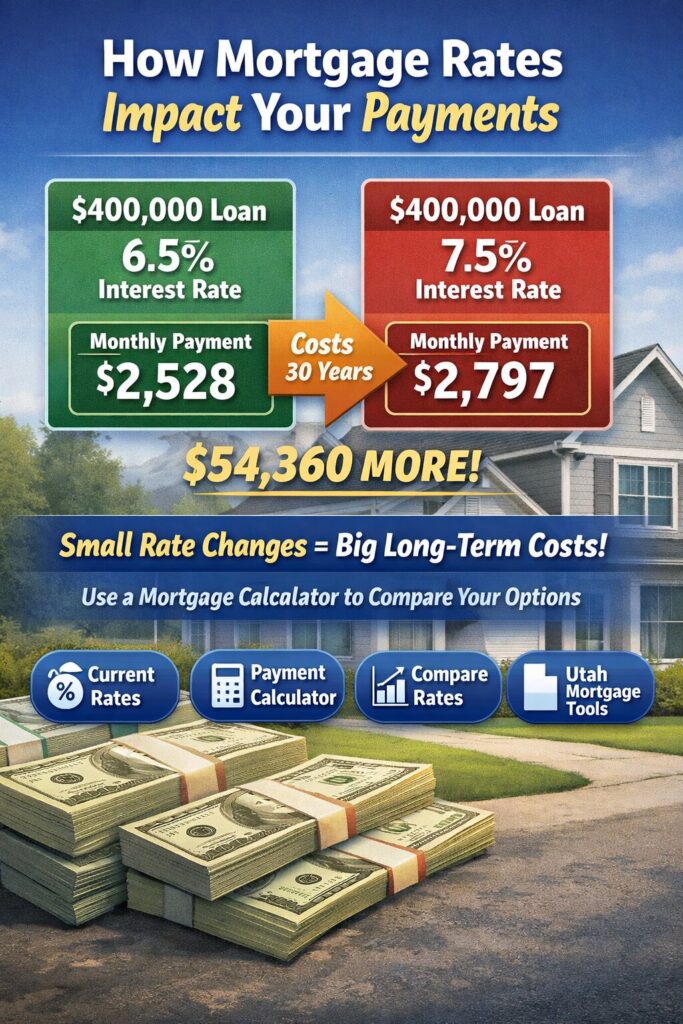

Understanding how mortgage rates affect monthly payments is more important than focusing on the rate alone.

For example:

A $400,000 loan at 6.5% vs 7.5% can change your payment by hundreds of dollars per month. Over 30 years, that difference adds up to tens of thousands of dollars.

This is why tools like: Current mortgage rates and monthly payment calculator, mortgage payment calculator with current rates, mortgage calculator based on current rates, mortgage calculator Utah, are so important before committing to a loan.

Using a mortgage estimator monthly payment tool helps you test rate scenarios and see how affordability changes in real time.

Compare Mortgage Rates Today Before You Commit

Smart buyers always compare mortgage rates today across multiple lenders.

When comparing, look at:

- Interest rate

- APR

- Loan term (15 vs 30 years)

- Closing costs

- Points

Even the best mortgage rates today may include higher fees, so reviewing full loan estimates matters.

You can monitor national market movement through Freddie Mac’s rate survey:

https://www.freddiemac.com/pmms

Refinance Mortgage Rates Today 30 Year Fixed: Should You Refinance?

Homeowners often ask:

“Should I refinance at current mortgage rates?”

Refinancing may be beneficial if:

- You can lower your interest rate

- You want to shorten your term

- You need to reduce monthly payments

Check refinance mortgage rates today 30 year fixed and compare them against your current loan before deciding.

https://www.mortgagerateutah.com/refinance-rates-utah

Why Mortgage Rates Change Daily and What Affects Mortgage Rates Today

Many borrowers wonder why mortgage rates change daily and what affects mortgage rates today.

Mortgage rates are influenced by:

- Federal Reserve policy

- Inflation

- Bond market performance

- Economic data reports

- Employment trends

Because of these factors, current mortgage rates can fluctuate even within the same week. This uncertainty leads many borrowers to ask: Is now a good time to lock mortgage rates? If rates are trending upward, locking your rate may protect your payment before closing.

Final Thoughts on Current Mortgage Rates in Utah

Tracking mortgage rates today and understanding how home loan interest rates today affect affordability can help you make confident financial decisions.

Before applying:

- Review current average mortgage rates

- Use a mortgage estimate calculator

- Compare lenders offering the best mortgage interest rates today

- Evaluate whether refinancing aligns with your goals

Staying informed ensures you’re prepared — whether buying your first home or refinancing in Utah.