Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Buying your first home in Utah is an exciting milestone, but it can also feel overwhelming. Between rising home prices, changing current mortgage rates, and trying to figure out how much money you need for a down payment, it’s easy to feel like homeownership is out of reach. Many first-time buyers also wonder if their credit score is high enough, how much they need to earn, or whether they even qualify for a mortgage.

The good news is that getting mortgage pre approval is one of the best places to start. It helps you understand what you can comfortably afford before you begin touring homes and gives sellers confidence that you’re a serious buyer.

Whether you’re a first time home buyer or simply looking to better understand the home-buying process, this guide will walk you through loan options, down payment assistance utah, first time home buyer programs utah, and the steps you can take to move toward homeownership with confidence.

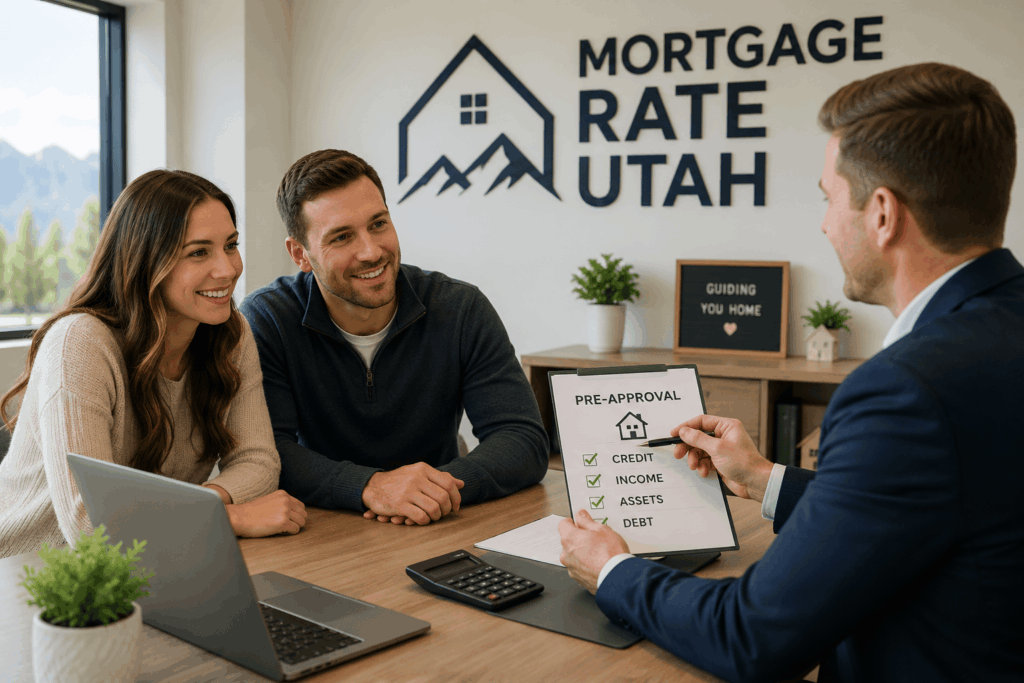

Getting mortgage pre approval before you begin house hunting helps you understand your budget and puts you in a stronger position when you’re ready to make an offer. During the pre-approval process, your lender reviews your income, employment history, debt, assets, and credit profile to determine how much you may qualify to borrow. This helps ensure you’re shopping within a realistic budget before falling in love with a home.

Benefits of Mortgage Pre Approval

Working with a trusted mortgage lender or mortgage broker in Utah can help you compare loan options, understand your financing choices, and find the best mortgage lender in Utah for your financial goals. Keep in mind that a mortgage pre-approval is not a final loan approval, but it is one of the smartest first steps you can take before buying a home.

One of the biggest misconceptions about buying a home is that you need a 20% down payment. While putting more money down can lower your monthly payment, many loan programs allow qualified buyers to purchase a home with much less. Depending on your financial situation, you may be able to qualify for a conventional loan with as little as 3% down, while an FHA loan typically requires 3.5% down. Eligible veterans and active-duty military members may qualify for a VA loan with no down payment, and buyers purchasing in eligible rural areas may qualify for a USDA loan, which also offers zero-down financing. Working with a trusted mortgage lender can help you compare these options and determine which loan program best fits your financial goals.

Utah offers several resources that can make homeownership more attainable for first-time buyers. Depending on your financial situation, you may qualify for first time home buyer programs utah, first time home buyer grants utah, or first time home buyer loans utah that can help reduce upfront costs. Some buyers may also qualify for down payment assistance utah, making it possible to purchase a home sooner than they expected.

Before applying, it’s important to understand the first time home buyer requirements utah, including income, credit score, and loan eligibility requirements. Because every buyer’s financial situation is different, working with an experienced mortgage lender can help you identify which programs you qualify for and determine the best path toward homeownership.

Review FHA loan requirements Utah, FHA loan credit score requirements Utah, VA loan requirements Utah, VA home loan eligibility, and USDA loan requirements Utah to determine which program fits your needs.

One of the biggest questions for first-time buyers is, “How much house can I afford?” The answer depends on several factors, including your income, monthly debt, credit score, down payment, and current mortgage rates. Lenders review each of these when determining how much you may qualify to borrow and what your estimated monthly payment will be.

Before you begin shopping for a home, it’s helpful to use a mortgage payment calculator, home loan calculator, or mortgage calculator to estimate what a comfortable monthly payment might look like. While these tools provide a good starting point, speaking with a trusted mortgage lender is the best way to receive an accurate estimate based on your unique financial situation.

· Government-issued ID

· Recent pay stubs

· W-2s or tax returns

· Bank statements

· Employment information

· Estimated down payment

Yes, many qualified buyers can.

Usually 60–90 days.

A hard inquiry may have a small temporary impact.

1. Check your credit score.

2. Estimate your budget.

3. Compare loan options.

4. Gather documents.

5. Get mortgage pre approval.

6. Start shopping for a home.