Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Buying a home is a major financial decision, and the mortgage rate you receive can affect your monthly payment for years. For Utah buyers, understanding how to get the best mortgage rates in Utah can make the process easier to navigate and help you make a smarter financial choice. Since current mortgage rates in Utah can change often, it is important to compare lenders, understand your credit profile, and know what factors influence your final loan offer. A clear plan can help you feel more confident before applying for a home loan.

Understanding current mortgage rates utah today is a useful starting point because rates directly affect affordability. A lower rate can reduce your monthly payment, while a higher rate can increase the total cost of the same home over time. However, the rate shown online is usually only a general estimate. The actual rate you qualify for depends on your financial situation, loan type, credit history, and lender.

When comparing mortgage rates in utah, it is helpful to look at more than one lender instead of relying on the first rate you see. Utah mortgage rates today can give buyers a broad view of the market, but individual loan offers may vary. Comparing utah home loan rates, current home loan rates utah, and home loan interest rates utah can help buyers see how rates, fees, and loan terms differ between lenders.

It is also important to pay attention to home loan interest rates right now because mortgage rates can change quickly. Rates may shift due to inflation, housing demand, national economic trends, and lender competition. Checking rates regularly can help buyers decide whether to move forward, keep comparing options, or improve their financial profile before applying.

Learn more about Utah mortgage options from Mountain America Credit Union: https://www.macu.com/loans/home-loans/utah-mortgages

Before applying, it can be helpful to understand the average mortgage rate utah so you have a general idea of what borrowers may be seeing in the market. Average rates are useful for comparison, but they do not guarantee the exact rate one individual buyer will receive. A buyer with strong credit, steady income, and a larger down payment may qualify for a lower rate than someone with more debt or a lower credit score.

One of the most common loan options is a 30-year fixed mortgage. Looking at 30 year mortgage rates utah can help buyers understand how this type of loan may affect monthly payments. A 30-year mortgage spreads payments over a longer period, which can make the monthly payment more manageable. However, borrowers may pay more interest over the life of the loan compared to a shorter term. Utah buyers should compare monthly payments, total interest cost, and long-term goals before choosing a mortgage.

Credit score is one of the most important factors lenders review when setting a mortgage rate. A strong credit score for mortgage approval can help borrowers receive better rates because lenders may view them as lower risk. A lower score does not always prevent someone from getting a loan, but it can lead to a higher interest rate or fewer loan options.

For Utah buyers, understanding credit score for mortgage Utah requirements can make the process feel more manageable before applying. The credit score needed to buy a house can vary by lender and loan program, so it is important to compare options. Buyers can improve their credit by paying bills on time, lowering credit card balances, avoiding new debt, and checking their credit report for errors.

The relationship between current mortgage rates by credit score is important because credit can influence loan pricing. Two Utah buyers purchasing similar homes may receive different rates based on their credit history. This is why improving credit before applying can be one of the best ways to lower long-term mortgage costs.

Before making offers on homes, buyers should understand the mortgage pre approval process. Pre-approval is when a lender reviews financial information and estimates how much a buyer may be able to borrow. This helps buyers understand their price range and shows sellers that they are serious.

The mortgage pre approval process utah can be especially helpful in competitive housing markets. A pre-approval letter can make an offer stronger because it shows that a lender has reviewed the buyer’s income, credit, and financial documents. Completing mortgage pre approval utah early can also help buyers compare lenders and avoid delays once they find a home they like.

A common question is how long does mortgage pre approval take. The answer depends on the lender and how quickly the buyer provides documents. Lenders may ask for pay stubs, bank statements, tax documents, employment history, and permission to check credit. Buyers should also understand mortgage pre approval how long does it last, because pre-approval letters usually expire after a set period. If the home search takes longer, the buyer may need to update financial information with the lender.

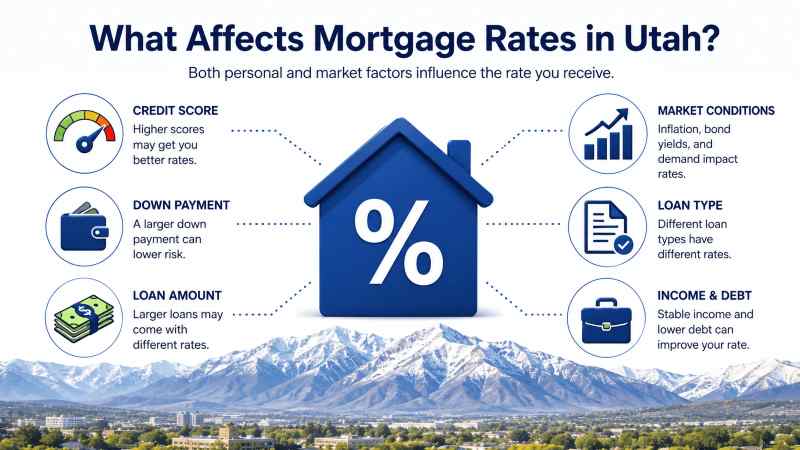

Understanding what affects mortgage rates in Utah can help buyers make better decisions. Mortgage rates are influenced by personal factors and larger market conditions. Personal factors include credit score, income, debt-to-income ratio, down payment, loan amount, and loan type. Market factors include inflation, bond markets, housing demand, and national interest rate trends.

Lenders also consider risk. A borrower with strong credit, reliable income, and manageable debt may qualify for better loan terms. A borrower with a smaller down payment or higher debt may receive a higher rate. This is why buyers should not rely only on advertised rates. Personalized quotes from multiple lenders are usually more useful.

Learning how to qualify for a mortgage starts with understanding what lenders look for. Qualifying usually means showing that you have enough income, stable employment, acceptable credit, manageable debt, and money available for a down payment and closing costs. Lenders want to know that you can afford the payment and repay the loan responsibly.

For buyers comparing first time home buyer mortgage rates, it is helpful to ask about different loan programs. Some first-time buyer programs may offer lower down payment options or other benefits for qualified borrowers. Comparing conventional loans, FHA loans, VA loans if eligible, and Utah-based programs can help buyers find a loan that fits their financial situation.

If your goal is how to lower mortgage rates Utah, there are several practical steps to consider. First, work on improving your credit score before applying. Second, save for a larger down payment if possible. Third, compare quotes from multiple lenders because rates and fees can vary. Buyers may also consider mortgage points, which allow them to pay more upfront in exchange for a lower rate. This can be helpful for buyers who plan to stay in the home long enough to benefit from the lower monthly payment.

Compare today’s Utah mortgage rates from City Creek Mortgage:

https://citycreekmortgage.com/todays-rates/

Finding the right mortgage rate is not just about choosing the lowest number online. It is about understanding your financial profile, comparing lenders, preparing for pre-approval, and knowing what affects your rate. Utah buyers should review home loan interest rates Utah, understand the role of credit, and complete the pre-approval process before making offers.

By preparing early, buyers can make stronger decisions and avoid surprises. Whether you are comparing best mortgage rates in Utah, reviewing your credit score, or learning how pre-approval works, the most important step is to stay informed and compare your options carefully. A stronger financial profile can help you qualify for better loan terms and potentially save money over the life of your mortgage.