Buying a home is one of the biggest financial decisions you’ll ever make, and understanding current mortgage rates can help you save thousands of dollars over the life of your loan. Even a small difference in interest rates can significantly impact your monthly payment and the total amount you pay over time.

Whether you’re purchasing your first home, refinancing an existing loan, or comparing lenders, staying informed about mortgage rates today is essential. Rates are influenced by factors such as inflation, economic growth, the Federal Reserve’s policies, your credit score, loan type, and down payment.

This guide explains how mortgage rates work, what affects them in 2026, and how you can find the best mortgage rates for your financial situation.

What Are Current Mortgage Rates?

Current mortgage rates are the interest rates lenders offer borrowers for financing a home purchase or refinance. These rates change daily based on market conditions and individual borrower qualifications.

The rate you receive depends on several factors, including:

- Credit score

- Debt-to-income ratio

- Income stability

- Down payment amount

- Loan term

- Property type

- Loan program

Because lenders calculate risk differently, rates can vary from one company to another. Comparing multiple offers is one of the easiest ways to reduce your borrowing costs.

Mortgage Rates Today: What’s Influencing Them?

Several economic factors affect mortgage rates today, including:

Inflation

Higher inflation generally pushes mortgage interest rates upward because lenders require higher returns to offset the reduced purchasing power of future payments.

Federal Reserve Policy

Although the Federal Reserve does not directly set mortgage interest rates, its decisions regarding benchmark interest rates influence borrowing costs throughout the economy.

Bond Market Performance

Mortgage rates closely follow yields on U.S. Treasury securities, especially the 10-year Treasury note. When bond yields rise, mortgage rates often increase as well.

Housing Market Conditions

Demand for homes and available housing inventory can also impact lending activity and overall market pricing.

Compare 30-Year and 15-Year Mortgage Rates

Choosing the right loan term is an important part of finding affordable financing.

30 Year Fixed Mortgage Rates

30 year fixed mortgage rates remain the most popular option because they provide predictable monthly payments over the life of the loan. Although borrowers typically pay more interest overall, the lower monthly payment offers greater budgeting flexibility.

This option is ideal for buyers who want lower monthly expenses or plan to stay in their home for many years.

15 Year Mortgage Rates

Borrowers looking to save on interest often choose 15 year mortgage rates. These loans generally offer lower interest rates than 30-year mortgages and allow homeowners to build equity faster.

However, monthly payments are usually higher because the loan is repaid over a shorter period.

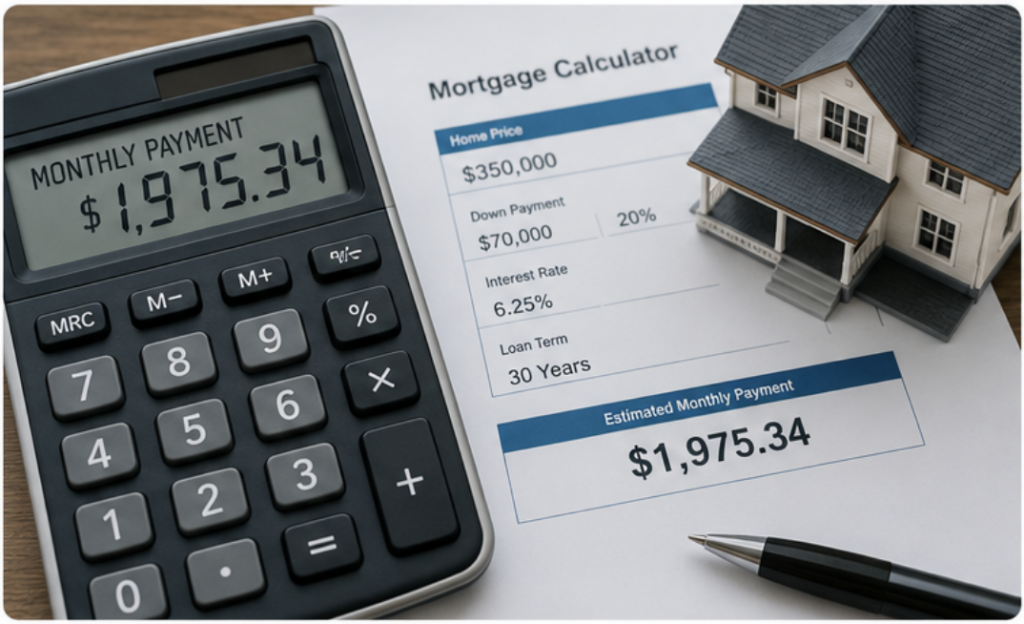

Use a Mortgage Calculator Before You Buy

Before shopping for lenders, estimate your monthly housing costs using a mortgage calculator. These tools help calculate estimated payments based on:

- Home price

- Down payment

- Interest rate

- Loan term

- Property taxes

- Homeowners insurance

A mortgage payment calculator can also help compare different loan scenarios so you understand how changing your down payment or interest rate affects your monthly payment.

How Much Mortgage Can I Afford?

One of the most common questions buyers ask is, how much mortgage can I afford?

While every borrower is different, lenders generally evaluate:

- Annual income

- Existing debt

- Monthly expenses

- Credit score

- Available savings

Many experts recommend keeping total monthly housing expenses below 28% of your gross monthly income and total debt below 36%, although qualifying guidelines vary by lender.

Running several affordability scenarios before shopping can help narrow your home search to a realistic price range.

How to Get the Best Mortgage Rates

Finding the best mortgage rates requires more than simply choosing the lender advertising the lowest rate.

Consider these strategies:

Improve Your Credit Score

Borrowers with higher credit scores typically receive lower interest rates. Paying bills on time, reducing credit card balances, and avoiding new debt before applying can improve your borrowing profile.

Increase Your Down Payment

A larger down payment reduces lender risk and may qualify you for better pricing while lowering private mortgage insurance costs.

Compare Multiple Lenders

Request several loan estimates before making a decision. Different lenders may offer different rates, fees, and closing costs for the same borrower.

Lock Your Rate

Mortgage rates can change daily. Once you’ve found a favorable offer, consider locking your rate to protect against market increases before closing.

Choosing the Right Mortgage Lender

Selecting the right mortgage lender is just as important as finding a competitive interest rate.

When comparing lenders, evaluate:

- Interest rates

- Closing costs

- Customer reviews

- Loan options

- Digital application process

- Closing timeline

Searching for a mortgage lender near me may help if you prefer in-person service, while online lenders often provide faster applications and competitive pricing.

Some buyers also work with a mortgage broker near me, who can compare loans from multiple lenders and help identify financing options that match their needs.

Best Mortgage Companies and Best Mortgage Lenders

Many borrowers begin by researching the best mortgage companies and best mortgage lenders. The ideal lender depends on your financial situation rather than a single national ranking.

Look for lenders that offer:

- Competitive interest rates

- Transparent fees

- Strong customer service

- Flexible loan programs

- Fast underwriting

- Positive customer satisfaction ratings

Always compare loan estimates side by side before choosing a lender.

Understanding Different Types of Home Loans

There are several types of home loans, each designed for different borrowers.

Conventional Mortgage Loan

A conventional mortgage loan is not backed by the federal government. These loans typically require stronger credit profiles but often offer competitive home loan rates for qualified borrowers.

FHA Home Loan

An FHA home loan is designed for borrowers with lower credit scores or smaller down payments. These loans often provide easier qualification requirements but include mortgage insurance premiums.

VA Home Loan

Eligible military service members, veterans, and some surviving spouses may qualify for a VA home loan, which offers benefits such as no down payment and no private mortgage insurance.

First Time Home Buyer Mortgage

A first time home buyer mortgage may include lower down payment requirements, reduced closing costs, or state and local assistance programs.

Many buyers also qualify for a first time home buyer loan that offers additional financial support or favorable lending terms.

How to Apply for a Mortgage

Once you’ve chosen a lender, it’s time to apply for a mortgage.

Most lenders require:

- Proof of income

- Tax returns

- Bank statements

- Employment verification

- Credit history

- Identification

Preparing these documents in advance can speed up the approval process.

Mortgage Pre Approval: Why It Matters

Obtaining mortgage pre approval before shopping for homes demonstrates to sellers that you’re a serious buyer.

If you’re wondering how to get pre approved for a mortgage, the process usually includes:

- Completing a loan application.

- Authorizing a credit check.

- Providing income and asset documentation.

- Receiving a conditional approval letter stating your estimated borrowing amount.

A pre-approval can make your offer more competitive in today’s housing market.

Request a Mortgage Quote Before Choosing a Loan

Before committing to any lender, request a personalized mortgage quote.

Quotes typically include:

- Interest rate

- Annual percentage rate (APR)

- Estimated monthly payment

- Closing costs

- Loan fees

Comparing several quotes side by side gives you a clearer picture of your total borrowing costs rather than focusing solely on interest rates.

The Bottom Line

Understanding current mortgage rates is the first step toward making a smart home financing decision in 2026. By monitoring mortgage rates today, comparing lenders, using a mortgage calculator, and exploring different loan options, you can improve your chances of securing the right financing for your budget.

Whether you’re looking for the best mortgage rates, researching home loan rates, exploring a first time home buyer loan, or preparing to apply for a mortgage, taking the time to compare offers can lead to significant long-term savings.

Before choosing a loan, compare multiple lenders, request a personalized mortgage quote, and complete your mortgage pre approval. The right preparation can help you find a home loan that fits both your financial goals and your monthly budget.

Frequently Asked Questions

What are current mortgage rates?

Current mortgage rates are the interest rates lenders offer for home loans, and they vary based on market conditions and borrower qualifications.

How can I get the best mortgage rates?

Improve your credit score, compare multiple lenders, increase your down payment, and get pre-approved before applying.

What is mortgage pre approval?

Mortgage pre-approval is a lender’s estimate of how much you can borrow after reviewing your financial information.