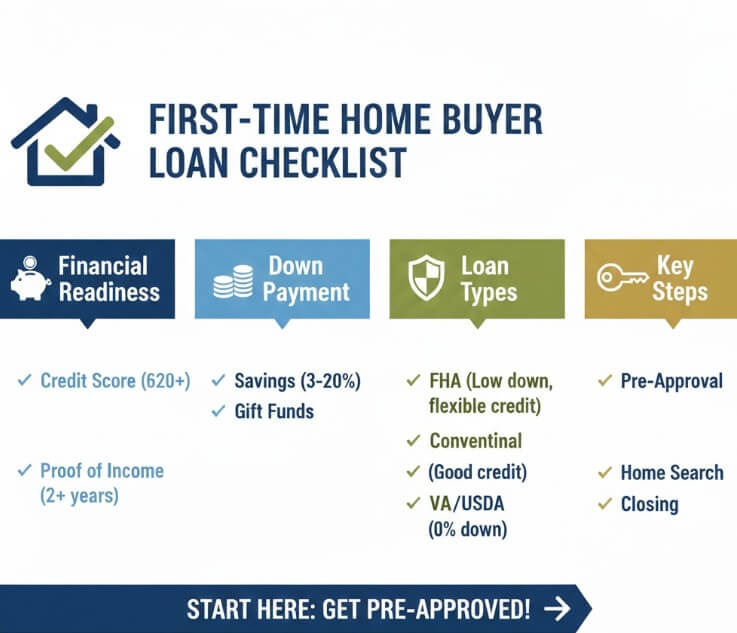

Master how to get approved for a first time home loan as you take your first exciting steps into the Utah housing market. The first concern is the average down payment on a house for first time buyer. While the old “20% down” rule is a common myth, the best lender for first home buyers will actually show you how to enter the market with much less. In 2026, many Utah buyers utilize programs that allow for as little as 3% or even 0% down. Researching the best professional mortgage lenders that prioritize education over a sales pitch is crucial. When looking for the best place to get home loan first time buyer support, local Utah expertise is invaluable for navigating our unique market, which often requires fast action and aggressive offers.

The Best Way for First-Time Buyers to Get a Mortgage

The secret is early preparation that begins months before you ever talk to a Realtor. If you’re currently renting and worried about future stability, you might wonder “how can I get help paying my mortgage”? In Utah, organizations like the Community Development Corporation of Utah (CDCU) provide grants and deferred loans to help bridge the gap for low-income families. However, the best way to prevent financial stress is to accurately calculate “how much could I get on a mortgage” before you start looking at listings. By understanding “how much would I qualify for a house”, you set a realistic budget for your home. This involves looking at your Debt-to-Income ratio, which lenders generally want to see below 43%. You can use an online mortgage calculator to test different interest rate scenarios and property tax impacts in various Utah counties.

How to Qualify for a Home Loan First Time Buyer

The path to your keys involves a few distinct stages of “approval” that often confuse beginners. USDA loans are particularly attractive because they offer 100% financing, but the property must be in a designated rural area. Generally, the ‘Three Cs’—Credit, Capacity, and Collateral—determine your success when you apply for a home loan. In 2026, Utah lenders are looking for a mid-score of at least 620 for most conventional programs, though some Utah Housing Corporation programs can work with scores as low as 600 if other factors are strong.

How to Get Pre-Approved for a Home Mortgage

Before you meet a Realtor, you must master how to get approved for a home mortgage. This is a much more powerful tool than simply knowing how to get prequalified for a home loan, which is just a rough estimate based on unverified data. In Utah’s competitive 2026 market, a pre-approval letter is essentially your ticket to the show. Once you’ve mastered the requirements, you become a “cash-equivalent” buyer in the eyes of a seller, allowing you to compete with investors and move quickly when the right home appears.

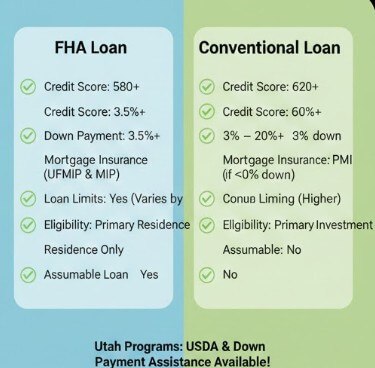

How to Qualify for an FHA Loan and Utah Government Programs

If your credit score or savings aren’t quite where you want them, look into government-backed options. Learning how to qualify for an FHA loan is often the easiest path for those with a lower credit history or higher debt loads. The specific criteria for how to qualify for FHA mortgage allow for a down payment as low as 3.5%, and Utah offers unique “second mortgage” options through the Utah Housing Corporation (UHC) that can cover that entire 3.5% for you. To prepare for this, you must understand exactly what lenders require to qualify for a mortgage: typically two years of steady employment history and a clear explanation for any large deposits in your bank accounts.

| Qualification | FHA Loan | Conventional Loan |

| Min. Down Payment | 3.5% | 3% – 5% |

| Credit Score | 580 – 600+ | 620+ |

| Mortgage Insurance | Required for life of loan | Can be removed at 20% equity |

| Best For | Lower credit/savings | Higher credit scores |

Determining How Much Mortgage Can I Qualify For

Once you determine “how much mortgage can i qualify for”, it’s time to take action and learn how to apply for a home loan. This process involves gathering your W-2s, 1099s, and two months of full bank statements. Even after you’ve closed on your home, your relationship with the mortgage market shouldn’t end. In a few years, if rates drop significantly, you might want the best mortgage refinance companies with no closing costs to lower your monthly payment and increase your home equity

Conclusion

Ultimately, knowing what you need to qualify for a home loan and where to apply for a first time home buyer loan gives you the confidence to own your future. Whether you are looking in the bustling Salt Lake Valley or the growing suburbs of Utah County, being an educated buyer is your greatest advantage. Contact us at Mortgage Rate Utah to start your personalized journey today and see which Utah-specific grants you might qualify for.