Navigating the 2026 real estate market requires more than just a passing interest in home listings; it requires a fortified financial strategy. As home prices remain steady and inventory remains a challenge, the first step for any serious buyer is understanding the difference between mortgage prequalification vs preapproval. While a prequalification gives you a ballpark estimate of your buying power based on self-reported data, a preapproval is a rigorous, verified commitment from a lender that carries significant weight when you finally make an offer.

How Much House Can I Afford ?

Determining your budget is the cornerstone of a successful home search. To truly answer the question, “how much house can I afford,” you must look beyond the sticker price and evaluate your monthly cash flow. In 2026, lenders are scrutinizing mortgage income requirements more closely than ever, typically looking for a debt-to-income (DTI) ratio that ensures your total monthly obligations, including your future mortgage, stay within a manageable range.

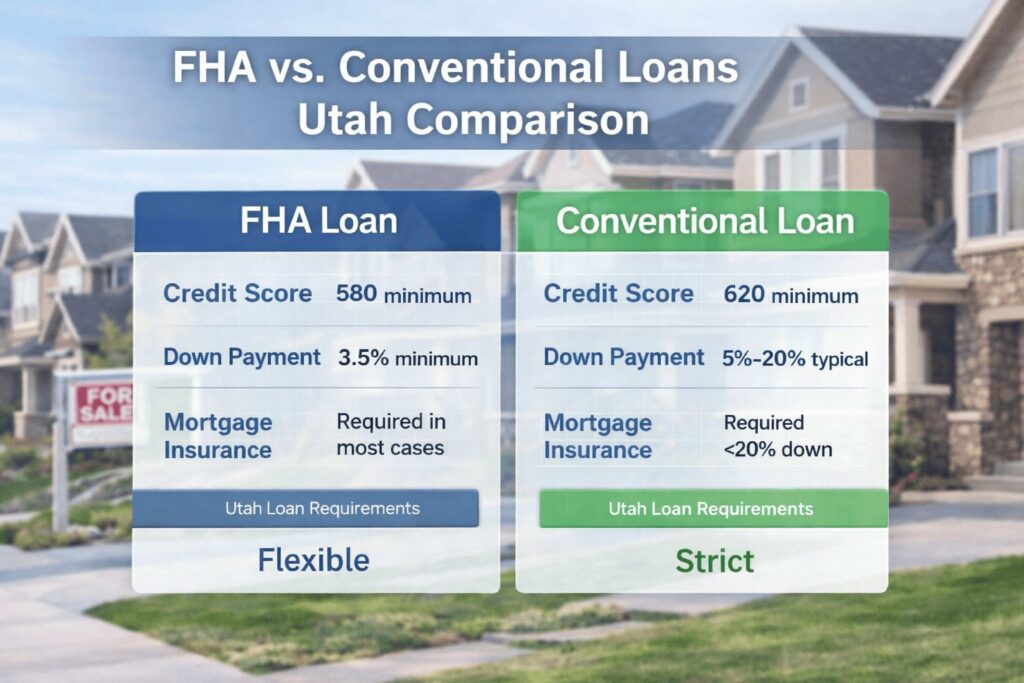

When running these numbers, many buyers forget to include the mortgage insurance cost, which is a mandatory fee for those putting down less than 20% on a conventional loan or using an FHA product. Furthermore, you must determine exactly how much do I need for a down payment to reach your desired price point. While traditional advice suggests 20%, modern FHA down payment requirements allow buyers to enter the market with as little as 3.5% down, making homeownership accessible even as savings are stretched.

First Time Home Buyer Programs

The path to your first front door is often paved with financial assistance. There are numerous first time home buyer programs available in 2026 designed to lower the barrier to entry for new market participants. These programs often provide a combination of low-interest loans and first time home buyer grants that do not require repayment, provided the buyer remains in the home for a specified period.

Because real estate trends are highly localized, you should also investigate home buyer grants [state-specific] that may offer additional tax credits or cash assistance for down payments. Many buyers find that they can “stack” these benefits with down payment assistance programs and closing cost assistance to significantly reduce the out-of-pocket expenses required at the signing table. Taking the time to research these options before you start touring homes can add tens of thousands of dollars to your effective budget.

How to Improve Credit to Buy a House

Your credit score is the single most important factor in determining your interest rate and loan eligibility. If you find your score is below the minimum credit score for mortgage approval, typically 620 for conventional loans or 580 for FHA, you must prioritize how to improve credit to buy a house. This process includes paying down high-interest credit card debt, ensuring all utility bills are paid on time, and avoiding any new large purchases or credit inquiries in the months leading up to your application.

Once your credit is in a healthy range, you can explore more specialized financing options. For example, if you are looking at properties in less populated areas, a USDA rural development loan offers a 0% down payment option for eligible borrowers. For those with an Individual Taxpayer Identification Number, an ITIN home loan provides a vital alternative to traditional Social Security-based financing. If your dream home is a fixer-upper, the fha 203k loan allows you to bundle renovation costs directly into your mortgage, though you should be prepared for the fact that this specific, “how long does mortgage approval take” question often results in a 45-to-60-day timeline due to the extra inspections required.

Navigating Specific Loan Requirements

Different properties come with vastly different financial hurdles. If you are eyeing a luxury property, you must meet the stringent jumbo loan requirements, which often include higher cash reserves and credit scores. Conversely, those interested in a more affordable entry point might investigate a manufactured home loan, though these require the home to be permanently affixed to a foundation to qualify for traditional real estate rates.

Condo living offers its own set of challenges, as condo financing requirements demand that the homeowner association (HOA) maintains adequate insurance and financial reserves. Regardless of the property type, your lender will conduct a thorough audit of your finances to ensure you meet all mortgage income requirements. Understanding these nuances early in the process, before the clock starts ticking on a purchase agreement, is the difference between a smooth closing and a failed deal.