Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Buying a home is one of the largest financial decisions most people will ever make, and understanding mortgage rates can have a significant impact on how much you’ll pay over the life of your loan. Even a small difference in interest rates can add up to thousands of dollars in savings. Whether you’re purchasing your first home, comparing home loans, or looking for a trusted mortgage lender, learning how the mortgage process works will help you make more confident financial decisions.

Helpful resources for getting started include the Consumer Financial Protection Bureau (CFPB) Mortgage Guide and general market insights from Freddie Mac Mortgage Rates Data.

With so many lenders and loan options available, it’s easy to feel overwhelmed. From comparing interest rates to choosing between government-backed loans and conventional financing, understanding your options is essential. This guide explains what influences mortgage rates, how to compare lenders, and when refinancing or using your home equity might make sense.

Keeping an eye on mortgage rates today and current mortgage rates is one of the best ways to prepare for buying a home. Mortgage rates change daily based on inflation, the economy, and financial markets. While you can’t control the market, you can improve your chances of qualifying for lower mortgage interest rates by maintaining a strong credit score, reducing debt, and saving for a larger down payment.

You can track national rate trends using sources like Freddie Mac Primary Mortgage Market Survey or compare lender estimates on platforms like Bankrate Mortgage Rate Comparisons.

Many buyers compare 30 year mortgage rates because they offer stable monthly payments over the life of the loan. Others may choose shorter loan terms to save money on interest, even if the monthly payments are higher. Understanding how rates affect your budget will help you choose the loan that’s right for you.

There isn’t a one-size-fits-all mortgage. Different home loans are designed for different financial situations, so it’s important to understand your options before committing to a mortgage loan.

Conventional loans are widely used and typically backed by Fannie Mae and Freddie Mac — learn more at Fannie Mae Home Loan Programs and Freddie Mac Borrower Resources.

FHA loans, backed by the federal government, are designed to help buyers with lower credit scores or smaller down payments. You can review eligibility details at HUD FHA Loan Information.

For eligible veterans and active-duty military members, a VA loan can be an excellent option because it often requires little or no down payment and doesn’t include private mortgage insurance. Learn more at VA Home Loan Program.

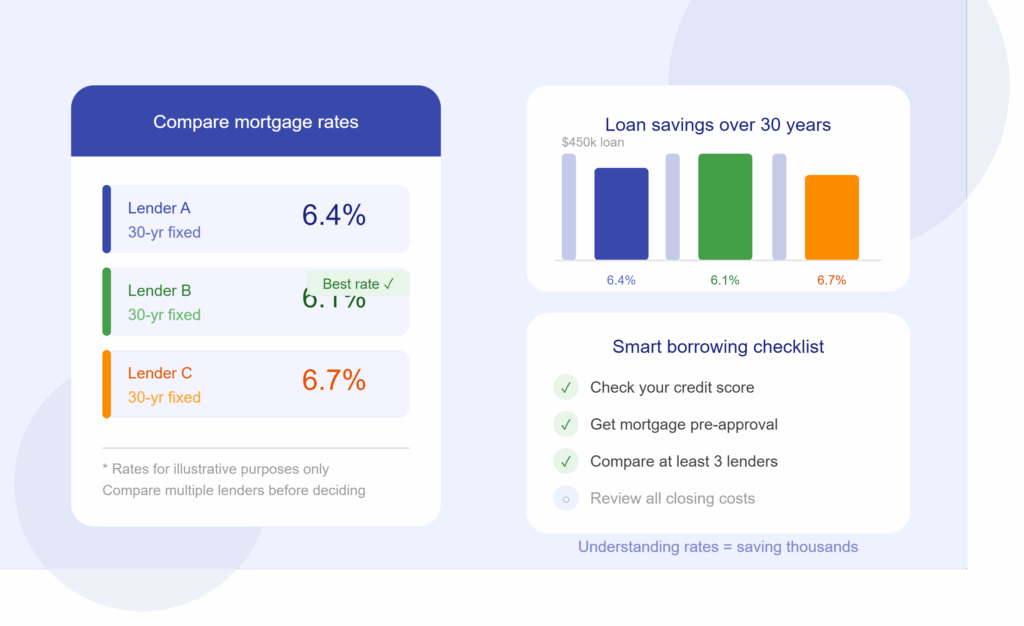

Choosing the right mortgage lender is about more than simply finding the lowest interest rate. A good lender should provide clear communication, competitive loan options, and excellent customer service throughout the home-buying process.

You can compare lenders and market offerings using tools like Zillow Mortgage Marketplace or rate comparison sites such as Bankrate Mortgage Lenders.

Many buyers also research the best mortgage companies before making a decision. Others prefer working with a mortgage broker, who can compare loan products from multiple lenders. Searching for a mortgage broker near me can help connect you with professionals in your local housing market.

No matter which route you choose, request a mortgage quote from several lenders. Looking beyond the interest rate and comparing fees, closing costs, and loan terms can save you money over time.

Before shopping for homes, obtaining mortgage pre approval gives you a realistic budget and shows sellers that you’re a qualified buyer. During this process, your lender reviews your finances to determine how much you’re likely to borrow.

You can learn more about the pre-approval process from the CFPB Home Loan Preapproval Guide.

Once you’ve found the right home, you’ll officially apply for a mortgage. Keeping your financial documents organized and responding quickly to lender requests can help move the approval process along and reduce delays before closing.

If you’ve already purchased a home, mortgage refinancing may allow you to lower your monthly payment, reduce your interest rate, or shorten the length of your loan. Comparing refinance mortgage rates can help you determine whether refinancing makes financial sense.

You can explore refinance tools and guidance from sources like the Bankrate Refinance Guide.

Although refinancing can save money, it’s important to weigh closing costs against your long-term savings before making a decision.

As your mortgage balance decreases and your home’s value increases, you’ll build equity that can be used for future financial needs. A home equity loan provides a lump sum with fixed monthly payments, while a home equity line of credit offers more flexibility.

General equity borrowing guidance can be found at the CFPB Home Equity Guide.

Many homeowners choose a HELOC to finance renovations, pay for education, or consolidate higher-interest debt. Before borrowing, compare HELOC rates, understand how repayment works, and review home equity loan rates to determine which option is best for your situation.

Finding the right mortgage isn’t just about getting the lowest interest rate. It’s about comparing lenders, understanding your loan options, and choosing financing that fits your financial goals.

By researching mortgage rates, comparing home loans, selecting the right mortgage lender, and understanding options like mortgage refinancing, home equity loans, and HELOCs, you’ll be better prepared to make informed decisions throughout the home-buying process.

Taking the time to compare loan offers, improve your financial profile, and stay informed about market trends can save you money and make homeownership more affordable for years to come.