Buying your first home is a major milestone, and understanding utah mortgage rates for first time buyers is one of the most important steps in the process. Mortgage rates influence how much home you can afford, your monthly payment, and your long-term financial commitment. In Utah’s competitive housing market, being informed can make the difference between feeling confident and feeling overwhelmed.

This guide breaks down current mortgage rate trends, loan options, affordability considerations, and the full application process so first-time buyers can navigate the Utah housing market with clarity.

Mortgage Rates Today in Utah and Salt Lake City

Tracking mortgage rates today utah is essential for anyone considering buying or refinancing a home. Rates fluctuate based on economic conditions, inflation, and Federal Reserve policy, which means buyers should stay informed rather than rely on outdated information.

Rates can also vary by location. For example, mortgage rates salt lake city may differ slightly from other areas of the state due to housing demand and lender competition. Borrowers interested in refinancing should also monitor mortgage rates today refinance, refinance rates utah, and refinance rates today utah to determine whether refinancing could lower their monthly payment or overall loan cost.

Comparing multiple offers is critical, which is why using tools that focus on mortgage rate comparison utah can help buyers identify competitive loan options that align with their financial goals.

How Much House Can I Afford in Utah?

A common question among first-time buyers is how much house can i afford utah. Affordability depends on income, existing debt, interest rates, and down payment size. Even small differences in rates can significantly impact monthly payments.

Understanding mortgage down payment requirements utah is also important. While traditional loans often require larger down payments, many buyers qualify for low down payment mortgage utah options that make homeownership more accessible.

In addition to down payments, buyers should explore mortgage payment options utah, including fixed-rate and adjustable-rate loans, to determine which structure best fits their budget and risk tolerance.

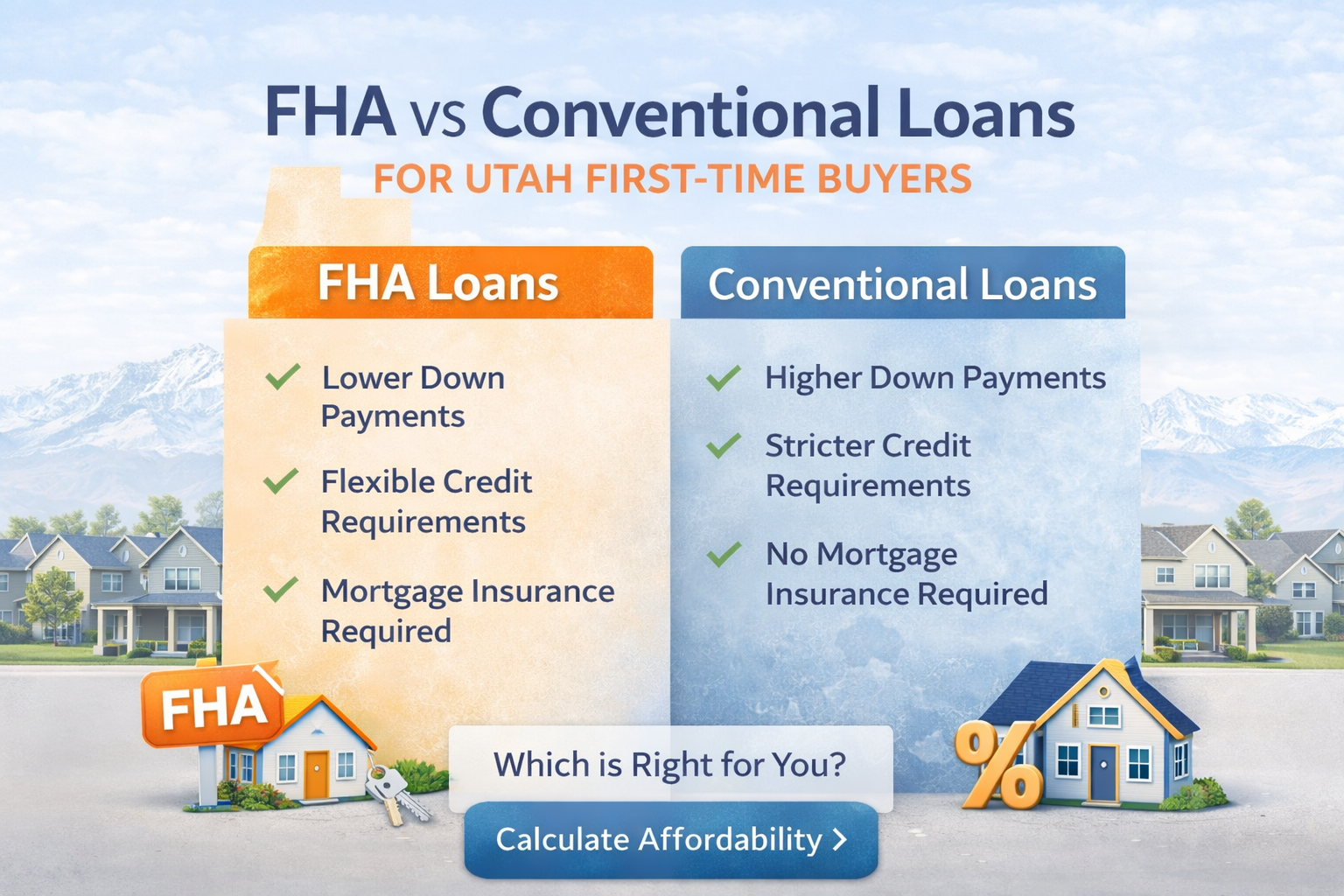

FHA Loans and Other First-Time Buyer Options

Many first-time buyers benefit from government-backed loan programs such as FHA loans utah, which are designed to make homeownership more accessible for borrowers with lower down payments or less-than-perfect credit. Searching for FHA loans near me can help buyers connect with lenders who specialize in these programs.

For those specifically entering the market for the first time, a first time buyer fha loan utah can be an excellent option due to flexible qualification requirements. However, it’s still important to compare this option with conventional financing. Understanding conventional vs fha loan utah helps buyers weigh differences in mortgage insurance, interest rates, and long-term costs.

Borrowers with strong credit may also qualify for best home loans utah or best home loans for good credit utah, which can offer lower interest rates and reduced fees.

Credit Scores, Rates, and Timing the Market

Your credit profile plays a major role in determining loan terms. Knowing how credit score affects mortgage rate utahallows buyers to understand how improving their credit before applying could lead to meaningful savings over time.

Timing also matters. Many buyers ask about the best time to buy a house in utah, which depends on market conditions, inventory levels, and interest rate trends. While predicting the market perfectly is impossible, reviewing the utah mortgage interest rate forecast can help buyers make informed decisions about when to lock in a rate.

The Utah Mortgage Application and Approval Process

Understanding the utah home buying process mortgage helps first-time buyers feel prepared rather than surprised. The journey typically starts with pre-approval and continues through underwriting, appraisal, and final approval.

During this process, buyers will encounter the utah mortgage application process, which requires documentation such as income verification, credit history, and asset statements. Knowing the expected mortgage approval timeline utah can reduce stress and help buyers plan their move more effectively.

Working with local home loan lenders utah can be especially beneficial, as local lenders often understand regional market conditions and can provide personalized guidance.

Closing Costs, Rate Locks, and Final Considerations

Beyond the purchase price and interest rate, buyers should budget for average mortgage closing costs utah, which can include appraisal fees, title insurance, and lender charges. Planning for these expenses early helps avoid last-minute surprises.

Another key decision involves utah mortgage rate lock options. Locking in a rate protects buyers from market fluctuations during the loan process, offering peace of mind in a changing rate environment.

Finally, homeowners may want to explore future financing tools such as heloc rates utah, which can provide access to home equity for renovations or other financial needs after purchasing a home.

Preparing for Success as a First-Time Buyer in Utah

Navigating utah mortgage rates for first time buyers doesn’t have to be overwhelming. By understanding current rates, loan options, affordability factors, and the application process, buyers can approach homeownership with confidence. Taking time to compare lenders, improve credit, and plan for upfront costs can make the entire experience smoother and more financially rewarding.

With the right preparation and information, first-time buyers in Utah can turn homeownership from a challenge into an achievable goal.