Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

For Utah homeowners watching home loan interest rates closely, the question

of whether to refinance mortgage utah today is one of the most significant

financial decisions they face in 2026. With housing interest rates today

stabilizing after years of volatility, the calculus around refinancing has shifted –

and for many borrowers, the window may be opening.

Understanding what drives current home mortgage rates, how the numbers

work, and how to position yourself to capture the lowest mortgage rates utah

has to offer is essential before you pull the trigger on a refinance.

The mortgage rates utah today environment reflects a market that has largely

normalized after the sharp swings of 2022 and 2023. The current mortgage

rates utah today for a standard 30-year conventional refinance are hovering in

the low-to-mid 6 percent range, with well-qualified borrowers occasionally

accessing rates below that. The interest rates today 30 year fixed are the

benchmark most homeowners track, and the current 30 year fixed mortgage

rate utah sits close to national averages.

Homeowners who purchased in 2023 or early 2024, when rates peaked above 7

percent, are among those with the clearest refinancing case. Even dropping from

7.25 percent to 6.25 percent on a $400,000 loan saves roughly $300 per month –

a meaningful difference in monthly cash flow.

The home mortgage interest rates today also reflect differences based on loan

type. The current fixed mortgage rates on conventional loans differ from FHA

and VA programs, so it pays to compare across loan types rather than assuming

your existing loan type is automatically the best fit for a refinance. The current

fixed rate mortgage rates and current mortgage loan interest rates available

to you will depend on your credit score, equity position, and overall financial

profile.

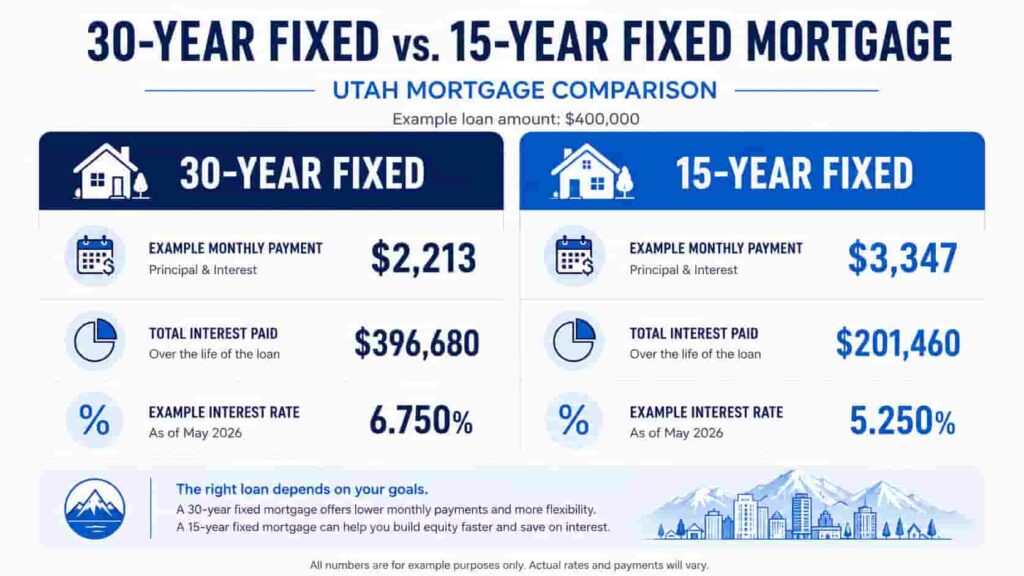

One of the most important decisions in any refinance is choosing your new loan

term. The utah mortgage rates 30 year fixed offer lower monthly payments,

making them appealing for homeowners who prioritize cash flow. The refinance

rates 30 year fixed are particularly attractive for borrowers who want a

predictable payment without stretching their budget.

However, homeowners with sufficient equity and income stability should seriously

consider the utah 15 year mortgage rate, which typically runs half a percentage

point or more below 30-year pricing. Refinancing into a 15-year loan – especially

if you are already several years into your current mortgage – can dramatically

reduce total interest paid while building equity at a much faster pace.

For homeowners trying to decide between terms, running both scenarios through

a utah mortgage calculator 2026 is the clearest way to see which option saves

more money over your expected ownership horizon. The 30 year fixed

mortgage rates and 15 year mortgage rates currently available in Utah make

both options worth modeling before committing.

Knowing how to compare mortgage rates utah effectively is where most

refinancing homeowners leave money on the table. The average mortgage rate

salt lake city lenders advertise is a starting point, not a final offer. Lenders price

loans based on risk, and getting quotes from at least three – a local Utah lender,

a credit union, and an online lender – consistently produces better results than

accepting the first offer.

The best mortgage lenders utah 2026 will provide a Loan Estimate within three

business days of your application, laying out not just the rate but the APR,

closing costs, and monthly payment. This makes side-by-side comparison

straightforward. Pay close attention to lender fees, which can add thousands to

the total cost of a refinance even when the quoted rate looks competitive.

When comparing offers, prioritize the APR over the interest rate alone. The APR

incorporates lender fees and gives a more accurate picture of the true cost of the

loan over its term – two lenders can quote the same rate but have meaningfully

different APRs depending on their fee structures. Always compare the full Loan

Estimate, not just the headline number.

Once you have selected a lender and confirmed the numbers make sense, the

next step is to lock in mortgage rate utah. Rate locks typically run 30 to 60

days at no additional charge, protecting you from rate increases while your

application is processed. In a market where mortgage rates utah 2026 can shift

week to week based on economic data, locking early is the safer move for most

borrowers.

Not every homeowner should refinance mortgage utah today, even when rates

are lower than their existing loan. The classic rule of thumb still applies:

refinancing makes financial sense if you can reduce your rate by at least 0.75 to

1 percentage point and plan to stay in the home long enough to recoup closing

costs – typically two to three years.

The utah mortgage rate forecast from most analysts suggests rates will remain

in the 6 percent range through the rest of 2026, with modest easing possible in

2027 if inflation continues to cool. That outlook means homeowners on the fence

should not count on dramatically better rates appearing soon. If the numbers

work today, waiting may not improve the outcome.

One factor many homeowners overlook: most lenders require a home appraisal

as part of the refinancing process. If your home value has risen since you

purchased, that equity gain can work in your favor – improving your loan-to-value

ratio and potentially eliminating private mortgage insurance (PMI) you may still

be paying. That adds another layer of monthly savings beyond any rate

reduction.

The lowest mortgage rates utah homeowners can realistically access right now

depend on credit score, loan-to-value ratio, and overall debt profile. Borrowers

with credit scores above 740, substantial home equity, and low debt-to-income

ratios are accessing the most competitive pricing. Run the numbers on your

specific situation, compare the home loan interest rates available to you, and

make sure the monthly savings justify the closing costs within a timeline that

matches your plans. For many Utah homeowners, that math is working in their

favor right now.