Let’s be real for a second: looking at the housing market right now can make you want to hyperventilate. If you’re trying to figure out how much down payment you need for a house, you’ve probably seen the soaring numbers and felt completely overwhelmed. It is an intense environment to step into, especially if you’re doing it for the first time. But before you stress-sweat through your shirt, you should know that you don’t have to scrape together a massive fortune all on your own. There are actual, real-life first time home buyer programs in place specifically to help people catch their breath and get a foot in the door. If you are buying a home with low credit or just feel like you’re financially stretched to your limit, there is a way to find some balance in all this chaos.

The secret to keeping your sanity is understanding where the financial relief is hidden. By knowing the rules of engagement, you can tap into massive state grants, specialized loans, and local city incentives designed to build your bridge to homeownership. Let’s break down the actual grants and assistance programs that can help you buy your space without losing your peace of mind.

Utah Housing Corporation Down Payment Assistance: The State-Level Powerhouse

When you begin your research, the biggest resource you will encounter is the state housing authority. This organization exists specifically to create affordable housing solutions. If your personal savings account isn’t quite where you want it to be, tapping into housing corporation down payment assistance can completely change your homebuying trajectory.

Essentially, the program works by pairing a regular mortgage with a subordinate second loan that covers your upfront costs. To successfully navigate this path, you need to master how to qualify for a housing loan option. It isn’t as intimidating as it sounds, but it does require meeting specific criteria regarding your debt-to-income ratio, employment history, and household size. Furthermore, you must keep a close eye on the official income limits for a housing loan. Because these options are tailored to help low-to-moderate-income families, your total household income cannot exceed certain caps, which fluctuate depending on the specific county you are looking to live in.

Another critical piece of the puzzle is your credit profile. Fortunately, the state is relatively flexible compared to strict corporate lenders. Reviewing the updated housing score requirements 2026 standards shows that you generally need a minimum credit score ranging between 620 and 660, depending on the exact tier of financing you select. If you meet these benchmarks, you can gain access to the conventional preferred loan program, which offers excellent interest rates and lower mortgage insurance costs than traditional market options.

Utah First Time Home Buyer Grant 2026: Local Cash Inlets

While state programs offer incredible baseline coverage, true financial zen comes when you look closer to home. Many buyers completely miss out on free money because they don’t look at local municipal funds. If you broaden your search, you will find excellent localized resources like your local county first time home buyer program or specialized county down payment assistance funds.

These local government programs are heavily focused on community stabilization. For instance, if you look into down payment assistance initiatives in major cities, you’ll discover that local municipalities frequently offer deferred or forgivable loans to individuals who promise to occupy the home as their primary residence for a set number of years. Many of these programs are fueled by a community development block grant housing allocation, which pumps federal money directly into local neighborhoods to make purchasing realistic for everyday working people.

If you expand your toolkit further, you should check your eligibility for the first time home buyer grant 2026 updates, as well as specialized state down payment assistance 25k programs. These substantial financial assistance structures were specifically enacted to help buyers combat rising interest rates by providing substantial equity right at the closing table. Additionally, look into the first time home buyer tax credit, which allows you to claim a portion of your annual mortgage interest as a direct deduction on your tax returns, saving you thousands of dollars over the lifespan of your loan. If you have faced severe financial hardships, it is also worth researching HAF program qualifications to see if any remaining Homeowner Assistance Funds can be utilized for your transition.

Grants for Buying a Home in Utah: Tailored Loan Paths

There is no such thing as a one-size-fits-all mortgage. Depending on your personal background, specific grants for buying a home might open doors you didn’t even know existed. For example, there are highly targeted funds like single mother home buyers grants programs that focus heavily on helping single-parent households establish long-term housing security.

Beyond grants, your choice of the underlying loan structure matters immensely. If your credit history has a few bruises, looking into the standard FHA loan requirements lenders enforce is an excellent safety net. FHA loans are backed by the federal government and allow for lower down payments and softer credit score restrictions. If you want to avoid a down payment entirely, you can look into rural areas or specific programs that facilitate a zero down payment mortgage strategy, allowing you to walk into closing without draining your liquid cash.

All of these diverse options fall under the umbrella of low income home loans providers offer to ensure that teachers, healthcare workers, and first-time buyers aren’t entirely priced out of our local communities.

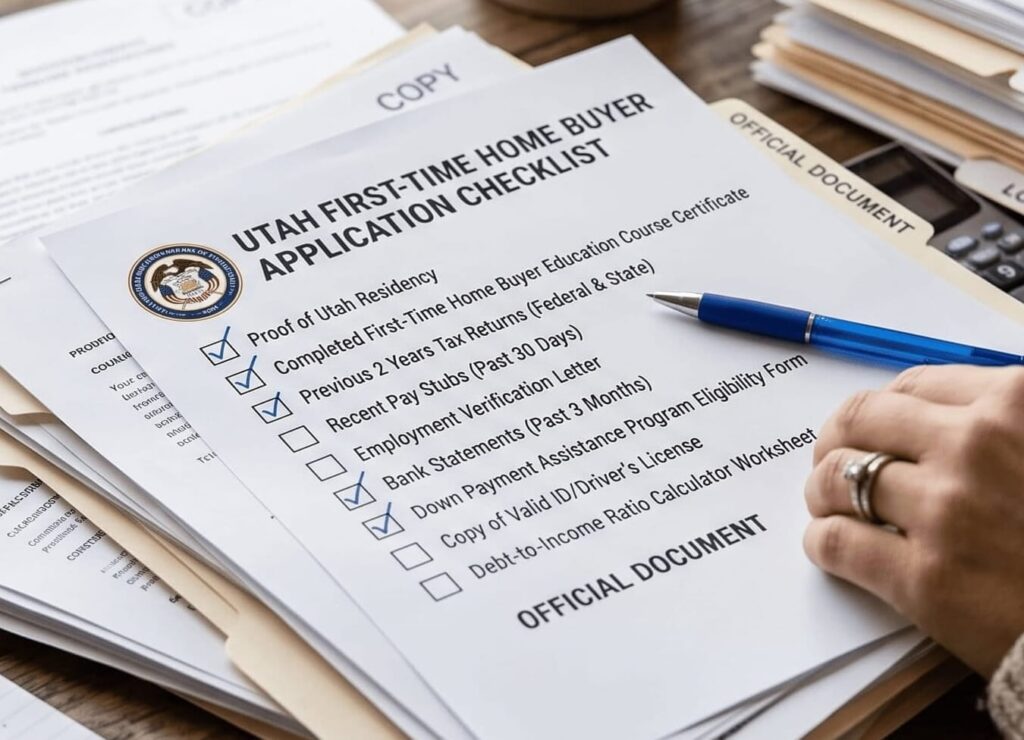

Utah First Time Home Buyer Checklist: Your Action Plan

To bring your homebuying journey into perfect alignment, you need to move systematically. You cannot just jump into the deep end without preparation. Your first step should always be completing a certified first time home buyer education course. These classes are incredibly informative, and more importantly, completing one is a mandatory prerequisite to unlock almost every single down payment grant mentioned above.

To help you organize the chaos, here is your essential first time home buyer checklist:

- Check your credit score and clear up any outstanding collections.

- Gather two years of tax returns, W-2s, and your most recent bank statements.

- Complete your approved homebuyer education class.

- Get pre-approved by a lender specializing in housing grants.

As you check off those boxes, remember that who you work with matters. You want to deliberately seek out the best mortgage lenders for first time buyers the market has to offer. Find a loan officer who treats you like a human being, answers your midnight anxiety texts, and deeply understands how to layer grants on top of your loan.

Before you take the plunge, take a deep breath. Review the strict first time home buyer requirements, get your paperwork organized, and realize that owning a home is entirely within your reach. With a clear strategy and the right assistance programs, your financial goals are closer than you think.