Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

When people search for mortgage rates, they usually want one thing: a clear answer about what it will cost to buy or refinance a home. In a market where mortgage rates today can change quickly, it helps to understand what drives pricing, how to compare loans, and what steps can lead to the best mortgage rates for your situation. For Utah buyers and homeowners, that process becomes even more useful when you focus on local needs, local housing goals, and the type of loan that fits your financial plans.

At MortgageRateUtah.com, the goal is not just to show numbers. It is to help readers understand how current mortgage rates affect monthly payments, how different loan terms change the long-term cost of borrowing, and when refinancing might make sense. Whether you are looking at home mortgage rates for a new purchase or comparing refinance mortgage rates for an existing loan, the right strategy can save money and reduce stress.

If you are shopping for a home, current mortgage rates are one of the biggest factors in your monthly budget. Even a small rate change can affect your payment, your total interest cost, and the price range you can comfortably afford. That is why many buyers check home mortgage rates today before they start house hunting. The better you understand the market, the easier it is to spot opportunities and avoid surprises.

A good starting point is to compare current home mortgage rates with your expected down payment, credit profile, and loan type. Borrowers with strong credit and stable income often have access to the best mortgage rates today, while other buyers may need to improve their position before locking in a loan. It also helps to compare average mortgage rate data with personalized offers to see whether a quote is truly competitive.

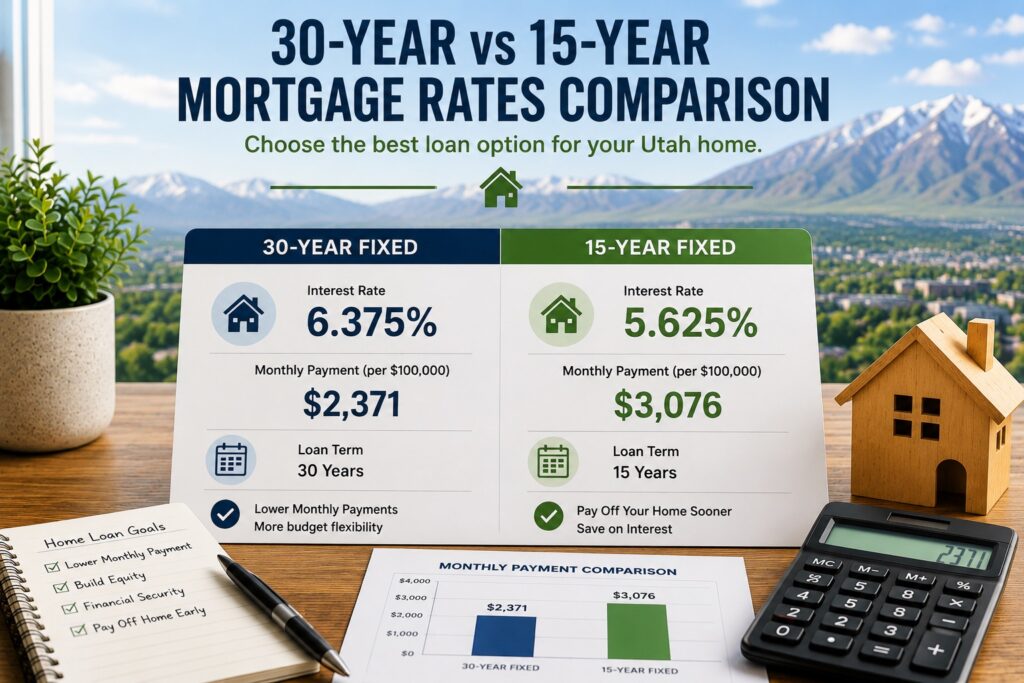

For many Utah buyers, the most common purchase loan is a fixed-rate mortgage. That is why 30-year fixed mortgage rates and current 30-year fixed mortgage rates receive so much attention. These loans provide predictable monthly payments and long repayment terms, which makes them appealing for first-time buyers and families planning to stay in a home for many years. If you are comparing offers, you may also want to look at the best 30-year mortgage rates and 30-year mortgage rates today to see which lenders are offering the strongest terms.

Many borrowers focus on 30-year mortgage rates because the lower monthly payment can make homeownership more manageable. A 30-year loan usually spreads the balance over a longer period, which can help keep the payment affordable. For buyers who want flexibility, that can be a smart option. But if you can handle a higher payment, 15-year mortgage rates may offer a lower overall interest cost and a faster path to owning your home outright.

It is smart to compare 15-year fixed mortgage rates with 30-year options before making a decision. A shorter term often comes with a better interest rate, but the payment may be significantly higher. That is why buyers should look beyond the headline rate and compare the full monthly cost, including taxes, insurance, and any mortgage insurance that may apply. A simple mortgage rate calculator can help you test different scenarios and see how the numbers change.

Some borrowers also watch average 30-year mortgage rate trends and the average 30-year mortgage rate today to get a sense of where the market stands before applying. If you are seeing current 30-year mortgage rates that fit your budget, you may decide to move forward faster. If not, waiting, improving your credit, or increasing your down payment could help you qualify for the lowest mortgage rates later on.

Homeowners often watch refinance mortgage rates to decide whether a new loan could lower their payment or shorten their term. Refinancing may be worth considering if you can move from a higher rate to a current refinance with significantly lower mortgage rates, or if you want to switch from a long-term loan to a shorter one. In some cases, the goal is not only payment relief but also a faster payoff or a more stable loan structure.

The best time to refinance depends on your current loan, your home equity, and your financial goals. Some homeowners search for the best refinance mortgage rates when they want to reduce interest expense, while others look for current refinance mortgage rates simply to see whether the market has improved enough to justify a change. If you own a higher-balance property, jumbo mortgage rates can also matter because larger loans often follow a different pricing structure than standard conforming mortgages.

It is also worth checking current mortgage rates against your existing rate before you apply. If the difference is small, refinancing may not save enough to cover closing costs. But if the new rate is lower and the timeline works, refinancing can still be a smart move. Borrowers sometimes use best mortgage rates and best refinance mortgage rates as benchmarks, then compare those quotes with their own loan estimate to see whether the deal truly makes sense.

Shopping for a mortgage is about more than finding the lowest interest rate. Compare the loan type, closing costs, lender fees, and how long you plan to stay in your home. Looking at all of these factors will help you choose the best mortgage.

Comparing offers from different lenders is one of the best ways to find the right loan. If you plan to stay in your home for many years, a 30-year fixed mortgage may be a good choice because it offers stable monthly payments. If you want to pay off your loan faster and save on interest, a 15-year mortgage may be a better option.

Mortgage rates are different for every borrower. Your credit score, down payment, loan amount, and property type all affect the rate you receive. That is why it is important to compare personalized loan offers instead of only looking at average mortgage rates.

Utah borrowers with larger loan amounts may also want to compare jumbo mortgage rates. First-time buyers often choose a 30-year mortgage because it usually has lower monthly payments. A mortgage rate calculator can help you estimate your monthly payment and the total cost of the loan.

Talking with a trusted local lender can help you understand your options. Comparing loans before making a decision can help you save money over time. Locking in a rate when the numbers make sense can also help you avoid future rate increases. If you are serious about affordability, compare the lowest mortgage rates available to you and consider the total cost of the loan before making your decision.

For readers who want more educational support, this article can also link internally to MortgageRateUtah.com and externally to a trusted consumer resource such as the Consumer Financial Protection Bureau at https://www.consumerfinance.gov/ for general mortgage education.

Choosing the right mortgage is about more than just finding the lowest interest rate. It is about finding a loan that fits your budget, your goals, and your financial situation. By comparing current mortgage rates, 30-year and 15-year mortgage rates, and refinance options, Utah homebuyers and homeowners can make better decisions and avoid unnecessary costs.

Whether you are buying a home, refinancing, or simply researching your options, staying informed is the best first step. With the right information and careful planning, you can choose a mortgage that works for your needs now and in the future.