In 2025, Utah residents searching for the best mortgage solutions will face a common but critical decision: choosing between an FHA loan and a conventional loan. For many, this choice will impact not only their monthly payments but also their eligibility, long-term costs, and even the type of home they can purchase. Whether you’re a first time home buyer or someone looking to refinance mortgage Utah with bad credit, understanding the FHA vs conventional loan Utah pros and cons is essential.

First Time Home Buyer Loans in Utah

Utah continues to offer some of the most supportive programs for new homeowners. If you’re exploring first time home buyer loans, you’ll find opportunities through Utah home loan programs 2025, which include first time home buyer tax credits, down payment assistance, and flexible lending criteria. Many programs even partner with the best mortgage lenders in Utah for first time buyers to provide smoother pre-approvals and better rates.

If you’re low on savings, programs for zero down payment home loans in Utah can help you get into a home faster. Additionally, Utah first time home buyer grants 2025 and Utah mortgage assistance programs for low income households offer expanded options for qualified borrowers.

FHA Loan Requirements vs Conventional Mortgage Standards

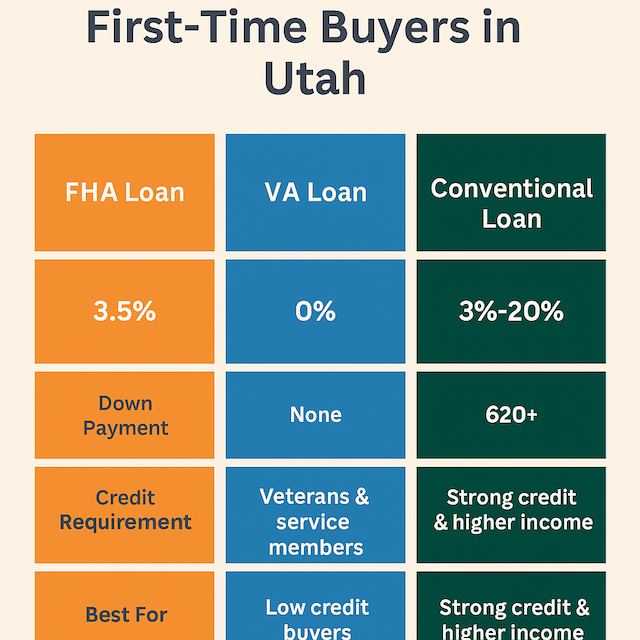

Understanding the FHA loan requirements is essential. FHA loans are backed by the government and require just a 3.5% down payment for those with credit scores above 580. This makes them ideal for people exploring low credit score mortgage options Utah.

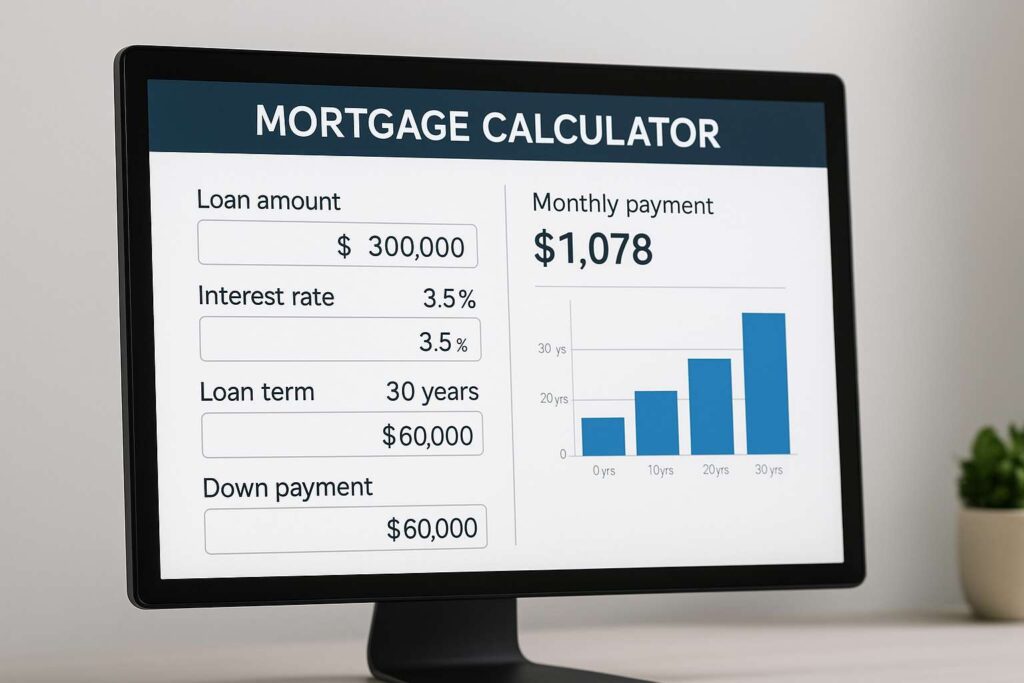

In contrast, conventional loans usually require a higher credit score (620+ minimum) and a larger down payment—typically 5% or more. However, they offer benefits such as removable mortgage insurance and lower long-term costs. Borrowers often use a refinance mortgage calculator to compare FHA vs. conventional savings scenarios.

Utah Mortgage Rates Today and What to Expect

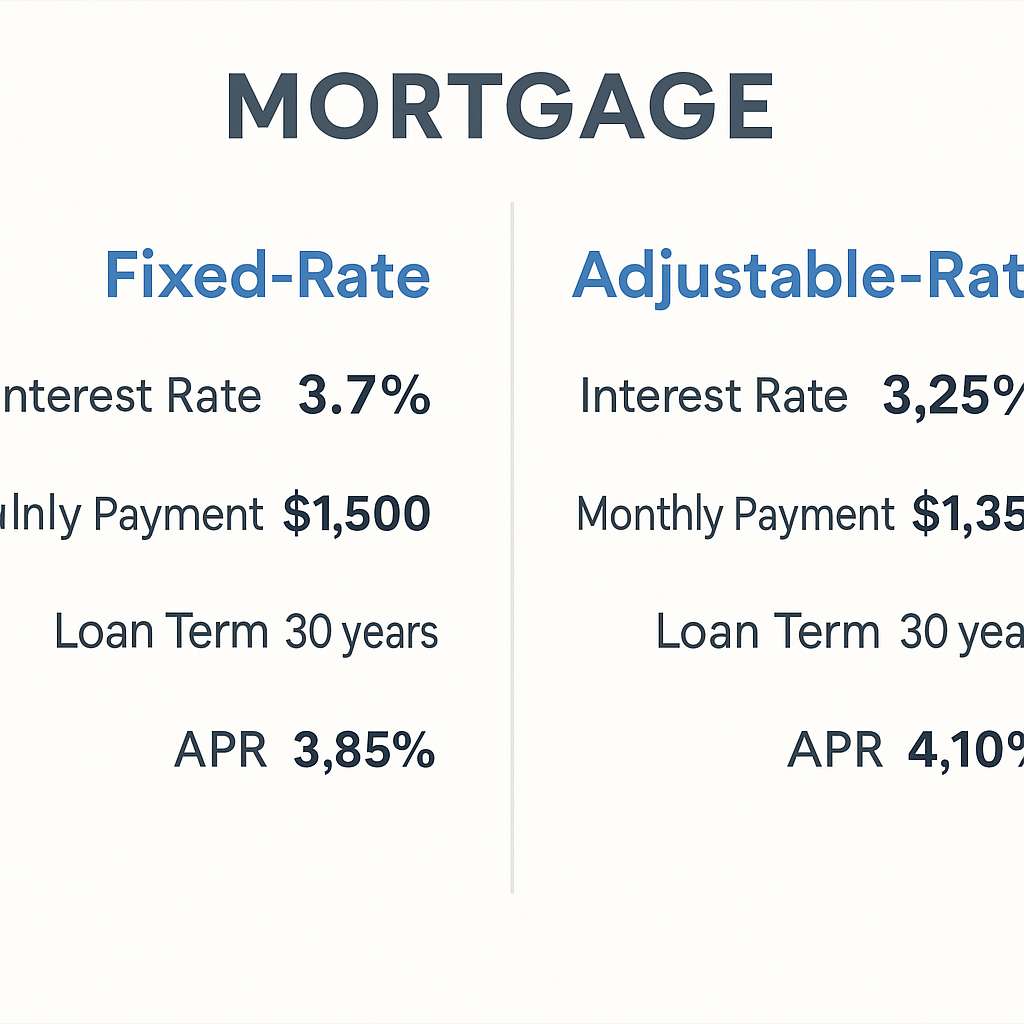

If you’re actively watching Utah mortgage rates today 30 year fixed, you’ll notice small fluctuations influenced by national trends. According to the mortgage interest rate forecast Utah, rates are expected to rise slightly throughout 2025.

FHA loan rates tend to start lower, but keep in mind they include mortgage insurance premiums for the life of the loan (unless you put 10% down). Conventional mortgage rates, while slightly higher, may be a smarter long-term choice for those who can build equity faster.

Many savvy buyers use a refinance mortgage calculator to forecast how a switch to a conventional loan could save money later—especially as refinance mortgage rates in Utah remain competitive.

Special Mortgage Programs for Utah Buyers

Utah offers specialized loan programs for unique buyer situations. For veterans and active-duty personnel, the Utah VA loan requirements for 2025 allow qualified borrowers to purchase with zero down payment, no PMI, and competitive rates.

Rural homebuyers can consider USDA loans. Understanding how to apply for USDA loan in Utah is key, as eligibility is based on location and income limits. Additionally, options like mobile home loans Utah offer financing for manufactured or modular housing through both FHA and VA pathways.

Refinancing in Utah with Less-than-Perfect Credit

Refinancing is not just for those with perfect credit. If you’re interested in refinance mortgage Utah with bad credit, several lenders in 2025 offer flexible terms and FHA-backed options.

You can use a refinance mortgage calculator to estimate potential savings and compare offers. Many Utah homeowners are making the most of current refinance mortgage rates while they remain favorable.

Which Loan Is Right for You?

Ultimately, the best loan depends on your financial profile.

FHA loans are ideal for buyers with lower credit or smaller down payments. Conventional loans are better for those with higher credit scores and stable income, offering more long-term flexibility and lower total costs.

If you’re unsure, speak with a trusted lender about your eligibility. Factors like how to qualify for a mortgage in Utah, available tax credits, and interest trends can all shape the right decision. Don’t forget to compare using resources like mortgage rates US and a refinance mortgage calculator.